Public-private insurance programmes (PPIPs) can help narrow protection gaps by improving insurance availability, affordability and uptake for risks that are difficult for private markets to absorb alone.

Suggested citation

Geneva Association. 2026.

Addressing Growing Protection Gaps through Better Public-Private

Insurance Programmes.

Author: Hélène Schernberg. February.

3 min read

Key Findings

-

-

Analysis of 14 established PPIPs shows that well-designed programmes can stabilise insurance markets and expand coverage, but may also create significant fiscal liabilities and crowd out private-sector participation.

-

PPIPs are most effective when governments act as reinsurers of last resort, covering extreme losses while allowing private insurers to retain a sustainable share of risk.

-

Successful PPIPs balance social, fiscal, market and operational objectives by ensuring affordable access to coverage, protecting public finances, supporting private insurance markets and enabling rapid claims payments.

-

PPIPs should form part of a broader resilience strategy that prioritises risk reduction, rather than serving solely as mechanisms for post-disaster compensation.

Q&A

-

What is this report about and what are its main findings?

This report examines the role of public-private insurance programmes (PPIPs) in addressing growing insurance protection gaps. Drawing on analysis of 14 established programmes covering risks such as natural catastrophes, terrorism, cyber incidents and pandemics, it finds that PPIPs can improve insurance availability, affordability and uptake. However, they must be carefully designed to avoid excessive fiscal costs, crowding out private insurance markets and weakening incentives for risk reduction.

-

Why do public-private insurance programmes matter?

As disasters become more frequent, severe and costly, many risks are becoming harder to insure through private markets alone. PPIPs can help maintain access to affordable insurance by sharing extreme losses across society and providing government-backed support for risks that exceed the capacity of private insurers. They can therefore play an important role in strengthening societal resilience and reducing insurance protection gaps.

-

What are the implications for insurers and policymakers?

The report highlights the importance of preserving a strong role for private insurance markets when designing public-private insurance programmes. For insurers, well-designed PPIPs can improve the availability and affordability of coverage for difficult-to-insure risks while maintaining incentives for private-sector participation and innovation. For policymakers, the challenge is to target government intervention where it is genuinely needed, protect public finances and ensure that PPIPs complement broader efforts to reduce risk and strengthen resilience.

-

What are the four guardrails for designing a public-private insurance programme?

The report identifies four guardrails that can help ensure PPIPs achieve their objectives while remaining sustainable over time. The social guardrail focuses on providing fair access to coverage at affordable prices. The fiscal guardrail seeks to protect public finances by limiting the state's role to that of a reinsurer of last resort. The market guardrail encourages private-sector participation and ensures insurers retain a sustainable share of risk. The operational guardrail emphasises the importance of paying claims quickly and efficiently after a loss.

-

Can public-private insurance programmes help reduce disaster risk?

Yes, but only if they are designed to support resilience as well as risk sharing. The report argues that PPIPs should not function solely as financial mechanisms that compensate losses after disasters occur. They should also encourage investments in prevention, mitigation and risk reduction. By reinforcing incentives to reduce exposure and vulnerability, PPIPs can help keep risks insurable over time, strengthen societal resilience and reduce pressure on public finances following major events.

7 min read

Author

Hélène Schernberg, Director Public Policy & Regulation, Geneva Association

Introduction

The disaster protection gap – the uninsured share of economic losses from natural and man-made disasters – is widening. Between 1980 and 2025, natural catastrophes caused an estimated USD 7.4 trillion in property losses, of which two thirds were uninsured.1 Uninsured losses impede economic growth and push governments into slow, unpredictable, and budget-destabilising post-disaster relief.2

Investing in risk reduction – measures that prevent or mitigate losses and support recovery and adaptation – is often more cost-effective than rebuilding. In addition, insurance can spread remaining losses and provide rapid, pre-arranged liquidity that keeps firms open, preserves jobs, and reduces the need for ex-post fiscal support.

In some regions and for some perils, however, private-market mechanisms do not generate enough risk reduction or insurance coverage. Government intervention can help narrow the disaster protection gap to an efficient and socially acceptable level.

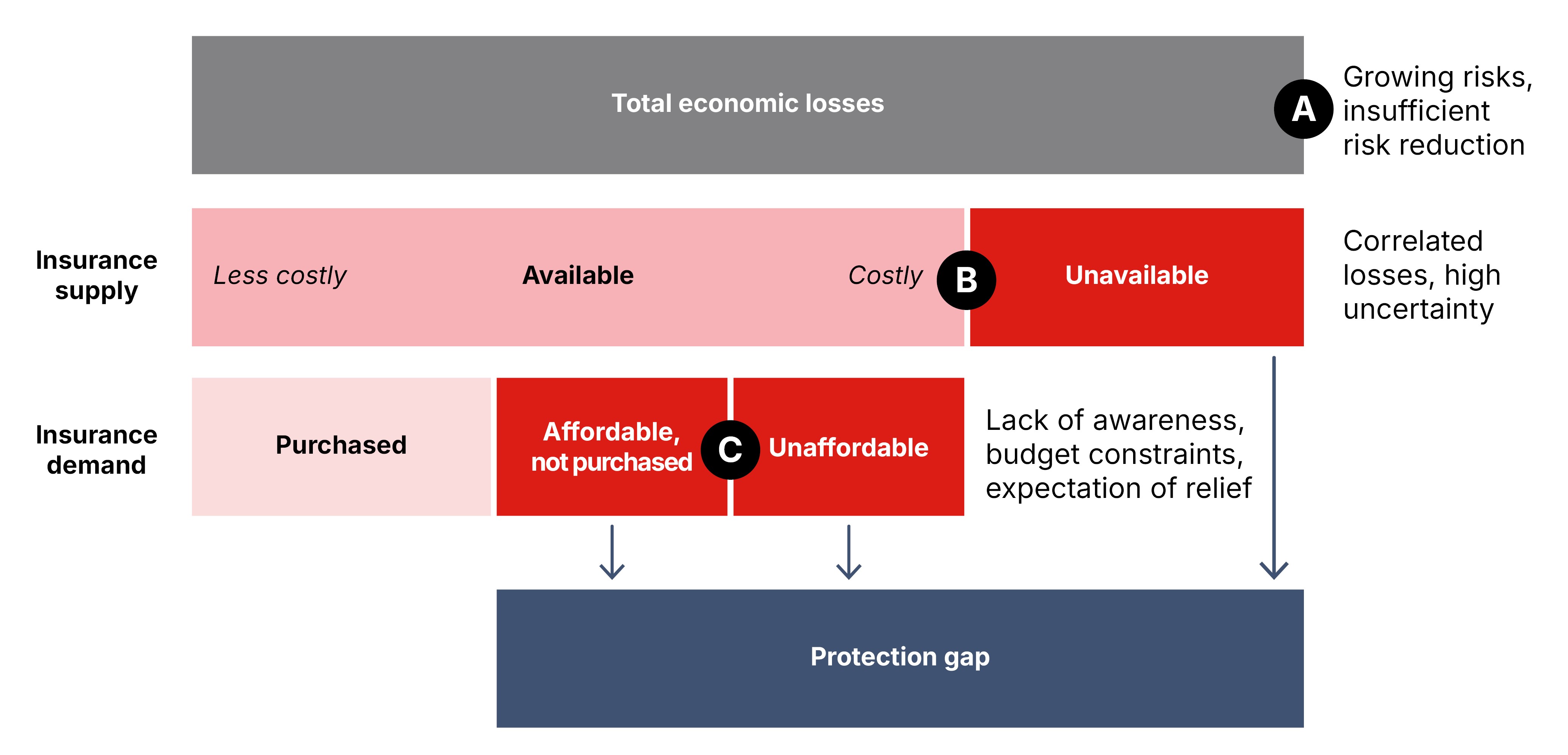

Causes of the protection gap

Three market frictions drive the gap:

A. Increased losses: Climate change and technological progress intensify hazards while urban concentration and digitalisation increase exposure. Ageing infrastructure, weak building codes, and insufficient investment in risk reduction increase vulnerability.

B. Insufficient demand: Individuals underestimate the likelihood of rare events or expect government relief, reducing the perceived need for insurance. For low-income groups, premiums can be prohibitively expensive. Moreover, factors like financial-literacy levels impact demand.

C. Supply uncertainties: Highly correlated losses and significant uncertainty or ambiguity increase regulatory capital requirements, forcing insurers to charge higher premiums or to withdraw coverage. Inflation and price regulation further erode profitability and availability.

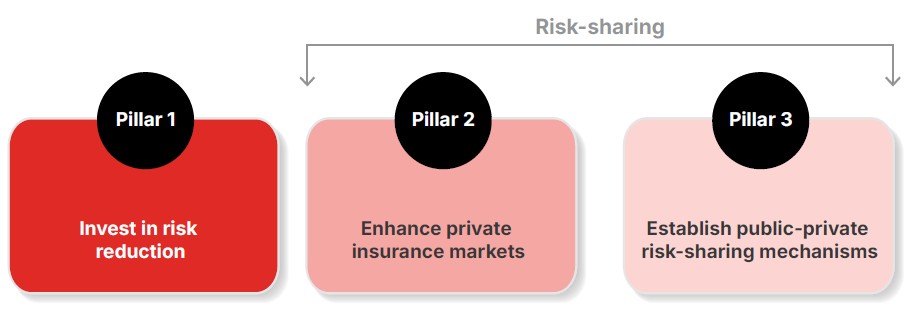

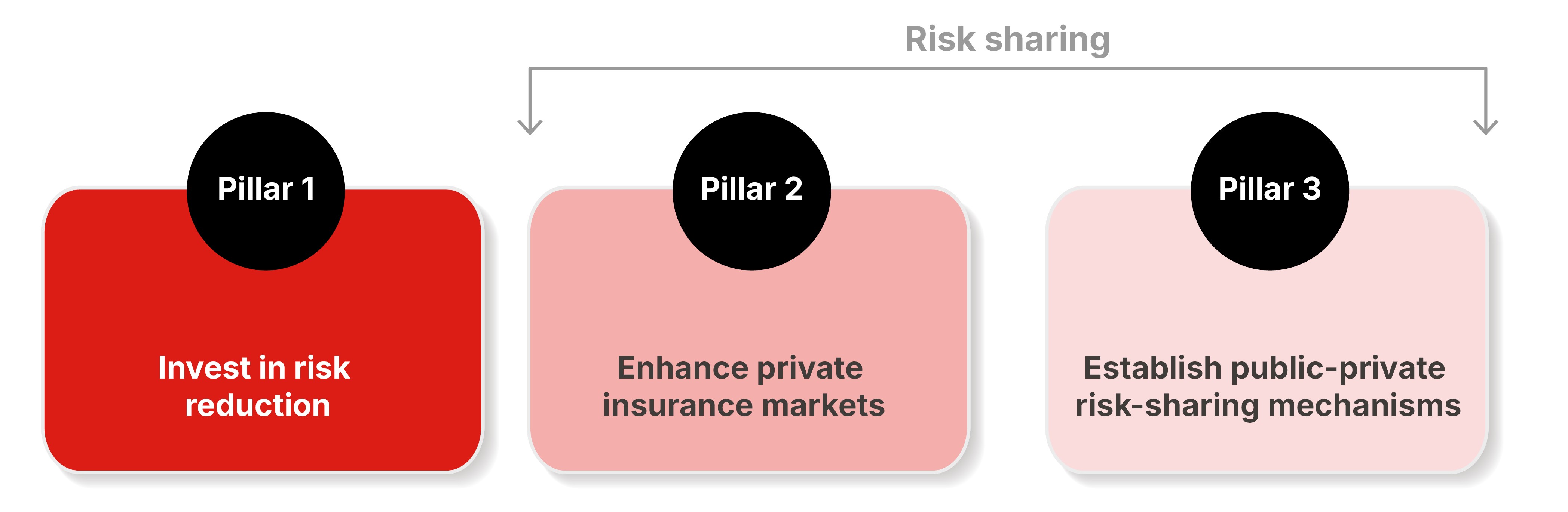

A three-pillar strategy

This report proposes a proactive, three-pillar strategy to narrow disaster protection gaps:3

- Pillar 1: Invest in risk reduction. Governments can both invest in infrastructure and create risk-reduction incentives, such as land-use planning or building codes, as well as provide financial support and information.

