Advances in diagnostics and therapeutics are improving the early detection, treatment and management of disease, with significant implications for health and life insurance.

Suggested citation

Geneva Association. 2026.

Insuring Tomorrow’s Cures:

Balancing the promises and practicalities of innovative medicine

Authors: Adrita Bhattacharya-Craven and Christoph Nabholz.

February.

2 min read

Key Findings

-

-

Innovations such as AI-supported diagnostics, genetic risk profiling, liquid biopsies and wearable technologies are making health risks more visible, often before symptoms emerge.

-

New therapies, including GLP-1 medicines, gene therapies, cell therapies and immunotherapies, have the potential to improve outcomes and expand the insurable population, but may also increase pressure on healthcare budgets and insurance systems.

-

Medical innovation is likely to require insurers to modernise product design, underwriting and risk assessment, reflecting a growing emphasis on prevention, early intervention and changing health profiles over time.

-

Insurers can help translate medical breakthroughs into sustainable value by adopting new coverage approaches, exploring innovative risk-sharing mechanisms and collaborating with healthcare stakeholders and regulators.

Q&A

-

What is this report about and what are its main findings?

This report examines how advances in medical diagnostics and treatments could reshape health and life insurance. It analyses emerging technologies ranging from AI-supported imaging and multi-cancer early detection tests to gene therapies, immunotherapies and obesity medicines. The report finds that these innovations have the potential to improve health outcomes, expand insurability and support longer, healthier lives, but they also challenge traditional approaches to product design, underwriting, pricing and healthcare financing.

-

Why do medical innovations matter for life and health insurers?

Medical innovation affects the core assumptions that underpin health and life insurance. Earlier detection may increase diagnosed disease incidence even as outcomes improve, while more effective therapies can extend survival, improve quality of life and make some previously uninsurable conditions insurable. Health insurers may face rising claims costs from breakthrough treatments, while life insurers may need to adapt to changing mortality, morbidity and longevity trends. Across both sectors, insurers will need to rethink products, pricing and risk assessment to reflect a rapidly evolving healthcare landscape.

-

How could medical innovation change insurance products and underwriting?

As earlier detection and more effective treatments change the course of disease, insurers may need to update product definitions, coverage triggers and underwriting approaches. The report suggests placing greater emphasis on prevention and proactive health management, while moving towards more dynamic risk assessment that reflects changes in policyholders' health over time. Insurers must also balance the benefits of more precise risk segmentation with concerns around affordability, equity, privacy and consumer trust.

-

How can insurers manage the cost of breakthrough medical treatments?

The report highlights several approaches that could help insurers manage the financial impact of high-cost therapies. These include reinsurance solutions for catastrophic treatment costs, subscription-style payment models, outcome-based and annuitised payment arrangements, and collective negotiations on treatment pricing. Such mechanisms can help make medical innovation more affordable and predictable while supporting patient access to new therapies.

7 min read

Authors

Adrita Bhattacharya-Craven, Director Population Health Trends, Geneva Association

Christoph Nabholz, Founder, Risk Insight Consulting

Introduction

The pace of medical innovation has increased in recent years. It has been driven by the growth of artificial intelligence (AI)-enhanced personalised medicine alongside advances in general medicine. This trend may challenge the assumptions underpinning the products and pricing of life and health insurers, who base their models on population-level patterns of morbidity, mortality, longevity, and disability.

Four factors could prove disruptive for life and health insurers: 1) earlier detection may increase the incidence of disease, even as outcomes improve; 2) curative or near-curative therapies can expand the insurable pool, including previously excluded conditions; 3) direct-to-consumer diagnostics could lead to information asymmetries between insurers and policyholders, leading to adverse selection; and 4) a small number of high-cost therapies could destabilise premiums and coverage limits without new financing approaches.

The Geneva Association has mapped key diagnostic and therapeutic advances, assessing their likely impacts on insurance products, underwriting, and regulation. This work draws on a literature review, as well as a series of roundtables with experts from insurance, biotech, the pharmaceutical industry, medicine, and academia.

Diagnostics: More digital, less invasive

Five diagnostic innovations, supported by AI, are making health risks more visible, often before symptoms emerge.

AI-supported imaging can help interpret CT, MRI, ultrasound and similar scans,1 spotting patterns linked to early cancer, vascular change, or other disease signals. Its near-term value is likely to be better triage and higher reading capacity, allowing more people to be screened sooner. Its reach, however, is still limited by capacity, staffing, and referral pathways.

Liquid biopsies and multi-cancer early detection (MCED) tests can identify tumour-related signals without an invasive tissue biopsy through bodily fluids. MCED aims to detect multiple cancers with one test, potentially improving survival through earlier intervention. Current limits include variable sensitivity for small tumours and the practical challenge of managing follow-ups when cancer signals are present but without clear tumour identification.2

Genetic risk profiling, such as polygenic risk scores, estimates inherited risk for complex diseases. Their accuracy varies3 and results can be misunderstood. Misinterpretation of risk is a concern, where a finding of higher chance of disease is treated like a diagnosis, driving anxiety and unnecessary testing.

Wearables and remote monitoring can track measures such as heart rhythm, glucose, sleep, and activity. They can promote healthy habits, early intervention, and improved chronic-disease management but depend on sustained behaviour change.

Multi-omics and companion diagnostics combine genetic, transcriptomic, proteomic, and metabolic data to improve diagnostic precision and match patients to therapies. While promising, these approaches are currently constrained by cost, complexity, and the need for specialist infrastructure.

Therapies: From management to modification and cure

We identified five therapeutic areas, which could better alter and manage disease pathways:

Metabolic therapies, including GLP-1 class drugs, can improve obesity and diabetes outcomes and may reduce cardiovascular risk among other health conditions. However, uncertainty remains around long term adherence and side effects.4,5,6,7

Genetic medicines, including gene therapy and gene editing, offer the prospect of durable benefit or one-off cures for certain inherited conditions but often with very high upfront cost.

Cell therapies can produce strong remission outcomes in some cancers8 but are hard to manufacture and scale.

RNA-based medical technology has paved the way for relatively quick vaccine development following the COVID-19 pandemic. However, use of RNA-techniques for personalised cancer vaccines is harder to scale because, unlike a virus, each tumour is unique.

Immunotherapies can redirect immune responses in cancer and may slow progression in early Alzheimer’s and other diseases. However, benefits are currently modest, especially for the latter, and require careful monitoring.

The development of diagnostic and therapeutic breakthroughs continues to be constrained by both limited biomedical infrastructure and affordability challenges. The report highlights three recurring hurdles: 1) high prices or high demand impacting healthcare payers; 2) uncertain reimbursement creating a wariness around provision; and 3) gaps between patient expectations and what payers can realistically fund.

What does this mean for life and health insurance?

Some diagnostic innovations can be deployed relatively quickly into existing care pathways, with short-term impacts on insurers. Therapeutic disruption will have a medium-term, five-year impact, led by anti-obesity drugs and metabolic health breakthroughs. Therapies targeting small eligible populations or requiring specialist centres are expected to have a more modest impact.

Health insurance: First-wave effects

Health insurers may face near-term budget pressure from 1) claims derived from both high-cost one-off treatments; and 2) high-volume chronic therapies, such as GLP-1 drugs. This will be balanced by improved detection and prevention approaches, although such investments could take years to accrue.

Life insurance: Mortality protection mostly benefits

Expectations of improved treatment and survival outcomes9,10 will require insurers’ models to be more dynamic. Medical innovations may expand eligibility criteria, widening the risk pool and allowing greater granularity in rate and loading reviews. Better tracking of biomarkers will allow insurers more touchpoints with customers, improving the perceived value of coverage.

Living benefits: Mixed and product-specific effects

Living benefit lines are exposed to changes in diagnosis timing, treatment effectiveness, and longevity. Annuities may be impacted by longer lifespans; however, healthier ageing may extend working lives and shift retirement timing. Critical illness will be affected by earlier screening and resultant early-stage diagnoses, pressing insurers to revisit definitions and triggers. Meaningful dementia breakthroughs would alter care needs, customer expectations, and pricing assumptions. Improved recovery outcomes from chronic and obesity-related conditions may reduce long-duration claims in disability and income protection lines.

The road ahead: Practical considerations for insurers

Coverage decisions: Define value consistently

Closer alignment to independent public-sector evidence reviews would provide enhanced guidance to what is covered and to what level. A shared, industry-wide view on high-value versus low-value tests and treatments could reduce waste and protect trust.

Product design: Prevention, pathways, and triggers

Critical illness products, in light of earlier detection, will benefit from product and trigger updates. Distinguishing between lumpsum and staggered payouts will create greater consumer value as well as keep products financially viable. Improving the inclusion of preventative measures within products provides some counterweight to the soaring costs of some therapeutic innovations.

Underwriting: Towards a more dynamic approach

A shift to continuous risk assessment and dynamic underwriting can capture material risk changes over the policy term, underpinned by clear rules on consent, data use and customer communication. Direct-to-consumer testing risks creating information asymmetries and adverse selection. Increasingly granular risk segmentation may improve identification of higher-risk individuals, but also raises concerns around equity, affordability, and appropriate disclosure requirements. Insurers therefore face a delicate balance between more precise underwriting and broader social expectations of common risk pooling.

Managing shocks: Pooling and payment tools

Mechanisms that turn high-cost/high-demand volatility into more predictable spending include: 1) reinsurance or stop-loss protection for defined high-cost therapies; 2) subscription-style treatment payments at a predictable per-member cost;11 3) outcome-linked, annuitised payments;12 and 4) collective, evidence-based price negotiations for new therapeutics.

TABLE 1: A simplified schematic of emerging risk pooling and purchasing mechanisms

Emerging models/ | Reinsurance | Subscription model | Annuitised | Disease-specific |

| Insurers against | Low frequency catastrophic claims risk | Volume risk | Upfront budgetary shock and performance risk | Price volatility |

| How it functions | Excess cover for unexpected claims from (defined) therapies through stoploss arrangements | Periodic fixed fee to access high-cost therapies | Costs spread over several years, which can also be performance-linked | Payers (including insurers) negotiate terms in defined disease areas using collective bargaining |

| Risk pooling | Yes, risk transferred to reinsurer | Yes, at payer level, based on anticipated demand | No, it is a contracting mechanism | No, essentially a procurement arrangement |

| Implications for health insurance | Protects solvency, especially for rare or high-cost cases | Predictable costs but there is a risk of getting projections wrong | Eases affordability but adds long-term liabilities and the need to follow clinical outcomes | Improves access and bargaining power, but limited to selected conditions |

| Implications for life insurance | May improve insurability for conditions that were previously excluded, for example, lifelong conditions cured by gene editing | May improve insurability for conditions Could affect mortality/longevity projections if uptake is widespread | May improve insurability for conditions Could affect mortality/longevity projections if uptake is widespread | N/A |

Source: Geneva Association

Regulation and ethics: Genetic data, AI, and trust

Insurers need to navigate widely differing and fast-evolving rules on genetic and health data. They need to balance strong consumer safeguards with the ability to design sustainable, innovative forms of coverage. Dialogue with public authorities and interest groups is not merely an issue of compliance. Such exchanges can define clear guardrails alongside core business considerations.

Concluding remarks

Medical innovation is likely to deliver earlier signals for disease risk and detection, alongside more effective treatments, improving survival and quality of life. At the same time, rising treatment costs and increasingly precise diagnostics may put pressure upon traditional risk pooling and challenge notions of access, equity and affordability. Insurers can act now by redesigning products to support prevention and earlier diagnosis, modernising underwriting and risk financing, and engaging regulators and health system partners on the conditions needed to scale new innovations.

Foreword

Medicine is in a period of transition. Healthcare is increasingly shaped by personalised models that reflect individual biology and behaviour rather than so-called population-based approaches. Digitalisation and artificial intelligence are accelerating this shift, expanding what medicine can achieve and the speed of implementation. These developments have important implications for patients, for health providers, and for payers - including insurers.

This report examines how advances in diagnostics and therapeutics are changing the visibility, predictability, and management of disease – and what this means for health and life insurance. It shows how earlier detection and more precise intervention could improve outcomes, support prevention, and alter long-term risk profiles, with artificial intelligence emerging as a key enabler across these developments.

The analysis also reveals obstacles to real-world impact. High costs, operational complexity, and uncertainty around financing continue to limit uptake.

Medical innovation will gradually reshape the parameters within which health and life insurance operates, influencing product design, pricing, and risk pooling over time. Responding to these shifts will require careful balance between innovation, affordability, and trust, and continued dialogue across health, insurance, and regulation. Managed thoughtfully, medical progress can strengthen the role of insurance in supporting prevention and more resilient health systems.

Jad Ariss

Managing Director

Executive summary

Modern medicine has reached a turning point. Centuries-old, population-based practice, commonly referred to as general medicine, is now converging with personalised approaches, which customise care based on personal characteristics of a patient, such as genetic profile, lifestyle, and environment. Furthermore, the speed, depth, and reach of these two genres of medicine, are now being dramatically augmented by digitalisation and artificial intelligence (AI).

Framing the outlook of medical innovation

Drawing on an extensive literature review, as well as direct insights from 38 experts across pharmaceutical and biotechnology companies, clinical experts, insurance, and academia, our analysis identifies five categories of diagnostic innovation that make risk more visible, visible earlier, and sometimes visible before it manifests itself as disease. These are:

- AI-powered medical imaging that enhances accuracy and expands screening capacity;

- Liquid biopsies and multi-cancer early detection (MCED) tests that identify tumours through blood-based molecular signals;

- Genomic profiling such as polygenic risk scores (PRS) that quantify inherited risk long before symptoms appear;

- Point-of-care wearables that continuously measure vital biomarkers and turn everyday behaviour into a real-time health dataset; and

- Multi-omics and companion diagnostics that integrate molecular and metabolic information to guide increasingly precise clinical decision-making.

As technologies enable earlier detection, new therapies are emerging that can alter disease trajectories. We identify five categories of therapeutic innovation that are redefining how diseases can be prevented, modified, or cured. These include:

- Metabolic therapies, such as GLP-1 receptor agonists that improve outcomes across obesity, diabetes, cardiovascular disease (CVD), and beyond;

- Genetic medicines encompassing gene therapy and gene editing, aimed at correcting disease at its source;

- Cell therapies and regenerative approaches that use living cells as programmable treatments;

- Ribonucleic acid (RNA)-based treatments that enable rapid, modular drug development including vaccines; and

- Immunotherapies that harness or redirect the immune system to target cancers, autoimmune disease, and other neurodegenerative conditions such as Alzheimer’s.

AI is seen as the unifying enabler across diagnostics, expected to accelerate earlier prediction and detection, with AI-powered medical imaging perceived as being the most transformative for patient outcomes. Therapeutic advances in metabolic and genetic diseases are seen as being the most promising for improving health.

While the clinical promise of many of these innovations is undeniable, their real-world impact will ultimately hinge on being able to overcome operational bottlenecks and affordability challenges. Barriers include high treatment costs that strain health payers’ balance sheets, reimbursement uncertainty that make health providers wary of product offerings, and limited payer-patient alignment that stifles a constructive dialogue around the wider challenges of health financing. Similarly, capital flows into medical innovation have tended to favour high-cost treatments over more scalable solutions, thereby exacerbating these challenges.

Insurance and medical innovation

In the field of diagnostics, insurance experts expect AI-enabled imaging, as well as liquid biopsies for certain cancers, to transform the industry within three to five years, improving underwriting accuracy and enabling earlier disease detection. Over the next decade, MCED tests are forecast to become a standard of care, identifying multiple cancers through molecular signals rather than organ sites.

With regards to new therapies, insurance experts anticipate major disruption within five years, driven by GLP-1 receptor agonists in particular. Insurers questioned see GLP-1 drugs as the most immediate game-changer in tackling obesity, a known risk factor for many chronic health conditions. Following closely behind, cancer treatments are expected to be the next most disruptive therapeutic category. In the long-term, genomic medicine, once implementation hurdles are overcome, could shift healthcare from treating illness to modifying or eliminating inherited risk. This could fundamentally alter L&H insurance risk pools, mortality assumptions, and pricing models.

Health insurance: First wave

Health insurance will feel the earliest and strongest impact of these breakthroughs. Therapeutics, such as high-cost gene, cell, and anti-obesity drugs, are set to test the stability of premiums and coverage limits. Predictive diagnostics and preventive therapies, meanwhile, could enable earlier and more targeted intervention, decreasing long-term costs by lowering hospital and specialist care use. However, annual policy cycles and high customer turnover may dampen expected rates of return on product and service investments, resulting in some difficulty balancing short-term expenditure with long-term gains.

Life insurance: Mortality protection

Therapeutic and diagnostic advances are largely positive for mortality protection products. Advances in gene, cell, and cancer therapies promise lower mortality and a consequently broader insurable pool, requiring new risk assumption and pricing approaches. Early data show GLP-1-related health benefits could also lead to reduced claims. Furthermore, embedding diagnostics and preventative tools can deepen customer engagement and reposition life insurers as proactive well-being partners rather than passive claim payers.

Life insurance: Mixed benefits

Living benefit products face a more complex set of effects. Longer lifespans will extend annuity payouts, but these may be offset by longer working lives and shorter decumulation periods enabled by improved health. Earlier disease detection, via AI and liquid biopsies, could raise early-stage critical illness (CI) claims and warrant updates to product definitions. Therapeutic breakthroughs for diseases such as dementia may reshape long-term care (LTC) needs and resultant expectations of LTC insurance (LTCI) policyholders. Improved recovery from obesity-related risks, such as musculoskeletal problems, could lower disability claim rates.

What next? How medical innovations could affect insurability

The pace of medical innovations may shift the parameters of current insurance risk models. Insurers could expand coverage to cover new cohorts and new diseases; however, they will concurrently have to manage the costs and complications of new diagnoses and treatments. Insurers have the opportunity to rethink their role within rapidly evolving health ecosystems now, rather than simply responding to future events. Addressing the following five issues will shape the future of the industry.

1. Defining what and how much to cover

Greater alignment with national health technology assessment bodies (HTAs) could create more consensus among insurers as to which new innovations are included in cover, while balancing value, affordability and ethics. There are also calls for industry-wide cooperation to define what constitutes truly worthwhile care, to reduce waste, and maintain policyholders’ trust.

2. Redesigning products for prevention and disruptive technologies

The sometimes-exorbitant costs of new cures can be offset by a shift to preventative models, driven by new diagnostics. However, improved screening tools will require a review of disease definitions and benefit triggers within CI products.

3. Rethinking underwriting in the face of dynamic health risks

Improved biomarker tracking allows for dynamic underwriting over the lifetime of a policy. This tends to favour lower-risk policyholders, requiring a delicate balance between technical underwriting and broader ethical considerations. Innovation on the consumer side, such as direct diagnostic testing, runs the risk of information asymmetry with the insurer. This prospect of adverse selection may force underwriters to revisit disclosure agreements.