- Pillar 2: Enhance private insurance markets. Targeted policy actions, such as awareness campaigns, insurance mandates, or supportive regulation can support private capacity and encourage demand growth without distorting markets.

- Pillar 3: Develop public-private risk-sharing mechanisms. In some regions and for some perils, collaboration between the re/insurance industry and the public sector – often implemented as a Public-Private Insurance Programme (PPIP) – can lead to more efficient risk-sharing.

Figure 1: A proactive strategy with governments relying on three pillars to reduce and share risks

Source: Geneva Association, adapted from Zurich Insurance Group

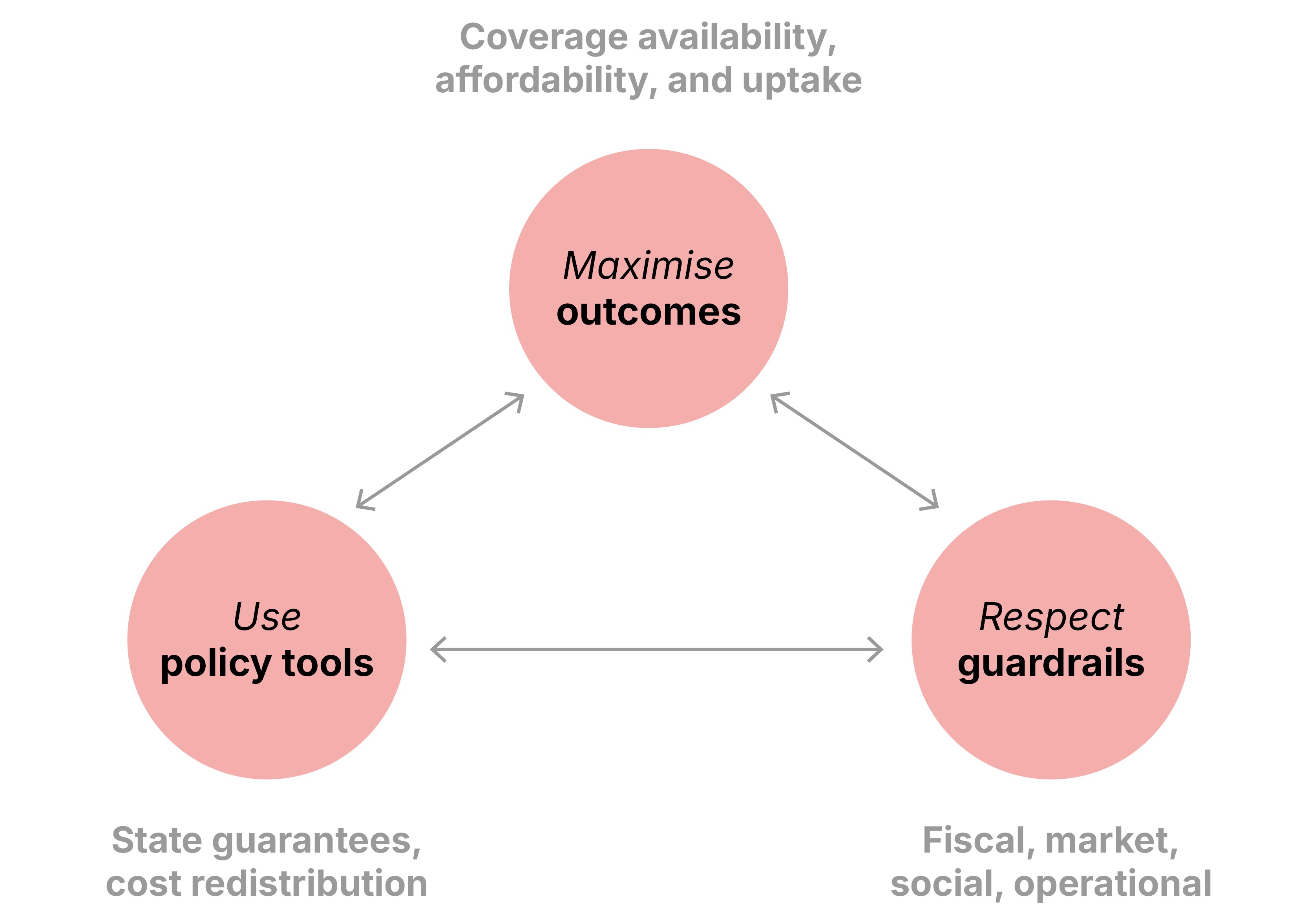

PPIPs: A conceptual framework

A PPIP aims to improve three outcomes: coverage availability, affordability, and uptake. Policymakers rely on two main tools: state guarantees to boost supply (availability); and cost redistribution – including insurance mandates and solidarity pricing – to support demand (affordability/uptake). Four guardrails constrain how policymakers use these tools:

- The fiscal guardrail aims to limit large, long-term burdens on public finances.

- The market guardrail aims to avoid crowding out private capacity or stifling competition and innovation.

- The social guardrail ensures affordability and an acceptable cost of coverage for vulnerable groups.

- The operational guardrail requires a fast claims-paying ability and adaptability to changing risk and market conditions.

The policy tools may stretch one or more guardrails, potentially requiring complex policy trade-offs. Strengthening the social guardrail though solidarity pricing improves affordability and uptake but can dampen risk signals, challenging the market guardrail. Over time, unmitigated risks might stress the fiscal guardrail. Likewise, state guarantees can crowd out private re/insurers, stifling the innovation and competition intended by the market guardrail.

Figure 2: PPIP design: an optimisation problem

Source: Geneva Association

PPIP archetypes: Tailoring the solution to the protection gap

This report analyses 14 existing PPIPs across natural and man-made perils (terrorism). They balance policy trade-offs in two archetypal ways:

- Market stabilisers focus on supply. They restore or maintain private-market capacity amid extreme uncertainty through state guarantees. By providing missing capacity, they encourage private insurers to remain in the market. Examples include the US California Earthquake Authority and Terrorism Risk Insurance Program (TRIP), and the UK Pool Re.

- Coverage expanders focus on the demand side of the protection gap. They typically combine state guarantees with cost redistribution to create capacity while lowering prices in high-risk areas. Examples include France’s CCR, Spain’s CCS, the UK’s Flood Re, and New Zealand’s NHC.

Successes and challenges

While market stabilisers provide coverage availability and price stability, they depend on voluntary participation and risk-based pricing. Significant protection gaps can remain: for example, just 4% of UK small businesses have terrorism coverage.4 Additionally, some PPIPs do not address contemporary risks, such as cyber threats or intangible asset losses.

Coverage expanders, combining mandatory participation with solidarity pricing, can reach uptake of 90–95%, such as in France and Spain. Voluntary programmes are less successful, as evidenced by opt-out rates from the US National Flood Insurance Program (NFIP).5

Many PPIPs stretch one or more guardrails. Some experience severe fiscal strain, including fund depletion at France’s CCR after recent droughts, the US NFIP’s enormous debt burden, and New Zealand’s Natural Hazard Commission (NHC) following multiple earthquakes. Market distortions arise when the PPIP crowds out private capacity, as in France. Flat rates can favour wealthier households in exposed regions, while risk-based pricing proposals in the NFIP (US) have triggered political backlash. Some schemes have faced high operational loss ratios, as recently seen in Australia’s Cyclone Reinsurance Pool.

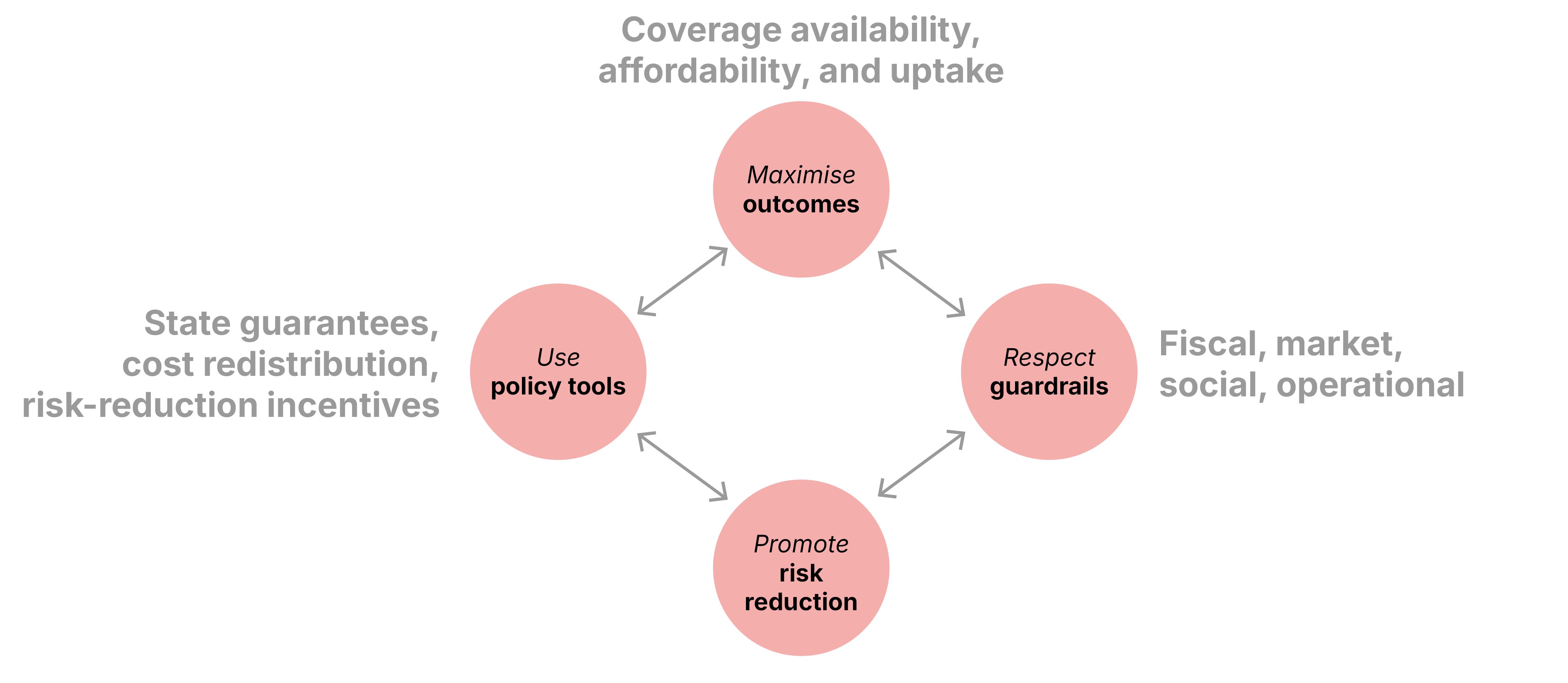

From sharing risks to supporting risk reduction

Pillar 3 (PPIP) interventions frequently precede or replace Pillar 1 (risk reduction) strategies. Flood Re (UK) is accused of allowing the government to defer flood prevention measures, while US NFIP flood insurance subsidies have encouraged population growth in high-risk areas.