4. Revisiting risk pooling and purchasing models

New pooling mechanisms, such as subscription-based models and performance-based annuitised provider payments, may improve the absorption of higher medical costs. These warrant further exploration for their replicability and scalability.

5. Navigating regulatory and ethical tensions

Uneven global genetic and health data governance challenges both insurers and public authorities seeking to promote improved coverage. Dialogue between all sides may improve the balance between actuarial fairness and the social need for protection in the face of improved diagnostics and therapeutics.

Introduction

Modern medicine is undergoing profound change. For centuries, healthcare has relied on general medicine, using broad clinical guidelines, statistical evidence, and average treatment responses drawn from large patient groups. This established model is now converging with rapid advances in precision medicine tailored to the individual, using personal characteristics such as genetic profile, lifestyle, and environment.1 Together, these medical approaches are reshaping both the diagnostic and therapeutic landscapes.

Global health systems are grappling with this transformation. For policymakers, as well as health payers (including national health schemes, statutory social insurance/sickness funds, and private health insurers), medical innovation raises fundamental questions. These include:

- Healthcare infrastructure requirements and organisation (e.g. specialist laboratories, health data/bio banks, etc.);

- Training the healthcare workforce;

- Innovation investment and funding (including a public-private mix); and

- Healthcare delivery.

More generally, policymakers and payers have a considerable challenge in balancing the benefits of modern medicine with healthcare cost, access, and equity. The resulting policy choices have implications far beyond health systems. They increasingly affect economic prosperity, as ageing populations and a less healthy workforce place pressure on productivity and growth.2

The acceleration of innovative medicine

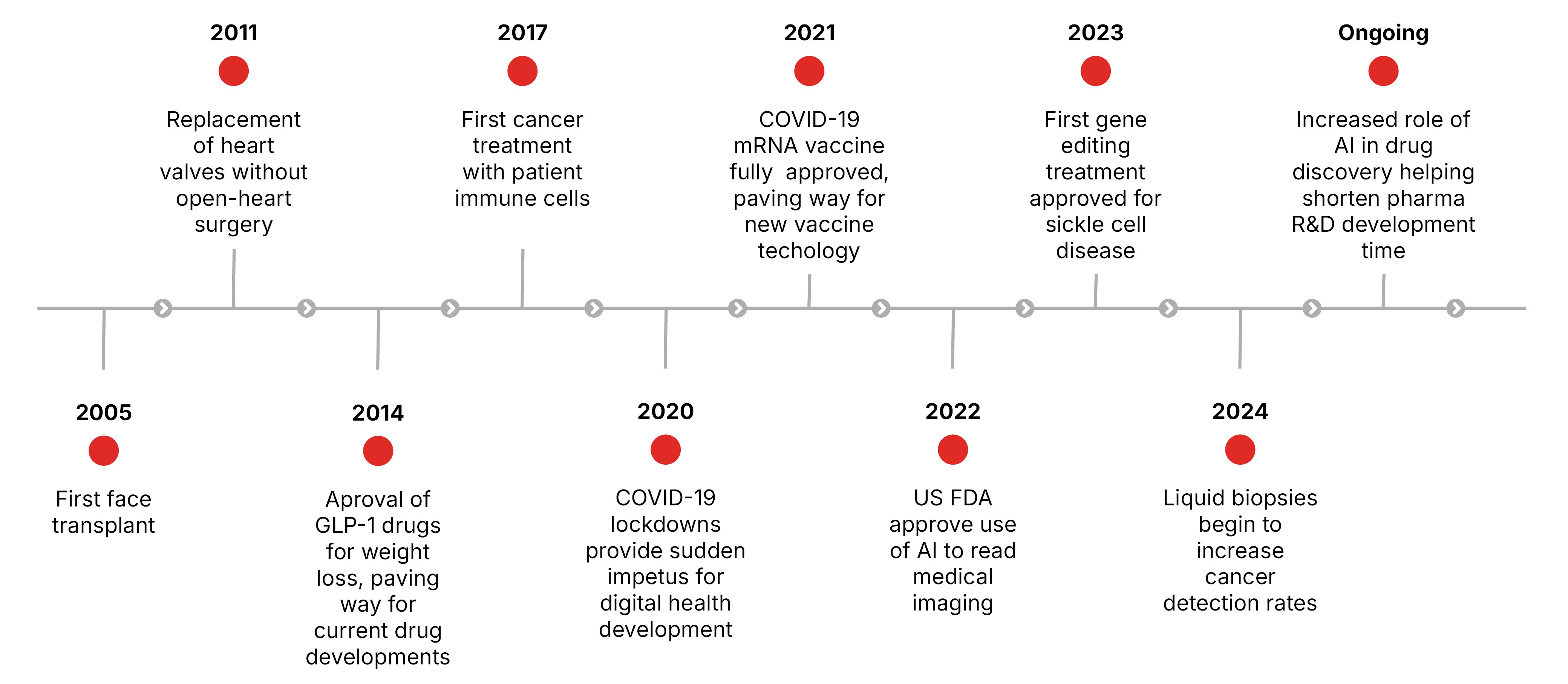

Major breakthroughs spanning general and personalised medicine over the last two decades have transformed how health risks are predicted, diagnosed, eliminated, treated, and managed. Figure 1 illustrates, without being exhaustive, the recent rapid pace of medical innovation.

FIGURE 1: Medical advancement over the past 20 years

Source: Geneva Association

Personalised medicine has driven many recent molecular and genetic innovations, such as liquid biopsies (tests on body fluids such as blood or urine) in diagnosing rare diseases or cancers. However, the widespread uptake of high-impact general medicine-based therapies in recent years – most notably glucagon-like peptide-1 (GLP-1) receptor agonists – has been equally transformative. Long-established in the treatment of type 2 diabetes, GLP-1s took on a new significance following their approval targeting weight loss in 2014, accelerating the development of more effective drugs.

The rapid adoption of GLP-1 drugs has intensified public debate around the allocation of healthcare resources. In recent years, this adoption has prompted many pharmaceutical producers to start reinvesting in general medicine, particularly those focused on cardio-metabolic health, previously sidelined in favour of treatments of more complex diseases such as cancer (see Section 4.2).3

The speed, depth, and reach of innovation in personalised and general medicine are now being dramatically amplified by digitalisation more broadly and by artificial intelligence (AI) in particular.

The relevance for life and health insurers

The adoption, financing and delivery of recent medical innovations are reshaping how insurers assess and price biometric risks, including morbidity, mortality, longevity, and disability. Upstream decisions in healthcare policy and provision are trickling down to influence the design, accessibility, affordability, and sustainability of insurance coverage.

Predictive innovations, such as DNA testing, could establish a higher predisposition to adverse health conditions, making them harder to insure. Equally, when adverse health outcomes are paired with novel treatments, some biometric risks can be mitigated entirely, thereby potentially expanding the pool of insurable health risks. This includes previously incurable and rare diseases, HIV, type 2 diabetes, and even certain cancers.

New diagnostic and treatment breakthroughs may also mean that traditional, one-off health measures used in the insurance application process, such as body mass index (BMI), blood glucose, and cholesterol, are no longer sufficient on their own. As new therapies emerge, the level of risk assessed at the start of a policy can shift markedly over time, falling sharply in some cases, while rising in others, especially if treatment is stopped.

Improved diagnostic and predictive insights can further exacerbate information asymmetry between insurer and policyholder, especially as more direct-to-consumer testing kits enter the market. For instance, personalised genomic data-based testing, which provides estimates of disease risk, could lead to adverse selection. If individuals know more about their health risks than insurers do, higher-risk people may be more likely to buy L&H insurance. Conversely, more precise risk assessments could challenge premium affordability for individuals with higher risk.

These clinical uncertainties and technical challenges are compounded by financial stresses. The cost of delivering breakthrough therapies often exceeds the capacity of traditional insurance models. Some gene therapies are priced in the millions, raising questions about how far such innovations can realistically be absorbed by health systems.

Rapid advances in medical technologies come with cost implications for insurers as well as for societies more widely. Insurers will have to respond in a way that is financially sustainable, while continuing to maintain or expand meaningful risk protection. Estimated global medical cost inflation has consistently outpaced the consumer price index (CPI) for many years. In 2023, medical inflation was 10.7% against an end-of-period CPI of 6%; in 2024 the figures were 10.4% against 4.9%.4,5 Insurers’ ability to achieve an optimal mix of innovation, inclusion, solvency, customer trust, ethics, and sustainability will only grow in importance.

Scope and structure of the report

This publication examines how L&H insurers manage the opportunities and exposures of accelerating medical innovation. Drawing on academic and grey literature,6 as well as insights directly sourced from 38 subject experts (see Box 1), this report:

- Maps the medical innovation frontier. We outline the key breakthrough diagnostics and therapeutics transforming care and cost dynamics. (Section 2)

- Assesses the insurance implications. We analyse how medical advances affect product design, underwriting, pricing, and claims. (Section 3)

- Frames associated strategic challenges for L&H insurers. We identify the commercial, operational, and regulatory shifts insurers must navigate to sustain accessibility and affordability of their products and services. (Section 4)

L&H insurers need to keep pace with medical innovation. This report aims to foster an informed industry-wide dialogue on how insurers can sustainably achieve this goal while providing their policyholders with affordable and sufficient coverage to access these new innovations.

Box 1: Methodology used in this study

This study used a three-part qualitative research approach:

Desk research: We undertook an extensive review of academic and other literature to understand the evidence base, gaps, and key themes, which guide the structure of this report.

Expert clinical roundtables: We organised two roundtables with 20 experts from pharmaceutical and biotechnology companies, re/insurers, academia, and clinical practice. The roundtables followed an agenda informed by the desk research, exploring the clinical and technical characteristics of emerging diagnostic and therapeutic innovations, as well as their broader health systems implications.

Insurance executive roundtables: We further held two qualitative roundtables with 18 senior insurance professionals, including underwriting specialists, claims experts, and strategy leaders. These discussions built on insights from the preceding set of roundtables and examined the implications for L&H insurance.

Source: Geneva Association

Mapping the new frontier: From predictive diagnostics to transformative therapies

This section maps the new medical innovation frontier across two clusters: five diagnostic and five therapeutic categories. Each cluster is further broken down to understand: 1) clinical impact; 2) overall cost dynamics; and 3) its ultimate macro-level effects. The categories of breakthroughs identified in each cluster are based on our own analysis and are not intended to be exhaustive.

Novel diagnostics: Shifting from reactive to predictive

In order to understand how earlier identification of risk and disease can lead to improved prevention, we grouped the most influential diagnostic advances into five broad categories:

D1. AI-powered medical imaging

D2. Liquid biopsies

D3. Genomic profiling

D4. Point-of-care wearables

D5. Multi-omics platforms

Each plays a distinct role, yet are becoming ever more interconnected, as AI permeates all aspects of diagnostics, enhancing their speed of development, accuracy, and interpretation.

“AI won’t be a product; it will be a layer across everything … it will touch everything.”

Eric de La Fortelle

Cathay Health

D1. AI-powered medical imaging

Over the next decade, AI-driven medical imaging is expected to become the most influential area of innovation. Clinical experts anticipate that AI-enabled diagnostic technologies will deliver the greatest improvements in patient outcomes.

By analysing computed tomography (CT) scans, magnetic resonance imaging (MRI), ultrasound, and other imaging technologies, AI can flag subtle disease signals, such as early tumours, micro-haemorrhages, or vascular changes, which are often invisible to the human eye. As these tools continue to be trained on vast clinical datasets, they enable earlier detection, help prioritise the highest-risk patients for rapid follow-up, and can expand access to timely diagnosis for larger segments of the population.7

“A machine will eventually do it way better than a human … it’s happening already in radiology and pathology.”

Nicholas Wood

UCL

Evidence from real-world studies shows that AI can maintain or even improve diagnostic accuracy while accelerating reading times. For example, a Swedish trial demonstrated that AI-supported mammography doubled reading capacity while preserving cancer-detection performance.8 The real promise, however, lies not in efficiency alone, but in the potential for more people to be screened earlier, especially for cancers and cardiovascular disease (CVD), where late diagnosis can drive poor health outcomes.

Yet this potential is constrained by resources. Even in advanced health systems, access to CT and MRI scanning remains limited by long waiting lists, referral bottlenecks, workforce shortages, and the concentration of advanced imaging equipment is specialised centres rather than community settings. AI cannot compensate for a lack of scanners. Earlier detection at scale will likely only be achieved if accompanied by investments in imaging capacity, workflow redesign, and broader access to scanning infrastructure.

“We’re seeing severe under-testing even in developed systems … awareness and workflow are huge barriers.”

Frank Desiere

CorTec Neuro

D2. Liquid biopsies and molecular early detection

Liquid biopsies represent a major shift in how certain cancers can be detected. Unlike tissue biopsies, they are minimally invasive and can be repeated frequently, making them well-suited for population-level screening.

A rapidly advancing subset of this technology is multi-cancer early detection (MCED), which aims to identify possible molecular cancer signals from multiple tumour types through a single blood test.9 In principle, this could detect cancers long before symptoms appear, improving survival rates and reducing future treatment costs.

However, real-world performance remains mixed. Early findings from large-scale trials in the US and UK10 can effectively confirm when cancer signals are present, but have lower sensitivity to early and small tumours, i.e. those most difficult to identify yet often the most critical to detect.

“MCED blood tests mark an exciting advancement in cancer detection, but excitement must be balanced with caution. If a result can’t be acted upon and the site of the cancer is unclear, how should follow-up be managed?”

Prachi Patkee

Swiss Re

D3. Genomic profiling

By analysing thousands of genetic variants, often combined with lifestyle and environmental data, polygenic risk scores (PRS) aim to predict who may develop a disease before it emerges. When supported by AI, these profiles can help target prevention and tailor interventions for complex conditions.

While promising, PRS still face validation issues. For example, PRS may signal elevated health risk for years, or even decades, before any clinical signs of disease emerge.11 More importantly, a comprehensive review of published PRS found that, on average, only 11% of people who later went on to develop a disease were correctly identified.12

PRS may cause patients undue stress and may pressure physicians to order repeated follow-up screenings or initiate preventive interventions prematurely. Equally, in the absence of strong clinical validation, PRS may blur the line between risk prediction (the chances of a disease developing) and actual diagnosis (identification of a disease or condition) raising ethical, regulatory and privacy concerns. PRS may further require expert counselling to help individuals interpret these results responsibly.

D4. Point-of-care wearables

AI-enabled wearable or remote devices can continuously track biometric indicators such as heart rhythms, glucose levels, and activity patterns. This real-time monitoring, enables earlier detection of changes in health, supports the management of chronic conditions such as diabetes, and can trigger timely clinical responses. For patients, tools such as continuous glucose monitoring (CGM) and other real-time physiological data, provide powerful insights into how their bodies respond, helping them engage more actively in their own care and adopt healthier habits.

D5. Multi-omics platforms

While genomic profiling focuses only on DNA, multi-omics brings together DNA, RNA, proteins, and metabolism to reveal how a disease is truly unfolding. Currently limited to very specialised settings, these tools nonetheless help identify subtle molecular patterns that can guide earlier detection and more precise risk stratification. A further part of this platform, companion diagnostics, are designed to determine whether a patient is eligible for a specific therapy (most commonly cancer drugs) by confirming the presence of a particular DNA mutation or biomarker. Multi-omics platforms are paving the way for more personalised treatment pathways, though currently they are constrained by cost, workflow complexity, and the need for specialised laboratory infrastructure.

Novel therapies: Redefining how diseases are cured

Alongside diagnostic advances, new therapeutic approaches are reshaping disease treatment, or even elimination, by modifying their underlying biology. Five therapeutic categories will likely be most influential in future curing of diseases:

T1. Metabolic therapy

T2. Genetic medicine

T3. Cell therapy

T4. RNA-based therapy

T5. Immunotherapy

Despite having different biological pathways, these therapeutic categories are increasingly used in combination. These combinations demonstrate how treatments are drawing on both general and personalised medicine. However, their clinical benefit is offset by financial and operational bottlenecks, including complex manufacturing and infrastructure requirements.

T1. Metabolic therapy

Metabolic therapies copy natural gut and pancreas hormones that help control blood sugar, reduce appetite, and slow digestion, leading to weight loss and improved metabolic health. Commonly known as GLP-1, drugs such as semaglutide and tirzepatide have already had significant impacts. More recently developed GLP-1 drugs, such as retatrutide13and amycretin, are designed to act on more metabolic pathways, with potentially stronger results.

“The GLP-1 class could be bigger than most blockbusters in history combined.”

Eric de La Fortelle

Cathy Health

GLP-1 drugs provide clear benefits for obesity and diabetes, with growing evidence of long-term CVD protection, and early signs of application in the prevention of some cancers and kidney disease. Despite the considerable potential of GLP-1 drugs, there is a lack of longitudinal evidence, and some experts remain concerned about treatment adherence and long-term side effects. Research suggests only 46% of patients continue to take a GLP-1 drug after 180 days, 29% at one year, and just 15% at two years.14 15 Similarly, their side effects include the loss of muscle mass,16 malnutrition resulting from strong appetite suppression, and increased risk of gallbladder disease.17

T2. Genetic medicines

Gene and genome-editing therapies target disease at its biological root. Established gene therapy adds or replaces faulty genes to correct inherited disorders. Approved gene therapies treatments exist for haemophilia18 and β-thalassemia.19

Genome-editing tools, such as CRISPR, can precisely switch genes on or off, or make targeted changes to the genome, offering the ability to correct inherited defects at source. Genome editing may provide durable cures for diseases such as sickle cell disease20 and hereditary high cholesterol.21

While genetic medicine offers potential cures for rare diseases, it is currently supported only by small studies with limited population subgroups, and short follow-up periods. This underscores the need for extended clinical studies to establish their sustained effectiveness.

T3. Cell therapy

Cell therapies modify or replace patient cells to restore or enhance biological functions. CAR-T therapies22 are one such example, now delivering noteworthy remission rates in several blood cancers. Next-generation approaches aim to overcome barriers in tumours, as well as some autoimmune diseases.

Cancer-targeting CAR-T therapies are challenging to scale because of their complex production process, a factor that may take years to resolve.

T4. RNA-based therapy

RNA-based therapies enable the body to produce therapeutic proteins or silence harmful ones. After sequencing an individual patient’s tumour to ascertain its unique markers, a personalised mRNA vaccine shot is created to train the immune system to attack the cancer cells. Building on the same technology as COVID-19 vaccines, treatments like Moderna’s mRNA-415723 are now testing for cancers such as melanoma and for preventing infectious diseases.

However, mRNA cancer vaccines are far harder to bring to market than COVID-19 vaccines. Unlike a virus, each tumour is biologically unique and changes continuously, requiring personalised rather than batch-made vaccines. Manufacturing a bespoke vaccine, like a personalised cell therapy, is slow, expensive, and difficult to scale for routine use, echoing the same implementation barriers as cell therapy.