Policymakers should view PPIPs as part of a broader resilience strategy rather than as isolated financial mechanisms. PPIPs should not only share post-disaster losses but also support – not undermine – public and private efforts to reduce exposure and vulnerability. While a PPIP can incentivise individual behaviour, government actions, such as infrastructure investment, have the greatest risk-reduction benefits, emphasising the need for government dialogue with the PPIP.

Figure 3: PPIPs must balance coverage outcomes (Pillar 3) and risk-reduction (Pillar 1)

Source: Geneva Association

Decision process and design principles

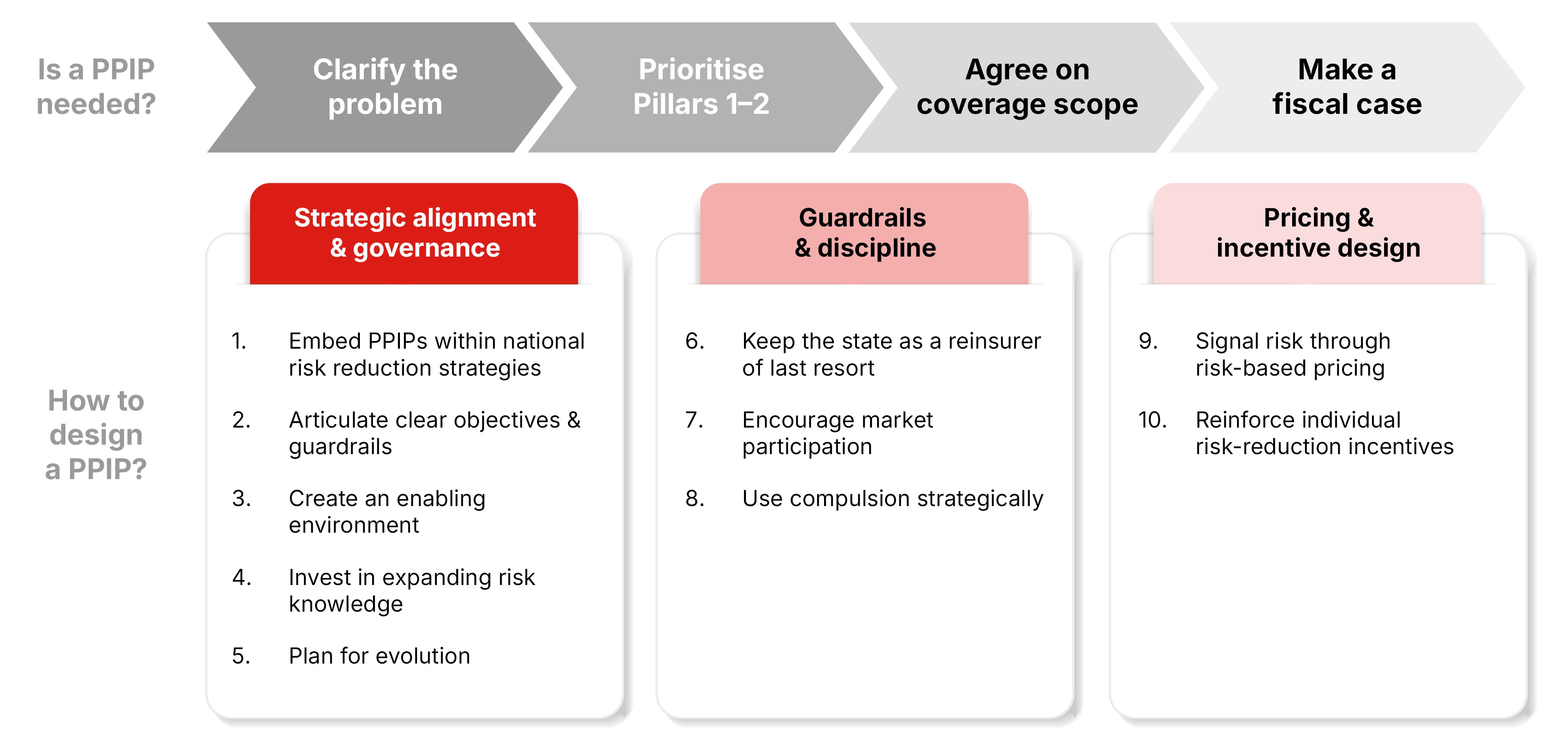

PPIPs are costly and complex. A four-step process can assess the need for and potential role of a PPIP:

- Substantiate the protection gap and the underlying drivers on the risk, supply, and demand sides.

- Prioritise non-distortive measures to reduce risks (Pillar 1) and enhance private insurance markets (Pillar 2).

- Agree on the perils and exposures a PPIP should cover, ensuring that remaining protection gaps are societally acceptable.

- Make a clear fiscal case for state intervention.

Several key principles provide scope for designing or reforming PPIPs to remain within fiscal, market, social, and operational guardrails and contribute to resilience. These principles relate to:

- Strategic alignment and governance: Embed PPIPs in national risk-reduction strategies; define clear objectives and guardrails; ensure effective, multi-stakeholder governance; invest in risk data and modelling; and plan for adaptation.

- Financial mechanics and market discipline: Keep the state as reinsurer of last resort, covering only losses that private markets cannot bear; structure state guarantees to crowd in, not crowd out, private capacity; and use compulsion strategically, mainly where uptake needs to increase.

- Pricing and incentives: Use risk-based pricing as the default to signal risk and encourage mitigation; address affordability through targeted, transparent subsidies rather than broad price controls; and use product features and claims practices to reward risk reduction.

Emerging risks: cyber and pandemic-related business interruption

Applying this framework to two emerging risks – for which calls for PPIPs are growing – reveals important considerations:

- Cyber risk. While there is scope to strengthen cyber security (Pillar 1) and private cyber insurance (Pillar 2), covering peak cyber risk remains challenging. A state-backed PPIP (Pillar 3) could boost capacity, taking account of the ambiguity surrounding tail cyber risks and without overstepping fiscal and market guardrails.

- Pandemic-related business interruption risk. A PPIP could provide a state-backed liquidity facility for small and medium-sized enterprises (SMEs), with limits on the duration and amount of support. Insurers would serve as distributors and administrators, only bearing a small share of the risk. Such a PPIP cannot replace fiscal support and a broader economic resilience strategy.

Conclusion

PPIPs are often essential tools for maintaining insurability of disaster risks, with their design and operations as part of a proactive risk-management strategy. Governments must lead on risk reduction. PPIPs should be (re)designed to complement and incentivise risk reduction rather than subsidise exposure. Progress depends on aligning incentives around the common goal of proactively building a resilient society.

Foreword

In recent decades, societies have grown more prosperous, more interconnected, and, paradoxically, more vulnerable. Natural and man-made disasters now unfold against a backdrop of dense economic activity, stretched public finances, and rising expectations of protection. In this environment, insurance is a cornerstone of resilience, helping households, businesses, and governments absorb shocks and recover more quickly. Yet the frequency, scale, and sometimes systemic nature of today’s risks – and urgent need to address insurance availability and affordability challenges – are testing the limits of existing mechanisms and forcing a reassessment of how risk is reduced, shared, and ultimately borne.

This report examines widening protection gaps, and the role that public-private insurance programmes (PPIPs) can play in addressing them. Our comparative analysis of 14 programmes across countries and perils shows that many PPIPs have succeeded in restoring or increasing coverage where private markets alone could not. However, too frequently, they have functioned as passive shock absorbers rather than as part of a broader strategy to reduce risk. The analysis highlights the fiscal, market, social, and operational guardrails within which PPIPs must operate, and documents how pressures on these guardrails are mounting as risks grow and losses accumulate.

Maximising protection for society over time requires a shift from financing disasters to proactively managing risk. Governments must prioritise investment in risk reduction, strengthen private insurance markets, and deploy PPIPs strategically where private capacity is missing, rather than viewing them as substitutes for prevention. PPIPs, when well designed and aligned with national resilience strategies, can do more than share losses after disasters: they can reinforce incentives to reduce risk, protect public finances, and support faster, fairer recoveries. The recommendations set out here aim to support policymakers in making that transition, at a moment when the growing cost of inaction is becoming ever clearer.

Jad Ariss

Managing Director

Executive summary

The disaster protection gap – the uninsured share of economic losses from natural and man-made disasters – is widening. Global natural catastrophe (Nat Cat) losses reached USD 327 billion in 2024, with 57% uninsured. Between 1980–2024, Nat Cats caused an estimated USD 6.9 trillion in property losses, of which two thirds were uninsured. These uninsured losses act as a drag on economic recovery and push governments into slow, unpredictable, and budget-destabilising post-disaster relief.

Sharing losses is only part of the answer. Investing in risk reduction – measures that prevent or mitigate losses and support recovery and adaptation – is often more cost-effective than rebuilding. Insurance can complement these efforts by spreading remaining losses and providing rapid, pre-arranged liquidity that keeps firms open, preserves jobs, and reduces the need for ex-post fiscal support.

However, private-market mechanisms often do not, on their own, generate sufficient risk reduction or insurance coverage. Individuals underinvest in protection and insurance due to limited budgets, behavioural biases, and expectations of government aid. Insurers may be unable or unwilling to cover large, uncertain, and correlated risks at prices customers can afford. This creates a clear economic and fiscal rationale for government intervention to narrow the disaster protection gap to an efficient and socially acceptable level.

A three-pillar strategy

This report proposes a proactive, three-pillar strategy to narrow disaster protection gaps:

- Pillar 1: Invest in risk reduction. While only governments can lead infrastructure investment, they can also create incentives for individuals and businesses to reduce their own risks through, for example, land use planning and building codes, as well as by providing financial support and encouraging increased risk awareness.

- Pillar 2: Enhance private insurance markets. Governments can initiate targeted policy actions, such as awareness campaigns, insurance mandates, or supportive regulation to help private capacity and demand grow without distorting markets.

- Pillar 3: Develop public-private risk-sharing mechanisms. In some regions and for some perils, collaboration between the re/insurance industry and the public sector – often implemented as a public-private insurance programme (PPIP) – can lead to more efficient risk-sharing.

PPIPs: Successes and challenges

PPIPs are already a prominent feature of the global insurance landscape. This report analyses fourteen existing PPIPs across natural and man-made perils. Many have delivered on their core mission. France’s Caisse Centrale de Réassurance (CCR), Spain’s Consorcio de Compensación de Seguros (CCS), and New Zealand’s Natural Hazards Commission (NHC) achieve near-universal coverage for key perils. Pool Re (UK) and the Terrorism Risk Insurance Program (TRIP, US) restored capacity after major terrorist attacks when private markets withdrew.

Yet, PPIPs involve significant design challenges. This report’s analysis revolves around the four guardrails that a PPIP must navigate, reflecting fiscal, market, social, and operational constraints:

- Fiscal guardrail: Limit long-term burdens on public finances and avoid open-ended state guarantees.

- Market guardrail: Avoid crowding out private capacity, competition, and innovation.

- Social guardrail: Ensure affordability and an acceptable distribution of costs and benefits, especially for vulnerable groups.

- Operational guardrail: Pay claims quickly and adapt to risk and market changes.