T5. Immunotherapy

Immunotherapies modify the immune system to help it recognise and slow down (or eliminate) cancer or neurodegenerative diseases. Alzheimer’s drugs,24 such as Leqembi, Aduhelm and Kisunla, work by helping the immune system clear harmful protein aggregates from the brain, which may slow early disease progression.

Although the benefits are modest, and experts suggest limited population health impact in the immediate future, these immunotherapies are the first treatments aimed at altering the course of Alzheimer’s rather than merely managing symptoms.

“Alzheimer drugs do work but have not yet shown to impact disease sufficiently to be broadly impactful where resources are finite.”

Nicholas Wood

University College London

The economics of innovative medicine

The current wave of therapies, particularly in metabolic and genetic medicine, mark a decisive shift from managing illness to modifying its biological roots. However, scientific success now has to manifest itself as being able to improve health for large numbers of patients in everyday care. Consequently, affordability has emerged as the defining test of their real-world impact.

Table 1 summarises the costs to purchasers of selected novel diagnostic tools and new therapeutic treatments in the US and UK. These two markets provide useful benchmarks. The US represents a largely unrestricted, market-driven pricing environment, with limited national negotiation. By contrast, the UK, through the National Institute for Health and Care Excellence (NICE) and the National Health Service (NHS), reflects one of the world’s most stringent health technology assessment (HTA) and price control systems. Together, they likely capture the upper and lower bounds of what mature health systems are typically willing or able to pay for new treatments.

As an illustration, prices range from over USD 12,000 per year for GLP-1 obesity drugs to USD 2.2 million for a one-off genetic cure for hereditary blood disorders in the US, underscoring an emerging tension between medical progress and financial sustainability. Many new treatments, such as gene therapies and personalised cancer drugs, are extremely expensive to develop and deliver. While they can dramatically improve or save lives, health systems, insurers, and governments often struggle to afford them at scale without threatening long-term financial stability. This has implications for the pace and breadth of adoption of medical breakthroughs.

TABLE 1: COST COMPARISON OF BREAKTHROUGH THERAPIES AND DIAGNOSTICS, US VS UK25

Disease area | Breakthrough | Indication & mechanism | List price US | List price UK |

| Metabolic disease | Wegovy (semaglutide 2.4 mg) | Obesity; GLP-1 receptor agonist | USD 1,350/mo26 | NHS: GBP 73/mo (USD 98/mo) (lower dosages; high dosage price undisclosed)27 Market price: GBP 99–199/mo (USD 133–267/mo) (from lowest to highest dosage) 28 |

| Zepbound (tirzepatide 15 mg) | Obesity; GIP/GLP-1 receptor agonist | USD 1,086/mo29 | NHS: GBP 92–122/mo (USD 123– 64/mo) (from lowest to highest dosage) 30 | |

| Rare disease | Casgevy (CRISPR gene edits) | Sickle cell disease/β-thalassemia; ex vivo cell therapy | USD 2.2 million (one time)31 | NHS: price undisclosed |

| Oncology | Kimmtrak (tebentafusp) | Human leukocyte antigen target for melanoma | USD 18,760/vial32 | NHS: price undisclosed |

| Autoimmune | Tzield (teplizumab) | Delay onset of stage 3 type 1 diabetes; anti-CD3 anti-body | USD 13,850/vial (14 vials USD 193,900/ course)33 | NHS: price undisclosed |

| Cancer diagnostic | Galleri (MCED blood test; liquid biopsy) | Multi-cancer early detection via cell-free DNA analysis | USD 949 per test (US self-pay)34 | Private access only, no NHS tariff (trial ongoing) |

| Cardiovascular | Leqvio (inclisiran) | Lowers bad cholesterol via siRNA that silences PCSK9 gene expression | USD 9,750 USD (USD 3,250 per injection, 3x first year)35 | NHS: GBP 5,962 (USD 7,980) (first year, 3 injections)36 |

| Coronary diagnostic | HeartFlow FFRct (CT-derived fractional flow reserve) | Non-invasive coronary physiology from CT scans enhanced with contrast dye | USD 1,500– 2,950 (per case) | NHS: GBP 700 (USD 936) (per case)37 |

| Neurodegenerative | Leqembi (lecanemab) | Early Alzheimer’s; anti-amyloid antibodies that reduce protein aggregates in the brain | USD 26,500/year38 | NHS: price undisclosed Market price: GBP 20,000/year (USD 26,770) |

| Kisunla (donanemab) | USD 32,000/year39 | No NHS tariff |

Source: Geneva Association

2.3.1 Where payers shape the pace of innovation

“It is a well-cited fact that it takes an average of 17 years for scientific evidence to be fully integrated into routine clinical practice. This shows that medical innovation must be met with a plethora of enabling conditions for real-world adoption.”

Maulik Majmudar

Biofourmis

Even when a diagnostic or a therapeutic intervention is approved, in addition to some of the operational issues indicated above, payer bottleneck can delay equitable and routine access for years.40 Clinical experts have highlighted three prominent barriers to the adoption of medical innovations. Unsurprisingly, they are associated with the role of a payer:

- High costs of treatment, either through high demand (GLP-1s) or one-off costs (gene therapies), are straining public and private payers. For statutory health schemes, social insurance funds, and private health insurers alike, a surge in eligible patients seeking treatment at the same time can place severe pressure on annual budgets. For example, an estimated 12% of the US population have used GLP-1 therapies, according to a 2025 survey.41 On average, US health insurers pay between USD 467–512 per person in monthly claims. A single GLP-1 prescription can double that amount for an individual (see Table 1).42

- Reimbursement uncertainty of new therapies or diagnostics can create hesitation among treatment providers. Without predictable reimbursement, new therapies may remain limited to specialist centres or tightly controlled pilots.

- Misaligned patient-payer expectations are the gaps between what patients believe should be covered and what payers can reasonably fund based on evidence, regulation, and cost. This expectation misalignment makes balanced discussions difficult and obscures the practical constraints under which health payers (irrespective of if they are public or private) operate.

2.3.2 Where investors shape the priorities for innovation

While current medical innovations are constrained by payer and operational barriers, future medical advances are dependent on the availability and flow of financial capital for research and development (R&D).

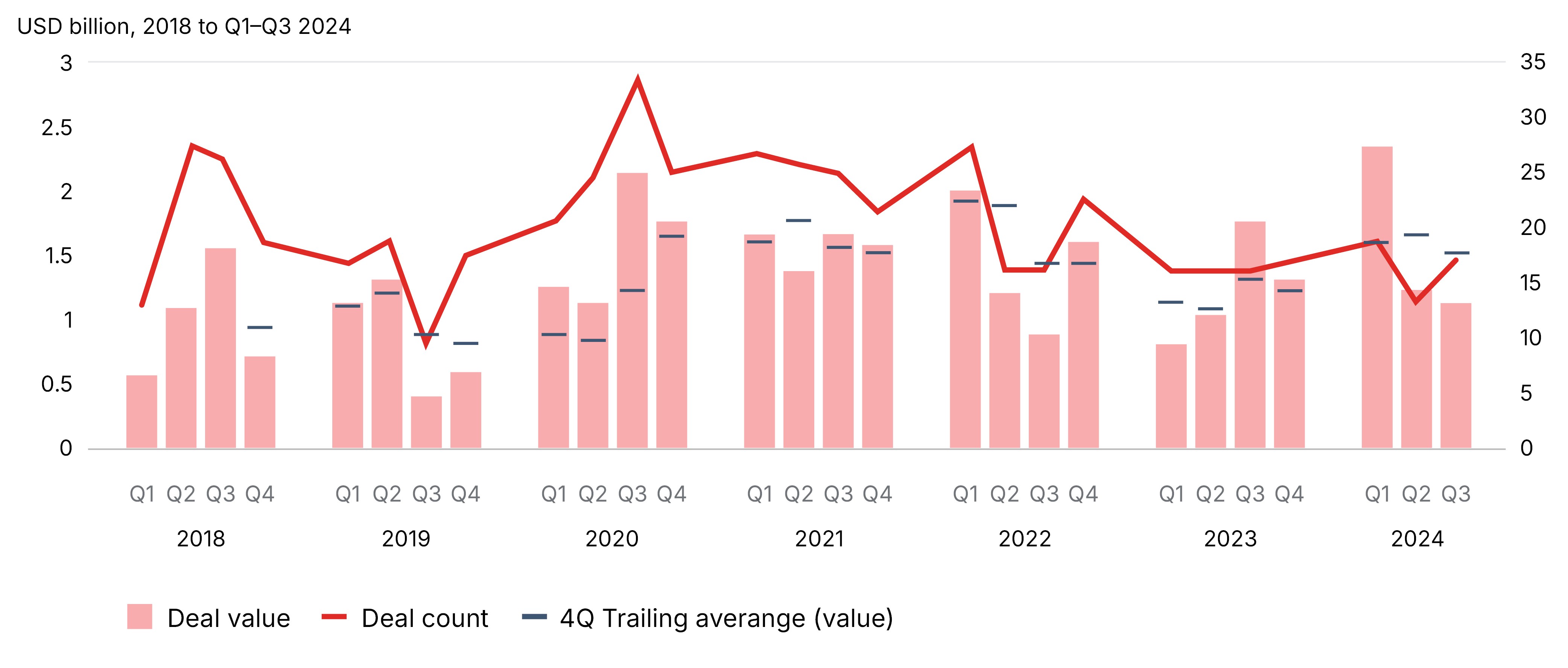

Venture capital (VC) investment in biotechnology showed clear peaks and troughs between 2018-2024 (Table 2). Using pharmaceutical company VC data as a proxy, both deal count and deal value rose sharply from 2019 and remained elevated through the pandemic period, peaking between 2020 and early 2022. Activities slowed through 2022 and 2023, followed by early indications of a recovery in 2024, although levels remain below the pandemic peak. Over these seven years, on average 37.4% of all VC investments by pharmaceutical companies were directed towards cancer.43,44

Figure 2: Trends in venture capital investment by pharmaceutical companies (2018–2024)

Notes: Deal value is full-deal value regardless of size of pharmaceutical CVC investment. Pharmaceutical CVCs included Amgen Ventures; Baxter Ventures; Boehringer Ingelheim Venture Fund; Lilly Ventures; M Ventures (Merk KGaA); MP Healthcare Venture Management (Mitsubishi Tanabe); MRL Ventures Fund (Merck & Co.); Novartis Venture Fund; Novo Ventures; Pfizer Ventures; Roche Venture Fund; Sanofi Ventures; SR One Capital Management (GSK); Takeda Ventures.