Our analysis shows that many current PPIPs have stretched one or more of these guardrails. Several have experienced severe financial strain, including the US National Flood Insurance Program’s (NFIP) enormous debt burden; capital losses at France’s CCR after recent droughts; and New Zealand’s NHC drawing heavily on private capital and Treasury support after major earthquakes. Market distortions arise when state-backed reinsurance crowds out private capacity, as in France, where CCR covers most catastrophe reinsurance; or when solidarity pricing dulls risk signals and sustains development in high-risk areas, as in the cases of Flood Re (UK) and the NFIP in the US. Broad risk pools can favour higher-income households in exposed areas, exacerbating economic inequalities, while attempts to reintroduce risk-based pricing in the NFIP have triggered political backlash. Operationally, some schemes pay quickly, but others face disputes over claims, processing delays, and some exhibit high loss ratios, as seen in Australia’s recent Cyclone Reinsurance Pool.

From sharing risks to supporting risk reduction

In many countries, Pillar 3 interventions have preceded strong Pillar 1 initiatives, making coverage available and affordable before, and often instead of, effective risk reduction strategies. This approach is reaching its limits: while PPIPs can slow the widening of protection gaps, they cannot narrow them if risk itself continues to increase.

This report calls for policymakers to treat PPIPs as part of a broader resilience strategy, not as standalone financial tools. PPIPs must not only share disaster losses but also support – or at least not undermine – public and private initiatives to reduce risk. Their legitimacy will increasingly depend on how their Pillar 3 functions reinforce Pillar 1 objectives.

Decision-process and design principles

Because PPIPs are costly and complex, the report proposes a four-step process to assess the need for and potential role of a PPIP:

- Substantiate the protection gap and the underlying drivers on the risk, supply, and demand sides.

- Prioritise risk-reduction measures (Pillar 1) and strengthen private insurance markets (Pillar 2) through targeted, market-enhancing measures. This minimises the residual risk a PPIP needs to absorb.

- Agree on the perils and exposures a PPIP should cover, ensuring that remaining protection gaps are societally acceptable.

- Make a clear fiscal case for state intervention.

Based on the comparative analysis, the report outlines key principles for designing or reforming PPIPs to remain within fiscal, market, social, and operational guardrails and contribute to resilience. These principles relate to:

- Strategic alignment and governance: embed PPIPs in national risk-reduction strategies; define clear objectives and guardrails; ensure effective, multi-stakeholder governance; invest in risk data and modelling; and plan for regular adaptation.

- Financial mechanics and market discipline: keep the state as reinsurer of last resort, covering only loss layers that private markets cannot bear; structure layers, triggers, and capital to crowd in, not crowd out, private capacity; and use compulsion strategically, mainly where high coverage is essential.

- Pricing and incentives: use risk-based pricing as the default to signal risk and encourage mitigation; address affordability through targeted, transparent subsidies rather than broad price controls; and leverage product features and claims practices to reward risk reduction.

Emerging risks: Cyber and pandemic-related business interruption

Applying this framework to two emerging risks in which new PPIPs are being actively considered suggests some important lessons:

- Cyber risk. There is significant scope to strengthen cybersecurity and incident response (Pillar 1) and to enable private cyber insurance market growth (Pillar 2). However, the scale and/or uncertainty of accumulated losses from a systemic cyber event mean that there is a lack of private capacity to absorb extreme tail risk. In this case, a state-backed PPIP (Pillar 3) could prove beneficial. In practice, however, designing such a scheme faces serious challenges, largely due to the ambiguity surrounding peak cyber risks and concerns about overstepping both the fiscal and market guardrails.

- Pandemic-related business interruption risk. Such risks remain uninsurable in a traditional sense. At best, a pandemic PPIP could provide a narrow, state-backed liquidity facility, particularly for small and medium-sized enterprises (SMEs), with limits on how long the support lasts and how much is provided. Insurers would serve as distributors and administrators, only bearing a small share of the risk. Such a PPIP cannot replace fiscal support and a broader economic resilience strategy.

Conclusion

PPIPs are often essential tools for maintaining insurability of disaster risks. To ensure viability in a world of rising, increasingly systemic risks, their design and operations need to be part of a proactive risk management strategy that prioritises risk reduction, preserves market discipline, protects public finances, and maintains social legitimacy.

Introduction

Economic losses from disasters are increasing, leaving a large and widening protection gap that represents the uninsured share of economic losses. This section shows how protection gaps and the costs of post-disaster relief strain public finances and slow economic recovery. It argues for a proactive strategy that prioritises risk reduction and implements efficient risk-sharing mechanisms for residual losses. The rest of the report focuses on public-private insurance programmes (PPIPs) as a key, but complex, component of this strategy.

A widening disaster protection gap

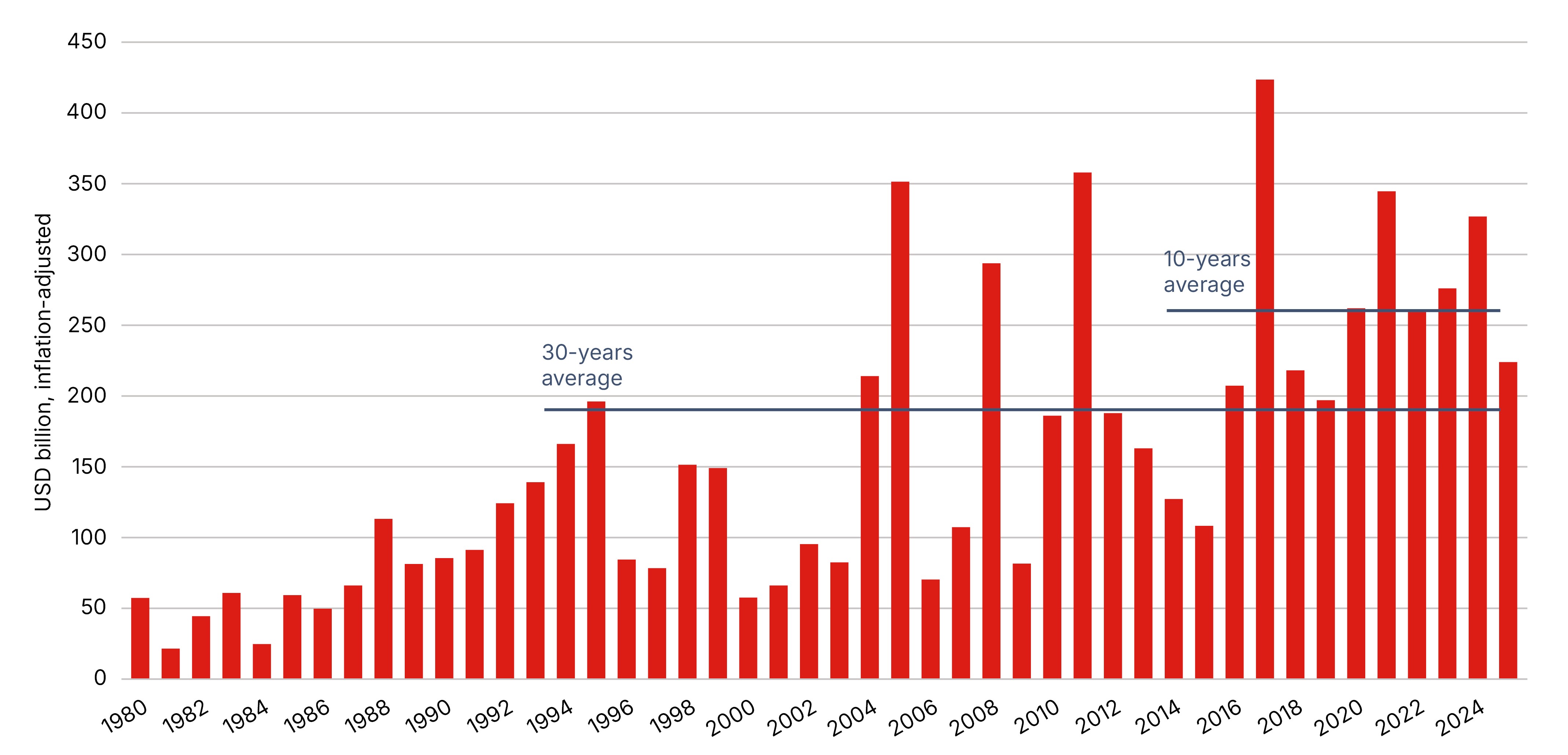

The United Nations defines disaster as “serious disruption of the functioning of a community or a society causing widespread human, material, economic or environmental losses which exceed the ability of the affected community or society to cope using its own resources.” Economic losses from disasters have increased over recent decades (see Figure 1), mainly attributable to rising natural catastrophe (Nat Cat) losses. Nat Cat losses totalled USD 277 in 2023, USD 327 billion in 2024, and around USD 224 billion in 2025, with a 10-year average of USD 262 billion and a 30-year average of USD 190 billion (inflation-adjusted).1

FIGURE 1: TOTAL ECONOMIC LOSSES FROM NATURAL DISASTERS (EXCLUDING DROUGHT AND HEATWAVE) IN USD AS OF 2025, INFLATION-ADJUSTED TO 2025, BETWEEN 1980 AND 2024

Source: Munich Re, NatCatSERVICE, May 20252, and Munich Re3

Record-breaking events are the new norm. Natural disasters, terrorist attacks, or pandemics can hit economies as hard as wars or financial crises.4 Although difficult to measure, the disaster protection gaps are significant. For example, Nat Cats caused an estimated USD 6.9 trillion in property losses from 1980 to 2024 (inflation-adjusted), 67% of which were uninsured.5 Disaster protection gaps will likely continue to widen across all perils, including cyber, through 2030.6

The consequences of disasters reach well beyond direct asset damage.7 The IMF estimates that, on average, disasters cut annual gross domestic product (GDP) by 1.3% in affected countries.8,9 These losses reflect not only destroyed assets but also indirect impacts, such as supply-chain disruption.10 Although reconstruction may briefly lift GDP, national or regional economies with low financial buffers often suffer lasting losses.11,12 They struggle to absorb immediate income shocks and to rebuild quickly, often due to credit and fiscal constraints, institutional weaknesses, or production linkages that transmit shocks across sectors.

Why governments intervene to narrow disaster protection gaps

When disaster losses are uninsured or underinsured, governments often step in to provide relief to households and firms. Such aid, however, is typically slow, insufficient, and unpredictable.13 It can also destabilise public finances if it strains budgets and debt service obligations.

Ex-ante risk-sharing mechanisms, such as insurance, can offer a more efficient alternative by spreading potential losses across many actors so that no single participant bears the full cost of an event. By providing rapid, pre-committed liquidity to disaster victims, insurance eases cash flow and borrowing constraints. This allows businesses to stay open, preserving employment, enabling output to rebound sooner, and reducing the need for taxpayer-funded aid.14 As a result, research suggests insured disasters are more likely to have temporary rather than permanent macroeconomic effects, a hallmark of resilience.15,16

However, sharing losses is only part of the solution. Investing in risk reduction measures (through actions that prevent or mitigate losses and foster recovery and adaptation) can save up to USD 4–15 in future losses for every dollar spent.17 A proactive strategy that combines risk reduction measures with the risk-sharing mechanisms of insurance can provide significant macroeconomic benefits.

While individuals and businesses would undoubtedly prefer to avoid or minimise losses, private markets alone, such as property or insurance markets, may be unable to both reduce risks sufficiently or share risks at scale. This creates the economic and fiscal case for government intervention to narrow the disaster protection gap to an economically efficient and societally desirable level.18

A growing interest in public-private insurance programmes (PPIPs)

PPIPs share risks and costs across public and private stakeholders – households, firms, re/insurers, governments, and potentially capital markets – to make insurance more available, more affordable, and to boost uptake in a way that neither public nor private sector could on its own. Such partnerships are not new; many countries have long-standing schemes, such as New Zealand’s 80-year-old earthquake programme. Historically, these schemes were founded reactively, often in the aftermath of a major disaster. However, persistent protection gaps are now prompting many jurisdictions to explore PPIPs proactively, rather than waiting for a crisis to force action:

- Since 2022, Australia’s Cyclone Reinsurance Pool has addressed chronic affordability and availability issues for cyclone protection. In Italy, where fewer than 6% of businesses were insured against natural disasters, a 2025 bilateral mandate requires businesses to purchase coverage and insurers to offer it, with a state-backed 50% reinsurance quota.19

- Debates are ongoing in other jurisdictions around creating PPIPs addressing specific risks: cyber and pandemic risks in the US.; flood coverage in Canada and Germany; and natural disasters in India and at the EU level.20

Structure of the report

A shift to proactive risk management requires more than financial or technical tools; it requires a social contract in which societies explicitly decide who invests in risk reduction and how losses are shared among households, businesses, re/insurers, and the state.21,22 This report explores the role PPIPs play in such a social contract. Insurability becomes a political choice, not just a technical issue, shaped by public investment in resilience, market-enhancing policies, and public-private risk-sharing mechanisms.23

Establishing PPIPs involves complex trade-offs with significant implications for public finances, markets, and social equity. This report, therefore, seeks to understand when such partnerships are viewed as necessary and how they operate.

- Section 2 details the root causes of persistent protection gaps; introduces how a proactive strategy can address these causes; and suggests how PPIPs can serve as one of three core pillars in forming this strategy.

- Next, we analyse the mechanics of this intervention. Section 3 presents the conceptual framework for navigating a PPIP’s complex policy trade-offs; and Section 4 lays out the core design components of the PPIP.

- Section 5 tests the aims and designs of PPIPs against their performance identifying common strengths and weaknesses of fourteen existing PPIPs.

- Section 6 diagnoses a growing challenge common to many PPIPs: rising losses threaten the viability of established risk-sharing models. Many PPIPs will need to align with and support risk reduction measures – a challenging role some already seek to fulfil within their capacity to do so.

- Finally, Section 7 synthesises these findings into concrete recommendations for designing sustainable PPIPs that are fit for an era of growing and emerging risks.

Narrowing disaster protection gaps: A proactive strategy

Section 1 shows why disaster protection gaps may require state intervention. An effective strategy must address the root causes of these gaps. Understanding these causes is therefore crucial for developing adequate policy responses to reduce risk and increase risk coverage. This section describes the underlying causes of disaster protection gaps and outlines a three-pillar proactive approach to tackle them.

Root causes of disaster protection gaps

Persistent protection gaps reflect structural frictions in both insurance markets and public policy. This report identifies three root causes (see Figure 2):

A. On the economic-loss side, risk reduction strategies may not keep pace with rising hazards, exposures, and vulnerabilities.

B. On the insurance-supply side, the potential for significant losses and their uncertainty – defined as the difficulty of quantifying the likelihood and severity of losses – may lead to coverage being either unavailable or available but unaffordable.

C. On the insurance-demand side, households and businesses may fail to purchase sufficient insurance due to unaffordability, insufficient risk awareness, or expectations of government relief.

FIGURE 2: CAUSES OF PROTECTION GAPS

Source: Geneva Association

2.1.1 Growing risks and insufficient risk reduction

Risk is rising as its three components increase: hazard (event frequency/severity), exposure (people/assets in danger), and vulnerability (ease of damage).24 New hazards are emerging (e.g. cyberattacks and chemical, biological, radiological, and nuclear – or CBRN – terrorism), while existing risks, such as climate extremes, are intensifying.25 Exposures are growing as urbanisation concentrates assets in potentially high-risk areas, economies increasingly depend on intangible assets such as supply chains, and digitalisation expands cyberattack surfaces. Vulnerability is also increasing in some areas due to weak land-use planning, building codes, and cybersecurity. As a result, many households and firms face new and worsening risks, including weather-related events, cyberattacks, and pandemics. Many of these risks have systemic potential: a single disruption in energy, transport, or digital infrastructure can cascade across sectors and regions through disrupted supply chains, amplifying losses. At the same time, uncertainty is growing due to limited historical data about new or changing risks. Consequently, some risks grow or evolve faster than societies can respond to them.26

Risk reduction occurs at the individual level (e.g. home retrofits) to protect single properties and at the community level (e.g. flood barriers or land-use rules) to protect entire areas. Even though risks are rising, both forms of risk reduction remain underfunded:

- Individual investments often fall short as individuals underestimate risk, face budget constraints, or expect government help after disasters.

- Large-scale projects require public funding. However, authorities may face fiscal constraints or lack long term policy goals, failing to sufficiently anticipate future returns on investment relative to current costs.27 Investment may also require blended finance structures, which combine public and private funding. These instruments are often difficult to access because they involve complex risk-sharing arrangements, large minimum investment sizes, and long lock-in periods that exclude most investors.

In addition, individuals and public entities alike often lack robust risk-reduction cost-benefit data, hindering the effective prioritisation and financing of interventions.28

2.1.2 Costly or unavailable re/insurance coverage

Business lines, such as motor insurance, rely on diversification: pooling many independent risks reduces the volatility of the average claim, as the law of large numbers predicts. Pooling thus lowers required capital per policy, bringing diversification benefits. This actuarial logic breaks down for disasters, as dependencies lead to simultaneous losses across individual and business lines, undermining diversification. Average claims’ volatility subsequently remains high or might increase with pooling, leading to a surge in re/insurers’ capital needs, thus inflating premiums.29 On top of this, uncertainty increases the capital costs re/insurers must pay to compensate investors for absorbing unpredictable future losses.

Simultaneous losses and heightened uncertainty have two consequences:

- Costly insurance coverage: As catastrophic losses or high uncertainty increase premiums, additional pressures outside re/insurers’ control, such as insurance taxes, inflation, or litigation costs in disputed claims, compound the issue.30 Low insurance uptake means smaller pools, less diversification benefits, and fixed costs spread over fewer customers, keeping premiums high.

- Unavailable insurance coverage: When risks become too concentrated or uncertain, insurers may limit the amount of coverage they offer, impose stricter terms, increase exclusions, or withdraw from some high-risk regions or perils altogether, redeploying their capital to cover other risks. Capital also disappears when the price needed to make a profit is higher than what customers will pay or what regulators will allow.31

Reinsurers provide additional capacity by spreading exposures globally, absorbing insurers’ tail risk. Capital markets, through insurance-linked securities (ILS), can further increase available capital by tapping into diversified investor portfolios. However, even these mechanisms hit structural limits to diversification.32

2.1.3 Low disaster insurance uptake

Even when disaster insurance is available, uptake may be low. The reasons are frequently similar to the ones that lead to under-investment in risk reduction. These factors include:

- Cognitive biases: Individuals frequently exhibit optimism bias, leading them to underestimate the likelihood of rare events such as disasters; only react to recent events; or see insurance as a poor investment due to its uncertain payoff.33

- Institutional factors: The expectation that governments will step in, or will be obliged, to provide post-disaster relief may suppress demand for insurance.

- Affordability: Low-income households or small businesses in high-risk areas may struggle to afford coverage.34,35

- Other factors: Culture, risk awareness and literacy, personal experience, and emotions all affect risk perception and demand. Abstract contract wording, exclusions, benefits that do not match actual losses (basis risk), and complex or confusing purchase processes also deter buyers.36

A 3-step proactive risk-management strategy

A proactive risk-management strategy must address the causes of the protection gap. This strategy rests on three pillars: one based on risk reduction, and the other two on risk sharing (see Figure 3).37

- Pillar 1: Investing in risk reduction. This addresses the first root cause of the protection gap: the risk itself. It is both a responsibility of private individuals (potentially incentivised by legislation or fiscal policy) and public authorities.

- Pillar 2: Enhancing private insurance markets. On the demand side, light-touch policy initiatives can include risk awareness campaigns, financial incentives to purchase insurance, or insurance mandates. On the supply side, examples include regulatory frameworks that support capacity-building, such as removing constraints on risk-based pricing or measures to encourage risk transfer to capital markets. These tools help private capacity and support demand without distorting insurance markets.

- Pillar 3: Establishing public-private risk-sharing mechanisms. In some regions and for some perils, the demand- or supply-side causes of the disaster protection gap may be better addressed jointly by the re/insurance industry and the public sector. This pillar, often a PPIP, fundamentally interferes with market operations by introducing tools such as state guarantees or by regulating underwriting and pricing. Therefore, it is an instrument that requires careful design.

Figure 3: A proactive three-pillar strategy for governments to reduce and share risks

Source: Geneva Association, adapted from Zurich Insurance Group

These three pillars, ordered from least to most market-distorting, represent an ideal order of priority. Risk reduction (Pillar 1) takes precedence whenever it is the most cost-effective option. Ideally, societies would invest in prevention and adaptation until the additional costs of further risk reduction outweigh the benefits. Only then should any remaining residual risk be transferred via private markets and, potentially, PPIPs.

This framework relies on a clear understanding of shared responsibilities, with the government orchestrating a national risk-management strategy:

- Pillar 1 indicates that while households and businesses are responsible for their private risk reduction, such as retrofitting a property, some risk components, such as the likelihood of a flood, are beyond their control. Then, the government’s role in Pillar 1 is twofold: funding and building risk-reduction infrastructure (such as flood defences); and using its legislative authority to set rules (such as land-use regulation or building codes) that incentivise or mandate private action.

- Pillar 2 is fundamentally a government and regulatory function; only the government can legislate insurance mandates, create tax incentives, or adapt regulatory frameworks.

- Pillar 3 is also a state responsibility. While it involves a public-private partnership that the re/insurance industry may initiate, only the government can legislate state guarantees or override market practices such as risk-based pricing to address availability and affordability issues.

Conceptual framework for PPIP analysis

Section 2 introduces the rationale for PPIPs (Pillar 3) as state interventions that alter market operations to improve risk-sharing. Economic theory and practice show that attempts to correct a particular market distortion can introduce new distortions, potentially reducing rather than improving overall market efficiency.38 Moreover, PPIPs have significant impacts beyond re/insurance markets: they typically expose the state to fiscal risk and may involve redistributive mechanisms with implications for social equity. The successful design of a PPIP therefore requires a conceptual framework that captures these implications.

Designing a PPIP is a complex policy optimisation problem that seeks to maximise societal well-being and market efficiency. This problem has three core components (see Figure 4):

- Desired coverage outcomes: Maximise coverage availability, affordability, and uptake.39

- Policy tools: To achieve desired coverage outcomes, policymakers use two main tools:40

- State guarantees: Formal commitments by the state to absorb losses for which private capacity is unavailable or prohibitively expensive.

- Cost redistribution: Mechanisms to spread losses and costs across a large pool of policyholders.

- State guarantees: Formal commitments by the state to absorb losses for which private capacity is unavailable or prohibitively expensive.

- Guardrails: PPIPs are constrained by four practical, potentially competing, imperatives:

- Fiscal: Preserving fiscal space to cope with future shocks to governments’ balance sheets.