Source: Oliver Wyman 2024

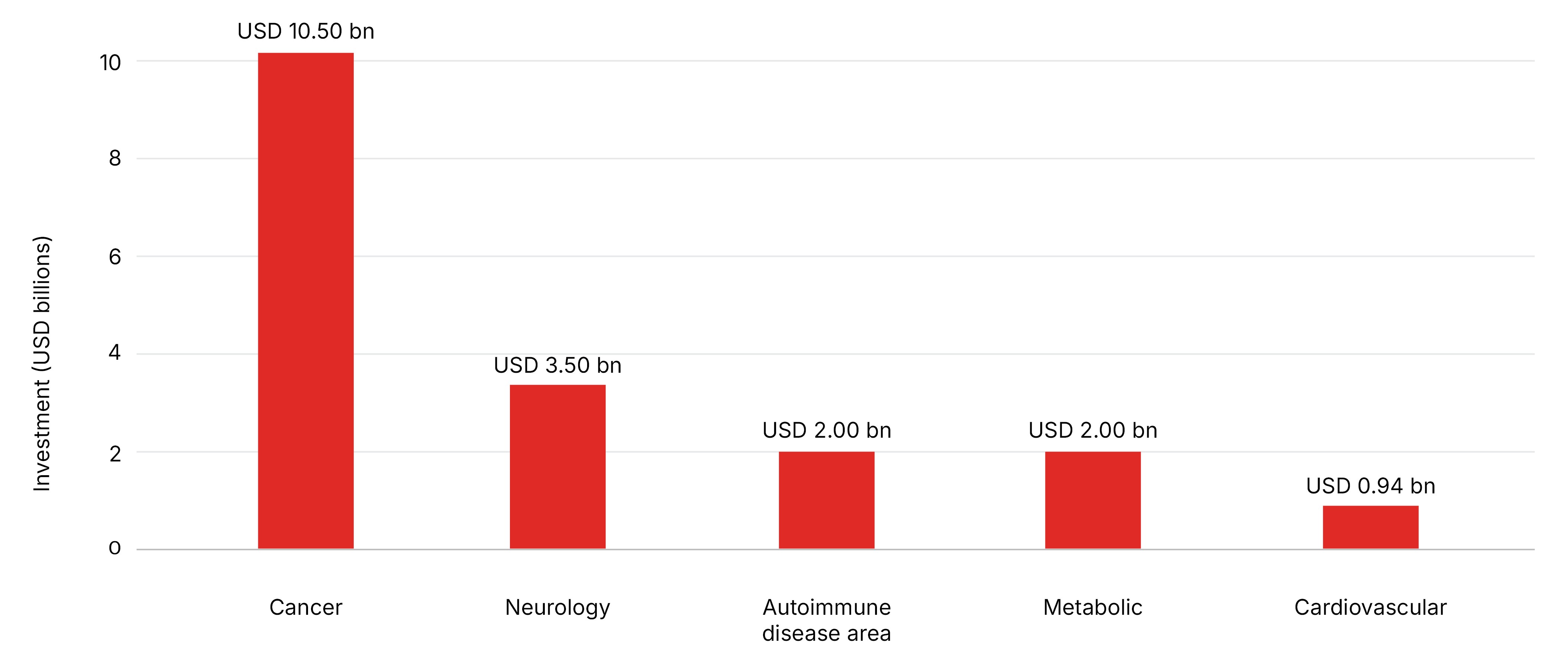

Figure 3. Value of venture capital funding by disease areas in 2023–24

Source: Compiled using DealForma’s 2023–24 venture-capital investment data

As shown in Figure 3, the dominance of cancer investment in particular, also becomes clear when looking beyond the pharmaceutical industry. Between 2023 and 2024, broader VC investment data shows that almost every major condition received less than half the level of cancer investment,45 even though many of these other areas play a crucial role in preventing future cancer diagnoses. This helps to illustrate the imbalance in capital flow by disease areas. Equally, areas of public health significance, such as broad-based prevention, generic antibiotics, or low-cost population screening tools, remain under-invested.

The innovation pipeline appears to have become skewed towards high-cost medical technologies, while preventative interventions and low-cost, population-based solutions have attracted relatively less financial backing. For health payers, this has two major consequences. Firstly, many heavily funded curative innovations, despite considerable clinical benefit, pass on high costs to healthcare payers. Secondly, prevention measures, which have the greatest potential to reduce long-term morbidity and mortality, attract far less investment. Both trends put pressure on the long-term sustainability of health systems.

Without strong incentives from payers or corrective measures by policymakers, investment is likely to keep flowing towards narrow, high-profit innovations. It could exacerbate a well-known healthcare market phenomenon, where, left to their own devices, pure market mechanisms do not funnel investments to the areas of greatest need or best value. The result could be big wins for a few, incremental gains for the many, and enduring gaps where health needs may be felt most acutely.

2.3.3 The innovation outlook

Medical innovation will most likely be impacted by the following trends:

- The largest near- or mid-term wins are in CVD, diabetes, and obesity. These are likely to be aided by GLP-1s, point-of-care wearables monitoring, greater use of CGM, and gene therapy for hereditary high cholesterol.

- Incremental gains in cancer, supported by infrastructure investments, will be aided by mRNA vaccines, CAR-T, and liquid biopsy. These may show gradual population-level impact owing to the need for specialised centres, more personalised testing, and delivery.

- Profound but narrow wins are occurring in rare diseases through gene or cell therapies. These are likely to have better effects at an individual patient level but may have a small population-level footprint.

- Neurodegenerative conditions and mental health are experiencing slow-moving developments, even though the latter has, in recent years, benefitted from digital innovations that enable greater population access.46

- Cross-cutting enablers, such as AI in diagnostics and point-of-care wearables, may enable earlier interventions but require policy and workflow considerations, as well as behaviour change, to realise their full value.

Implications of medical innovations for L&H insurers

This section analyses the implications diagnostic and therapeutic breakthroughs may have for the biometric risks managed by L&H insurers. The analysis draws on insights from 18 senior insurance executives from Europe, Asia, and the Americas.

How soon will diagnostic breakthroughs affect insurance?

Diagnostic innovations – including AI-enhanced diagnostic imaging, liquid biopsies to screen or monitor specific cancers, and consumer-accessible testing – are expected to have the strongest near-term impact on L&H insurance. These technologies will likely enable earlier disease detection and improve underwriting accuracy. They will also support early intervention, help manage rising healthcare costs, and contribute to healthier risk pools, ultimately reducing claims.

In the long-term, liquid biopsies, particularly in the form of MCED, are expected to mature and become the standard of care to identify the presence of multiple cancers. As these technologies are refined and gain the ability to detect harder-to-diagnose cancers – such as pancreatic, ovarian, liver, and lung cancers – where prognosis is often poor, they should enable earlier intervention, and more targeted and potentially less invasive and repetitive clinical follow ups. This, in turn, is likely to improve patient outcomes, while placing downward pressure on healthcare costs. Beyond MCED, advances in genomic medicine are also expected to accelerate highly personalised approaches to predicting and understanding individual health risks.

How soon will therapeutic breakthroughs affect insurance?

There is a wide range of opinions among insurance experts on when and to what extent novel therapeutic breakthroughs may influence L&H insurance. However, the majority expect considerable disruption within five years, contributing to a sense of urgency in framing the issues and charting the course ahead.

GLP-1 receptor agonists are considered highly transformative, mitigating not only the health risks related to obesity, but also potentially Alzheimer’s, reshaping morbidity, mortality, and the quality of longevity. This is not least because the GLP-1 therapies market is projected to grow rapidly and materially influence life expectancy.47,48 Widespread adoption could reduce cumulative all-cause mortality, with optimistic estimates ranging between 6.4% and 8.8% by 2045 in the US alone.49,50

Cancer therapies are also seen as disruptors, albeit with a slower timeline than GLP-1. However, any sudden advances or breakthroughs in targeted cancer therapies could put upward pressure on health insurance claims costs.

In the long term, cell and gene therapies, despite their implementation-related risks, could significantly shift healthcare delivery from treating illness to modifying or eliminating inherited predispositions. The widespread adoption of hyper-personalised therapies would have implications for L&H insurance risk pools, mortality assumptions and pricing models (see Sections 3.3 and 4).

How will life and health insurance product lines be affected?