- Market: Not crowding out private markets; ensuring re/insurers carry a sustainable level of risk; fostering market discipline, such as through risk-based prices; and promoting innovation.

- Social: Ensuring vulnerable groups can access coverage at a price they can afford and that benefits are distributed in a way that is considered fair.

- Operational: Delivering predictable, fast claims-paying ability and being adaptable to a changing risk landscape, all while remaining relevant to individual claimants and wider societies.41

- Fiscal: Preserving fiscal space to cope with future shocks to governments’ balance sheets.

Figure 4: Designing a PPIP is an optimisation problem

Source: Geneva Association

Policymakers face a challenge: deploying each policy tool to achieve coverage outcomes may collide with or even overstep guardrails. This requires policymakers to evaluate trade-offs:

- State guarantees improve availability and affordability. State backing is cheaper than private capital, lowering prices. When governments absorb tail risk, the remaining risk becomes insurable. Insurers thus face lower capital needs, freeing up capital to underwrite more policies (see Box 1). Ultimately, a well-designed state guarantee can stimulate private market growth. Conversely, one that absorbs otherwise privately insurable risks will stifle competition, testing the market guardrail. Moreover, as explicit contingent liabilities, state guarantees test the fiscal guardrail by reducing budgetary space, even if never used.

- Cost redistribution uses two mechanisms. First, compulsion (mandates to purchase or sell coverage), which increases uptake, creating a larger, more stable pool. It spreads fixed costs and prevents adverse selection (where only high-risk parties buy insurance), thus keeping coverage more affordable. Solidarity pricing, which lowers premiums for high-risk policies, can further boost affordability for those most at risk.42 Secondly, cost-redistribution, which requires choices in a trade-off between market efficiency and social equity.43 For example, using solidarity pricing for affordability purposes supports the social guardrail but impacts against the market guardrail by blunting risk signals and undermining competition.

Each PPIP must secure its social license – broad societal acceptance – by delivering expected outcomes and navigating guardrails in line with societal norms. How PPIPs seek to achieve their objectives while remaining within their guardrails reflects societal expectations and preferences, which explains why schemes differ across countries and perils.

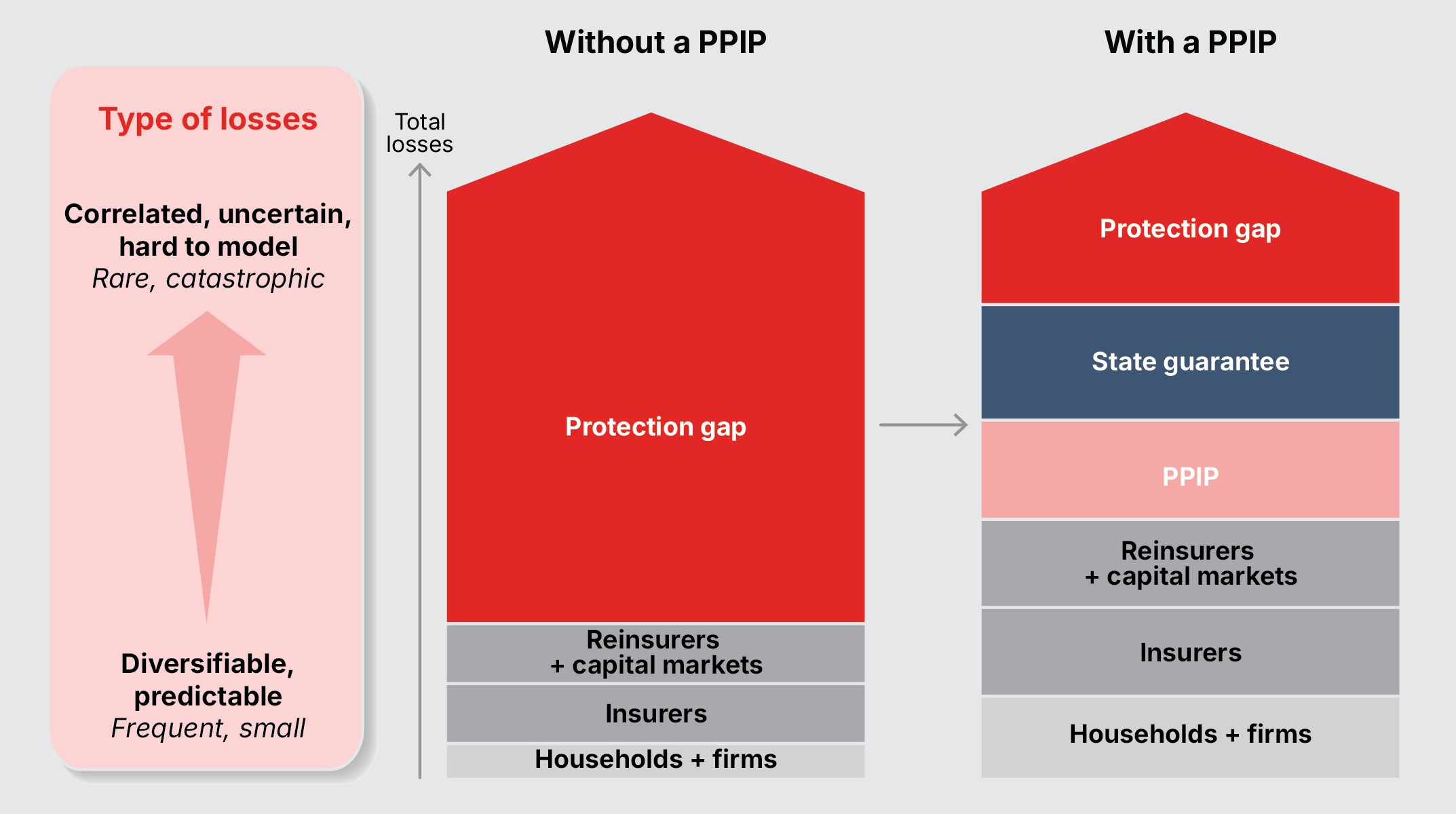

Box 1: How state guarantees make disasters more insurable

Efficient risk-sharing relies on loss layering, allocating risk based on frequency and severity (see Figure 5, left):44

- The smallest, most frequent losses stay with policyholders through deductibles.

- Routine losses (diversifiable, predictable), which entail a low cost of capital, stay with policyholders (deductibles) and primary insurers (up to their retentions). Insurers handle frequent claims at a low operational cost, given their comparative advantage in underwriting and risk management.

- For rare and large losses (correlated, uncertain, hard to model), the cost of capital rises steeply. This makes them best suited for reinsurers or capital markets. These can better diversify risks globally and across business lines, lowering capital needs. Moreover, low claims frequency offsets higher operational costs associated with greater distance from the underlying policyholders.

- For the most catastrophic, correlated, and uncertain events, capacity may be unavailable or unaffordable.

A state-backed PPIP introduces a new financing structure in which the state acts as reinsurer of last resort (see Figure 5, right):

- State guarantees cover the catastrophic loss layers.

- The PPIP’s own funds sit below. Built from retained earnings (accumulated premiums) in low-loss years – thus leveraging time diversification – and, being backed by the state, held at a lower cost than private capital, these funds further improve affordability.45

- Private re/insurers cover the lower layers of risk. Not bearing extreme losses reduces capital burdens, enabling insurers to offer more coverage at prices customers can afford, boosting availability and uptake.46

Therefore, state guarantees make disasters more insurable by catalysing capital accumulation.47 As private and PPIP capacity grow, the state guarantee can move up to cover increasingly less frequent losses, lowering fiscal risk.

FIGURE 5: How state guarantees make risks more insurable by catalysing capital accumulation

Source: Geneva Association

Anatomy of a PPIP: Core components

Drawing on findings from the analysis of fourteen PPIPs across five peril classes (see Table 1), this section explores the specific design choices used to implement state guarantees and cost redistribution while respecting agreed guardrails. Readers interested in the specific features of individual schemes can refer to the detailed table in the appendix.48

TABLE 1: THE PPIPs ANALYSED IN THIS REPORT

Name | Peril 49 | Country |

| Australian Reinsurance Pool Corporation, Terrorism Pool (ARPC)-Terrorism | Terrorism | Australia |

| Gestion de l’Assurance et de la Réassurance des Risques Attentats et Actes de Terrorisme (GAREAT) | France | |

| Extremus | Germany | |

| Pool Re | UK | |

| Terrorism Risk Insurance Program (TRIP) | US | |

| Japan Earthquake Reinsurance Company (JER) | Earthquakes | Japan |

| Natural Hazards Commission – Toka Tū Ake (NHC) | New Zealand | |

| Turkish Catastrophe Insurance Pool (TCIP) | Türkyie | |

| California Earthquake Authority (CEA) | US | |

| Caisse Centrale de Réassurance (CCR) | Nat Cats | France |

| Consorcio de Compensación de Seguros (CCS) | Spain | |

| Flood Re | Floods | UK |

| National Flood Insurance Program (NFIP) | US | |

| Australian Reinsurance Pool Corporation, Terrorism Pool (ARPC)-Cyclone | Cyclones | Australia |

Source: Geneva Association

The sample covers a range of natural and man-made hazards, mostly in developed countries. While they serve comparable policy objectives, these PPIPs differ widely in how they navigate trade-offs between fiscal, market, social, and operational guardrails. This shows that there is no unique blueprint: each design reflects the conditions – societal, economic, political, or regional – under which the PPIP formed. Moreover, some PPIPs in our sample have operated for decades (e.g. France’s CCR) and others for a few years (e.g. Australia’s ARPC-Cyclone), shedding light on long-term challenges and illustrating recent trends.

Implementing the state guarantee

The sample covers a range of natural and man-made hazards, mostly in developed countries. While they serve comparable policy objectives, these PPIPs differ widely in how they navigate trade-offs between fiscal, market, social, and operational guardrails. This shows that there is no unique blueprint: each design reflects the conditions – societal, economic, political, or regional – under which the PPIP formed. Moreover, some PPIPs in our sample have operated for decades (e.g. France’s CCR) and others for a few years (e.g. Australia’s ARPC-Cyclone), shedding light on long-term challenges and illustrating recent trends.

A. Scope of coverage: What does the guarantee cover?

A PPIP’s scope defines the specific protection gap that the state guarantee addresses.

Key choices:

- Eligible perils: Schemes can be peril-specific or multi-peril. Event definition can be narrow (conventional terrorism only for Germany’s Extremus) or broad (including CBRN risks such as in the UK or France). Payouts may also depend on official state recognition of the event (e.g. France’s CCR and most terror PPIPs).

- Eligible exposures: Terror PPIPs typically insure commercial properties, sometimes focusing on large businesses (e.g. Germany’s Extremus, France’s GAREAT). 50 Natural disaster schemes usually focus on residential properties, though some include SMEs (e.g. NFIP in the US, ARPC-Cyclone in Australia). Some schemes also cover damage-related business interruption (e.g. France’s CCR and the UK’s Pool Re).

- Coverage limits: Several insurer-PPIPs cover losses only up to a cap (e.g. NHC in New Zealand, TCIP in Türkyie, or NFIP in the US). Reinsurer-PPIPs typically align with property insurance terms, potentially covering all insured losses (e.g. France’s CCR) or a regulated, capped loss (e.g. Japan’s JER).