3.3.1 Health insurance

High-cost treatments, such as gene and cell therapies, alongside volume-driven expenditure for anti-obesity drugs, may exert stress on health insurance premiums and coverage limits. A small number of extremely costly treatment episodes and claims linked to one-off curative gene therapies, or a high volume of more moderately priced but recurrent episodes and claims for GLP-1 therapies, may prove difficult to sustain at scale. Traditional pooling mechanisms could have difficulty coping with such claims volatility, especially as technical underwriting margins in health insurance tend to be narrow. The US National Association of Insurance Commissioners states the loss ratio for health insurance was 89% in 2024 compared 86.7% and 85% in 2023 and 2022, respectively.51,52,53

There are also opportunities. Early detection of diseases, such as diabetes, may enable faster interventions and reduce the need for costlier hospital or specialist care. For the case of diabetes, GLP-1 therapies can be prescribed to help manage pre-diabetes and lower the chances of progressing to type 2 diabetes. This gives health insurers the option of focusing support on those most at risk, through a wrap-around service that combines medication with lifestyle programmes and coaching. Such an approach may help people stay healthier for longer, slow the onset of disease, and reduce healthcare costs over time. Moreover, as generic forms of GLP-1 drugs arrive post-patent expiry, and oral substitutes replace current injectables,54 broader access and lower drug costs could improve claims dynamics.

“In health insurance, the short-term costs of GLP-1s often speak louder than long-term benefits – yet the real challenge lies in balancing both.”

Steve Woh

RGA

Developing this type of wrap-around service requires upfront investment, which private health insurers may find hard to justify. This is largely because the regular movement of policy holders between insurers reduces the time available to recoup the benefits of longer-term investment in prevention and health improvement.

However, churn can operate in both directions. A 12-year longitudinal study from the US, using data from a large commercial health insurer, showed that among the members who disenrolled from the insurer, over a third (34%) re-enrolled within five years of leaving. This number rose to 47% after 10 years,55 suggesting churn may not undermine the case for investment. Healthier individuals may move between insurers over time, potentially strengthening overall risk pools across the private health insurance market.

3.3.2 Life insurance: Mortality protection

For traditional life insurance, diagnostic and therapeutic breakthroughs represent a largely positive shift. Advances in cancer therapies, as well as other gene and cell therapies, could reduce mortality and potentially expand the insurable pool (as conditions become manageable or curable). Once-excluded individuals may qualify for standard rates or more precise premium loadings. Over time, these changes could also affect annual mortality improvement assumptions and require pricing recalibration, as with GLP-1 estimates previously discussed.

Predictive and diagnostic innovation also creates new opportunities for consumer engagement. Life insurance has historically struggled to connect with policyholders, often interacting only at policy inception and/or at the time of a major claim. Embedding repeatable diagnostics, continuous biomarker monitoring, as well as prevention and lifestyle advice into insurance services, offers pathways to create more customer touchpoints in order to increase relevance and trust. These services can encourage healthier behaviours, improve health outcomes, reduce lapse rates, and reinforce the perceived value of cover, giving life insurers a chance to shift from passive claims payers to active partners in well-being.

3.3.3 Life insurance: Living benefit products

For longevity-based life insurance products (e.g. annuities), longer lifespans may increase annuity and pension payouts, create financial strain and require recalibration of underwriting assumptions.56 Conversely, healthier and more productive lives, enabled by medical breakthroughs, extend potential working years – prolonging accumulation, and shortening decumulation phases (i.e. the stage of life where life savings are expended, sometimes significantly, on health).

Critical illness (CI) insurance is directly exposed to new diagnostics and therapies. Earlier detection through AI-enhanced diagnostic imaging or liquid biopsies may increase early-stage claims and put pressure on lump-sum claim triggers, typically paid when the criticality (severity) of diseases manifest. The frequency of claims may change as diagnostic tools become more accessible and as population-based screening programmes develop, as seen with thyroid cancer in South Korea.57 Moreover, CI product definitions may come under scrutiny as newer forms of diagnostics are deployed, prompting questions about which medical interventions constitute a diagnosis and thus a payment trigger.

“MCED tests have the potential to reclassify risk, and we may have to rewrite what health and critical-illness insurance looks like."

Ana Luisa Villanueva Alonso

Mapfre Re

For long-term care insurance (LTCI), any future breakthroughs in dementia treatments could reshape morbidity and influence the structure of LTCI products. Similarly, predictive diagnostics may help raise awareness of genetic or health predispositions and encourage financial planning among policyholders, offering insurers an opportunity to design innovative products that could share the risks and costs associated with ageing between insurers and insureds. This could, in turn, narrow the protection gap typically seen in LTC and help to reduce old age poverty.58,59

Improved disease recovery rates through novel therapies could reduce the long-term prevalence of certain claims in income protection or disability protection insurance. For instance, anti-obesity treatments may lessen the incidence of musculoskeletal conditions, while advances in mental health interventions could alleviate psychological burdens, both of which are among the leading causes of disability claims.60

Where next? How medical innovations could affect insurability

Medical innovation is reshaping what can and cannot be insured. In some cases, it expands insurability, allowing new groups of people or new risks to be covered. In other cases, it brings challenges, including higher costs and greater certainty/predictability of some predisposed health risks. Taken together, these changes offer insurers an opportunity to rethink their role within this rapidly evolving innovation ecosystem, rather than simply responding to its future consequences.

“Integrated healthcare is the solution to soaring drug costs and shortages of medical professionals – a team-based approach that breaks down silos, lets AI take care of administrative tasks, and ensures every patient receives the right treatment at the right time.”

Alfred Beil

AXA

Figure 4: Insurance functions that need to change

Source: Geneva Association

Discussions with insurance experts reveal three areas of focus for L&H insurance (Figure 4). The immediate priorities are product design and evolution, given the rising cost of new treatments and the shifting risk profiles of policyholders. For instance, should health insurance include whole-body scans as an additional benefit? Although such features may enhance market appeal, research suggests that these scans provide limited clinical value,61 can trigger unnecessary follow-up tests (and costs), and may expose individuals to avoidable radiation risks. These choices also have market-wide consequences, as one market leader could compel other players to follow, and there could be a negative impact on medical inflation.

Underwriting, risk pooling, provider payment arrangements and navigating regulation are emerging priorities. As new diagnostics and therapeutics are deployed, their direct and indirect implementation costs, together with the need for ongoing performance monitoring, will require fundamentally new approaches to risk management and the policy frameworks that govern them.

Over the long-term, transforming L&H insurance will require new skills and new ways of engaging with customers. This is not a gradual change. It requires new ways of operating, often in close collaboration with governments, pharmaceutical companies, health economists and, at times, other insurers. Insurers will also need to find innovative ways to communicate with their customers, both building trust and raising awareness of understanding and managing their biometric risk. Customer engagement can encourage a willingness to share data, a critical enabler in transforming underwriting from static to dynamic.

Building on these expert inputs, the remainder of this chapter presents an integrated analysis of five key areas that merit deeper exploration and dialogue.

What and how much to cover?

Public entities play an important role in many countries in developing evidence-based guidelines for health policymakers and payers to critique the value of medical innovations. These entities, often referred to as health technology assessments (HTA) agencies conduct systematic evaluations of new medical technologies to guide reimbursement decisions. They differ by country in their emphasis on cost and clinical effectiveness.62 Examples of such agencies include the Institute for Clinical and Economic Review (ICER) in the US, the National Institute for Health and Care Excellence (NICE) in the UK, and Haute Autorité de Santé (HAS) in France. Insurers, including life insurers offering value-added health benefits based on available treatment for certain conditions, could consider how HTA decisions could guide product design, clinical pathways, and claims limits.

Insurance experts also voice the need for an L&H industry-wide agreement on value-adding predictive and diagnostic tests, as well as therapies that add little or no value. Achieving such a consensus could reduce waste through more targeted prescriptions of diagnostics and treatments, the elimination of harmful practices, and an improvement in clinical standards to deliver better health outcomes.

“There are great models to leverage risk pools to create certainty, predictability and value for purchasers, but pooling risk is not sufficient to solve the sustainability problem for transformative therapies. Insurers, as purchasers, increasingly need to play a central role in deciding which innovations are genuinely in the interest of policyholders and which innovations offer little value."

William Shrank

Aradigm (formerly of Humana)

“This is a clear opportunity for the insurance industry to come together and define what is truly worth covering – and to call out the gimmicks that add little or no value for consumers.”

Ana Luisa Villanueva Alonso

Mapfre Re

How should product design evolve?

The emergence of high-cost curative molecular therapies, such as CAR-T cell therapy, CRISPR genetic therapy and cancer vaccines, pose challenging decisions about the allocation of resources across the full continuum of care. High-cost therapies emphasise the need of embedding prevention at the centre of insurance product design to reduce the reliance on expensive interventions, where possible.

While the current R&D investment pipeline appears weighted towards expensive curative approaches, preventative services, risk monitoring, and proactive health management can often be clinically more effective. Research shows that environmental and lifestyle factors explain substantially more variation in mortality risk than PRS-based genetic risk, which accounts for only a small fraction of variance.63 Health insurers can send a clear financial signal to investors by choosing what to prioritise and cover as benefits for their customers, and so influence a more balanced capital flow across curative and preventative innovations.

In the case of CI insurance, as population-based cancer screening programmes (aided by the gradual maturity of MCEDs) begin to accelerate, insurers will have to decide how to mitigate the risks of early and frequent claims described in Section 3. This will require updating definitions for diagnoses and disease severity, as well as determining if payments are triggered as lump sums or are staggered. Such revisions will be crucial to maintain relevance of the coverage without compromising product sustainability.

How should underwriting adapt?