Trade-offs:

A narrow scope keeps premiums affordable and limits the chance of hitting fiscal constraints. In fact, a well-calibrated cap can absorb most losses, stabilising livelihoods after a disaster. 51 Moreover, it can stimulate private markets into providing top-up coverage, aligning with the market guardrail. Conversely, a broad scope better reduces protection gaps and brings diversification benefits and economies of scale.52 However, this may expose the state to larger losses and crowd out private capacity, testing the fiscal and market guardrails.

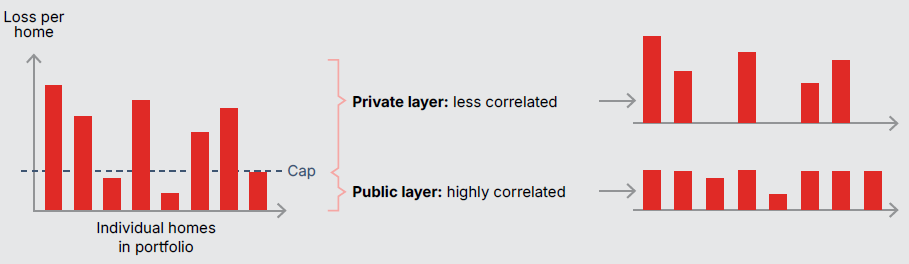

Box 2: How New Zealand’s NHC balances public and private shares of risk

Designing PPIPs is a balancing act: the state should absorb some risk, but not too much. New Zealand’s NHC provides a real-world example of this optimisation.

The NHC state-backed cover acts as a public deductible (currently NZD 300,000 per property). This cap is designed to solve an insurability problem for private markets, as illustrated in Figure 6. Losses below the cap represent the small-to-medium first loss damages from an earthquake. The key issue for insurers is that these losses can occur simultaneously across all exposed properties. As discussed in Section 2.1.3, highly correlated losses cannot be diversified away, driving up capital costs. Losses above the cap, however, correspond to rarer types of damage. These top-up losses are also more independent from home to home.

By absorbing correlated first losses, the NHC leaves private insurers not only with lower expected losses to cover, but also with a risk that is more diversifiable and thus more insurable.53 This enables the private market to offer top-up policies at risk-based yet affordable prices. NHC regularly adjusts the cap as construction costs climb, aiming to “keep private top-up cover affordable and attractive.”54 Each cap increase further challenges the fiscal guardrail but supports affordability and private coverage uptake, illustrating the trade-offs PPIPs face.

FIGURE 6 HOW THE NHC’S CAP ABSORBS THE MOST CORRELATED PART OF DISASTER LOSSES

Source: Geneva Association

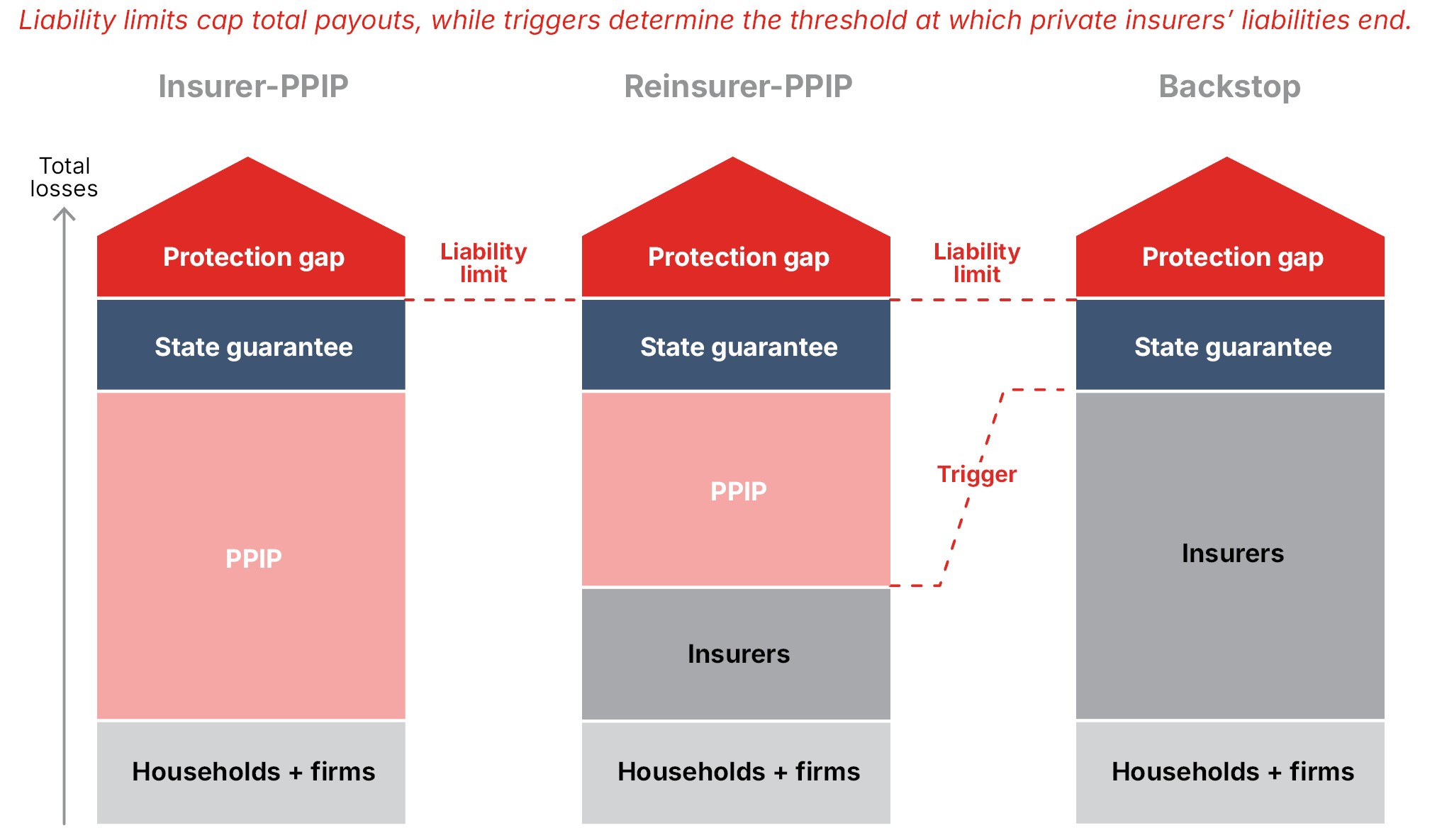

B. Market role: Insurer, reinsurer, or backstop?

The most visible aspect of state guarantees is how they interface with the insurance market (see Figure 7).

Key choices:

- Insurer-PPIPs provide direct insurance to policyholders.55 An insurer-PPIP pays claims directly from its own reserves and capital (PPIP layer in Figure 7). If those funds are exhausted, the state guarantee covers the excess (state guarantee layer in Figure 7). This model affords the government greater control over policy terms and pricing.56

- Reinsurer-PPIPs provide reinsurance to private insurers. This lowers insurers’ capital costs and preserves market discipline at the direct insurance level. Private insurers retain initial losses (insurers layer in Figure 7), underwrite and manage claims, and cede higher loss layers to the PPIP. The PPIP’s reserves and capital are used first, then the state guarantee.

- Backstops consist only of a state guarantee triggered above significant private sector retention, with minimal operational structure (e.g. TRIP in the US). A backstop does not collect premiums and therefore does not accumulate capital.

Trade-offs:

Insurer-PPIPs arise when insurance penetration is very low, or coverage is unavailable, as the government assumes direct financial risk – essentially replacing the private market for eligible perils and exposures. Reinsurer-PPIPs or backstops typically arise when private capital is unavailable for disaster-level losses (e.g. Pool Re in the UK or TRIP in the US) or when regulation mandates that insurers offer disaster coverage (e.g. Japan’s JER, France’s CCR). Insurer-PPIPs are more likely to strain fiscal guardrails, as they assume all eligible losses. Conversely, reinsurer-PPIPs help maintain market discipline at the direct insurance level.

C. Payout structure: Triggers and liability limits

The mechanics of the state guarantee clarify how much capital is available when disaster strikes and what share the private sector provides.

Key choices:

- Liability limits: They define the maximum payout, including public and private payouts, per event or annually.

- Triggers: For reinsurer-PPIPs and backstops, triggers are the loss threshold at which private insurers’ liability ends, and a reinsurer-PPIP or a backstop starts paying claims.57

Figure 7 illustrates how liability limits cap total payouts, while triggers mark the transition from private insurer liabilities (including those ceded to private reinsurers) to reinsurer-PPIP or backstop liabilities. For reinsurer-PPIPs, the trigger corresponds to the sum of insurers’ retentions. In TRIP (US), a backstop, the trigger defines the losses insurers must bear before fiscal support kicks in.58

Trade-offs:

If the trigger is set too low, the reinsurer-PPIP or backstop crowds out private insurers by covering insurable losses, straining the market guardrail; if set too high, a protection gap remains. Calibrating liability limits and triggers, thus, ideally relies on robust risk data and modelling. However, where uncertainty is high, calibration focuses on determining the maximum level of risk the private market’s capital base can sustainably retain, ensuring the state acts strictly as a reinsurer of last resort.

The state’s fiscal commitment varies, reflecting different approaches to managing the fiscal guardrail. In Japan, the state guarantee accounts for 97.2% of JER’s JPY 12 trillion liability limit, while in the US, the state bears around 33% of TRIP’s USD 100 billion liability limit. Some schemes benefit from unlimited state guarantees and, therefore, have no liability limits. They cover all eligible losses above the trigger, further narrowing protection gaps but creating open-ended fiscal liabilities that push the fiscal guardrail.

FIGURE 7: LOSS ALLOCATION ACROSS THREE TIERS: 1) INSURERS, 2) PPIP (OWN CAPACITY), AND 3) STATE GUARANTEE Liability limits cap

Source: Geneva Association

Finally, two PPIPs rely on industry levies instead of state guarantees. These are mandatory post-event contributions collected from insurers or policyholders. This removes fiscal exposure, shifting the cost of disasters onto insurers and policyholders. For example, should available funds run out, Flood Re can impose an unlimited Levy 2 on all UK home insurers. Similarly, California’s CEA can levy USD 1 billion from policyholders and USD 1.6 billion from participating insurers. While protecting public finances, post-disaster levies can lead to premium increases or delays in claims payments, potentially straining social and operational guardrails.

D. Capital strategy: Buffering the state guarantee

Capital strategies determine how PPIPs manage the risk on their own balance sheet (in Figure 7, PPIP layers).

Key choices:

- Own capital: Most PPIPs build capital through retained earnings: in years with few or no major disasters, premium income accumulates to absorb future losses.59 This capital serves as a first buffer before the state guarantee is called.60

- Private capital: Many PPIPs also purchase reinsurance and issue ILS – particularly those with smaller or no state guarantees.

Trade-offs:

Own capital accumulation works best for low-frequency perils such as earthquakes or terrorism, with long return periods. In the face of such perils, capital accumulation is essential for managing the fiscal guardrail, creating a buffer – as in the UK’s Pool Re, with GBP 7 billion in accumulated funds – that ensures the state guarantee is triggered only rarely. A capital mix that includes reinsurance and ILS, however, helps maintain the market guardrail by shifting more risk to private markets and connecting PPIPs to private pricing and risk signals. This also provides PPIPs with renewable capital and leverages global diversification, but exposes them to pricing volatility, potentially straining the operational guardrail.

E. The cost of the state guarantee

Unlike post-disaster aid, which often is a non-repayable transfer, governments can charge for state guarantees.