L&H underwriting will increasingly need to become more dynamic, adapting to individuals’ changing health risk profiles over the term of the policy. Such a continuous underwriting approach can also create new opportunities for consumer engagement, providing insurers with more meaningful touchpoints with policyholders.

At the same time, emerging diagnostic techniques and personalised medicine are creating smaller and more precise risk groups – in some cases almost down to the individual. While lower-risk individuals may see reduced premiums, insurance could become increasingly expensive for those at higher risk. This creates ethical and societal challenges, particularly in the importance of maintaining affordable access to coverage for vulnerable groups.

Information asymmetry between policyholder and insurer may be another emerging challenge, resulting in potential adverse selection, where policyholders may know more about their health risks when seeking protection than the insurer. This directly implicates disclosure arrangements and health data. For example, a GLP-1-induced weight loss episode not disclosed to an insurer at the point of application may mean that the (static) biomarkers understate future risk, if treatment is discontinued and weight is regained. Similarly, direct-to-consumer diagnostics kits and services may result in customers knowing more about likely future health outcomes than their insurers.

“Globally, the industry aims to cut friction and ease sales by reducing requirements and tests. Yet as predictive diagnostics give applicants greater insight into their risks, insurers may need more testing to stay on equal ground. We must find a way to balance consumer benefit with accurate underwriting.”

John Schoonbee

Swiss Re

How can insurers overcome the limits of traditional pooling and purchasing arrangements?

“Rapid medical innovation is driving up drug costs, making many treatments prohibitively expensive for most patients – even when they are the most appropriate option. Global reinsurers could help make such high-cost treatments more manageable and sustainable through risk smoothing and sharing, drawing on their expertise in natural catastrophe risk management.”

Achim Regenauer

Partner Re

The price volatility introduced by some expensive therapies is considerable. This volatility reflects not just direct costs, but the speed of treatment uptake by health systems, and public demand. Traditional risk pooling, even when supported by advanced underwriting techniques, may struggle to cope with sudden treatment cost shocks. Insurers can explore alternative ways of pooling risks, as well as novel purchasing arrangements (as summarised in Table 2), to help negate price volatility.

The US has previously used public mechanisms to manage very high healthcare costs, offering potential lessons for reinsurers elsewhere. One example was the Affordable Care Act’s transitional reinsurance programme, a temporary federal scheme that operated from 2014 to 2016 and provided insurers with stop-loss-style protection against very high claims.64 While this programme has ended, several US states now operate their own reinsurance schemes under federal waivers.65 A small number of private US reinsurers now also offer stop-loss guarantees to limit the losses of primary carriers or self-insured health plans. Some do this in the form of a subscription-based model, involving a fixed per-member, per-month payment, to enable a primary carrier secure access to high-cost therapies or manage unexpected claims emerging from them.66 The value of a subscription-based model for insurers/payers is the conversion of risk volatility into predictable expense.

New purchasing arrangements that align provider payments with clinical outcomes are also emerging under the broad umbrella of value-based payment. In parallel, collective negotiations with suppliers of new therapeutics are becoming more common under the remit of outcome-based contracting. For instance, performance-based annuitised payment models spread the payment of treatment cost to providers over multiple years based on their effectiveness.67 These models are notable for disease-specific funds or pools that create a controlled environment (sandbox) in which therapeutic innovations can be evaluated in real-world settings. This provides payers greater influence over market entry and provider performance, while maintaining cost control. The UK’s Cancer Drugs Fund exemplifies this approach and similar policy considerations are underway across many OECD countries.68,69 Similarly, partnerships for drug pricing, such as those surrounding the market entry of Zynteglo for thalassaemia, have strengthened the bargaining power of payers, while promoting common standard-setting and assuring the supply of these medicines.70

TABLE 2: A SIMPLIFIED SCHEMATIC OF EMERGING RISK POOLING AND PURCHASING MECHANISMS

Emerging models/features | Reinsurance | Subscription model | Annuitised payment | Disease-specific price negotiations |

| Insures against | Low frequency catastrophic claims risk | Volume risk | Upfront budgetary shock and performance risk | Price volatility |

| How it functions | Excess cover for unexpected claims from (defined) therapies through stop-loss arrangements | Periodic fixed fee to access high-cost therapies | Costs spread over several years, which can also be performance-linked | Payers (including insurers) negotiate terms in defined disease areas using collective bargaining |

| Risk pooling | Yes, risk transferred to reinsurer | Yes, at payer level, based on anticipated demand | No, it is a contracting mechanism | No, essentially a procurement arrangement |

| Implications for health insurance | Protects solvency, especially for rare or high-cost cases | Predictable costs but there is a risk of getting projections wronG | Eases affordability but adds long-term liabilities and the need to follow clinical outcomes | Improves access and bargaining power, but limited to selected conditions |

| Implications for life insurance | May improve insurability for conditions that were previously excluded, for example, lifelong conditions cured by gene editing | May improve insurability for conditions Could affect mortality/longevity projections if uptake is widespread | May improve insurability for conditions Could affect mortality/longevity projections if uptake is widespread | N/A |

Source: Geneva Association

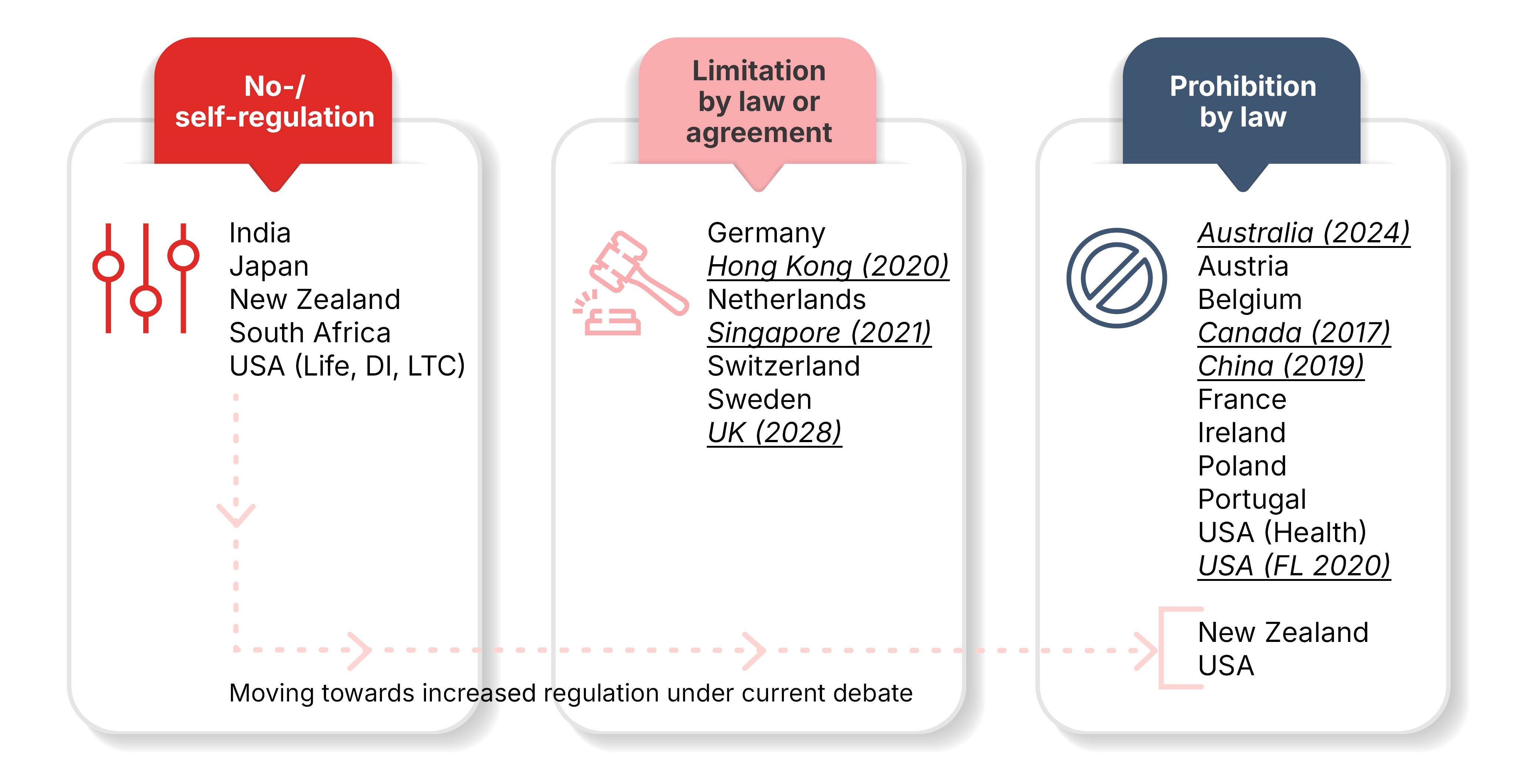

Navigating the regulatory tension ahead

Access to sensitive genetic data (predictive and diagnostic) remains unevenly regulated across jurisdictions (Figure 5). A recent Swiss Re report71 noted that while some countries have limited regulation, most enforce restrictions ranging from narrow permissions to outright prohibitions. However, the regulatory landscape is evolving rapidly. For instance, in the UK, insurers are generally barred from using predictive genetic test results, with the narrow exception of Huntington’s disease, in high-value life insurance cover.72 Similar high-sum insured exceptions apply in Hong Kong, the Netherlands, Singapore, and Switzerland amongst others. In Australia, the government launched a consultation in 2025 on proposals for a complete ban on the use of genetic data.73