Key choices:

- Upfront fees: The PPIP compensates the government for its state guarantee, as in the UK’s Pool Re.61

- Post-event repayments: Governments recoup some or all fiscal outlay in the years following a disaster (e.g. New Zealand’s NHC or TRIP and NFIP in the US).

Trade-offs:

Upfront fees, which act as a premium to compensate the state for its risk-bearing capacity, monetise the state’s commitment. For example, Pool Re (UK) has transferred over GBP 2 billion to the Treasury since its inception, in return for a state guarantee that has never been triggered. Upfront fees help maintain financial discipline in a PPIP by reflecting the cost of fiscal risk. They also provide predictability. This also raises the technical challenge of setting a price for risks that are difficult to quantify. Post-event recoupment, on the other hand, avoids immediate costs for the PPIP but may further strain its finances after major disasters and lead to premium increases, potentially straining the social and operational guardrails.

Implementing cost redistribution

While state guarantees lower premiums, some PPIPs rely on cost redistribution to further boost coverage affordability and uptake.

A. Compulsion

To overcome low uptake, selling or purchasing insurance coverage may be required by law or regulation.

Key choices:

- Supply-side mandates (insurers must offer coverage) mean insurers must include a disaster add-on to specific policies, but policyholders can opt out.

- Demand-side mandates (policyholders must buy coverage) are rare, usually targeting specific segments. For example, French tenants must have household insurance (which includes natural catastrophe cover). Türkyie mandates TCIP cover for all eligible properties.

- Compulsory bundling mandates both supply and demand. Insurers who sell basic policies must also offer the disaster component, and policyholders who buy basic policies cannot opt out. For example, in France and Spain, Nat Cats and terrorism coverage are bundled with property coverage.

Compulsion also exists in reinsurer-PPIPs. ARPC (Australia) and GAREAT (France) require all insurers to cede all eligible policies to the PPIP. While cession is voluntary, insurers who choose to cede policies to Pool Re (UK) or ARPC-Terrorism (Australia) must cede all their eligible policies. Such mandates lessen adverse selection.

Trade-offs:

Demand-side mandates or compulsory bundling, which impose costs on consumers, are politically sensitive. Thus, PPIPs often combine them with solidarity pricing (New Zealand’s NHC, France’s CCR) or a low coverage cap (Türkiye’s TCIP) to keep prices down. Conversely, compulsion may be necessary to implement solidarity pricing, ensuring a diversified pool and avoiding adverse selection.

Compared to voluntary systems, compulsion ensures higher uptake, larger and more stable re/insurance pools, and thus lower prices, potentially aligning with social guardrails. However, compulsion restricts choice, weakens underwriting practices, and raises fiscal commitments, weakening both market and fiscal guardrails. It also requires enforcement to be effective, an operational constraint.

B. Pricing approach

In our sample, a PPIP’s pricing of disaster risk ranges from risk based (premiums match actual risk levels) to solidarity based (lowering premiums for high-risk groups).62

Key choices:

- Prices at the policyholder level: Insurer PPIPs set premiums directly. For reinsurer-PPIPs or backstops, direct insurers typically set risk-based rates, with some reinsurer-PPIPs introducing solidarity pricing at the reinsurance level. For JER (Japan) and CCR (France), however, direct insurance premiums are regulated and subsequently ceded to the reinsurer-PPIP.

- Who finances the subsidies:

- Internal subsidies come from within the PPIP’s own risk pool. This can happen through flat rates, where low-risk policies subsidise high-risk ones (France’s CCR); through pricing models that use broad risk zones that do not reflect risk at a granular level (Japan’s JER); or through rates that depend on sums insured (France’s GAREAT) or council tax bands (Flood Re in the UK). In Australia’s ARPC-Cyclone, a state guarantee lowers the PPIP’s overall costs. These savings are then used exclusively to lower reinsurance premiums for high-risk policies.

- External subsidies are financed by parties outside the pool. For example, Flood Re (UK) relies on Levy 1, an annual charge on all UK home insurers.

- Internal subsidies come from within the PPIP’s own risk pool. This can happen through flat rates, where low-risk policies subsidise high-risk ones (France’s CCR); through pricing models that use broad risk zones that do not reflect risk at a granular level (Japan’s JER); or through rates that depend on sums insured (France’s GAREAT) or council tax bands (Flood Re in the UK). In Australia’s ARPC-Cyclone, a state guarantee lowers the PPIP’s overall costs. These savings are then used exclusively to lower reinsurance premiums for high-risk policies.

Trade-offs:

Risk-based pricing creates economic signals that direct investment toward risk reduction, which respects the market guardrail. However, it is data-intensive and can entrench unaffordability in high-risk areas, potentially straining the social guardrail. Conversely, solidarity pricing improves affordability and uptake but weakens risk-reduction incentives and market discipline. It may also raise fairness concerns when subsidies do not benefit the most vulnerable.

PPIPs in practice: From creation to performance

This section discusses the drivers behind the creation of featured PPIPs; before assessing their real-world performance and how they navigate fiscal, market, social, and operational guardrails. Most PPIPs have succeeded in improving insurance availability, affordability, and uptake. Yet many struggle to stay within one or more guardrails. Some schemes have stifled private insurance markets while others have exposed the state to rising fiscal risk. Moreover, new or growing risks drive up loss volatility, testing the limits of even well-designed PPIPs, highlighting the need for greater risk reduction (Pillar 1), an issue explored in the next section.

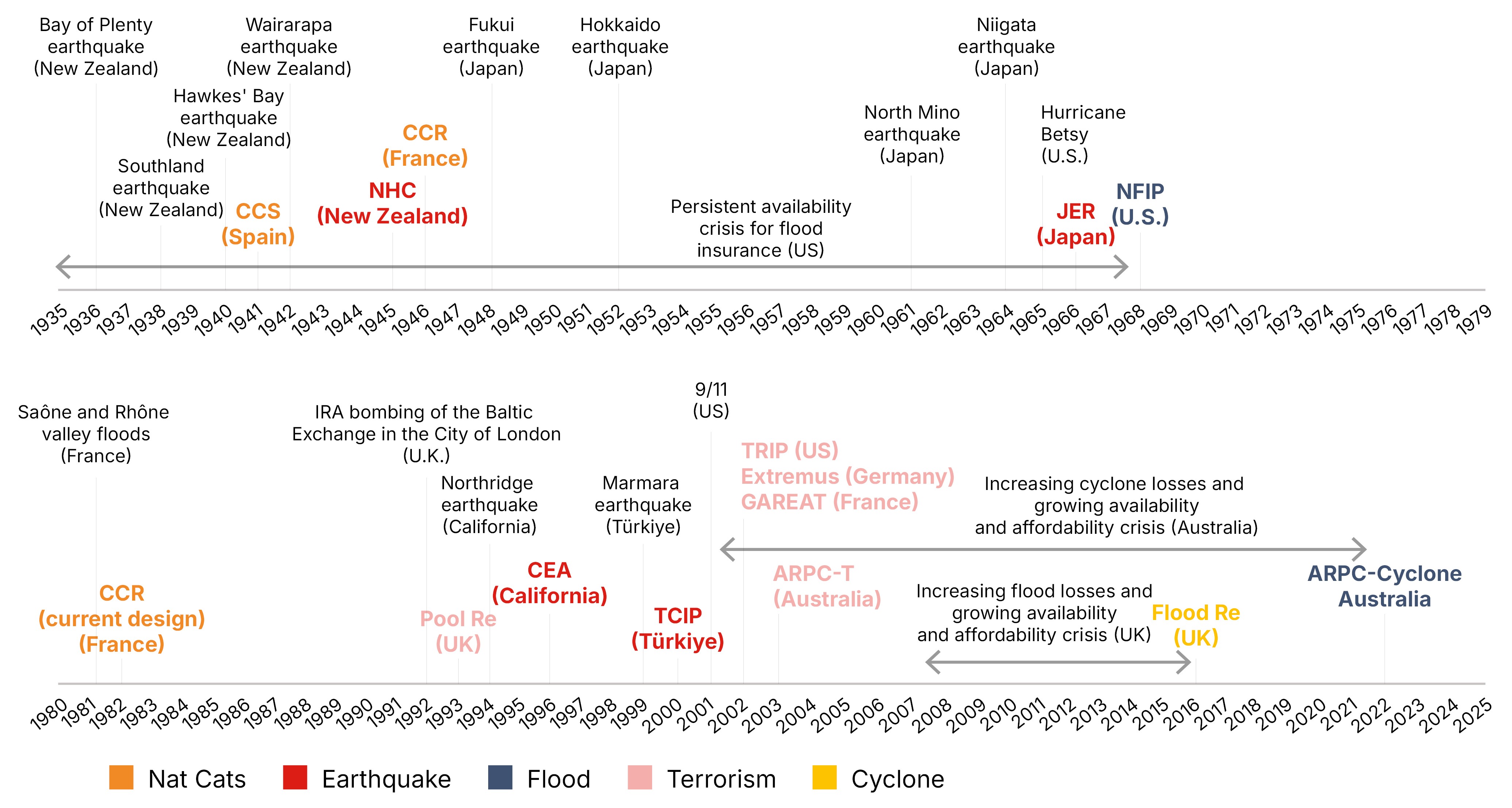

How crises catalyse PPIP creation

The history of existing PPIPs shows that a crisis often triggers their creation (see Box 3 and Figure 8):

- A costly disaster is often a catalyst. In some cases, a major loss event led re/insurers to sharply increase their prices or withdraw cover altogether. This prompted governments to introduce PPIPs to restore capacity and stabilise markets (including all five terror schemes and California’s CEA). In markets with low insurance uptake, however, the (sometimes repeated) cost of state relief led to the creation of a PPIP – often an insurer-PPIP – to increase coverage uptake and relieve governments of some future disaster losses.63

- For the more recent schemes, availability and affordability pressures act as a catalyst. For Flood Re (UK), an industry-government agreement ended, leading to a sudden withdrawal of private insurance for homes in flood-prone areas, amid rapidly rising flood losses that were already straining coverage affordability.64 Similarly, the creation of the ARPC-Cyclone (Australia) in 2022 was prompted by a chronic affordability and availability crisis for cyclone protection in Northern Australia. In both cases, the PPIP acts as a reinsurer, providing additional capacity to direct insurers.

Box 3: When a disaster triggers action

Four of the five terrorism-related schemes analysed – TRIP (US), GAREAT (France), Extremus (Germany), and ARPC-Terrorism (Australia) – emerged in the aftermath of the 9/11 attacks. The UK’s Pool Re was established in 1993 after the IRA bombing of London’s Baltic Exchange. These PPIPs addressed severe reinsurance shortfalls when terrorism risk, previously underestimated, became largely uninsurable, affecting critical sectors such as aviation, tourism, and commercial real estate lending.

Similarly, the four earthquake PPIPs were triggered by major earthquakes, often after private insurers had already withdrawn from the market (Japan, New Zealand) or where insurance penetration was minimal (Türkyie), following decades of costly losses. In California, home insurers are mandated to offer earthquake insurance alongside basic coverage, meaning that insurers cannot selectively withdraw capacity for earthquake risk. The CEA aimed to stabilise the homeowners’ market after insurer withdrawals following the 1994 Northridge quake, due to previously underestimated losses.

Finally, France’s CCR was implemented in 1982 after a series of severe floods between late 1981 and early 1982 revealed a significant protection gap, insurance being either too costly or unavailable.

Source: Geneva Association

Figure 8: Timeline of the creation of PPIPs

Source: Geneva Association

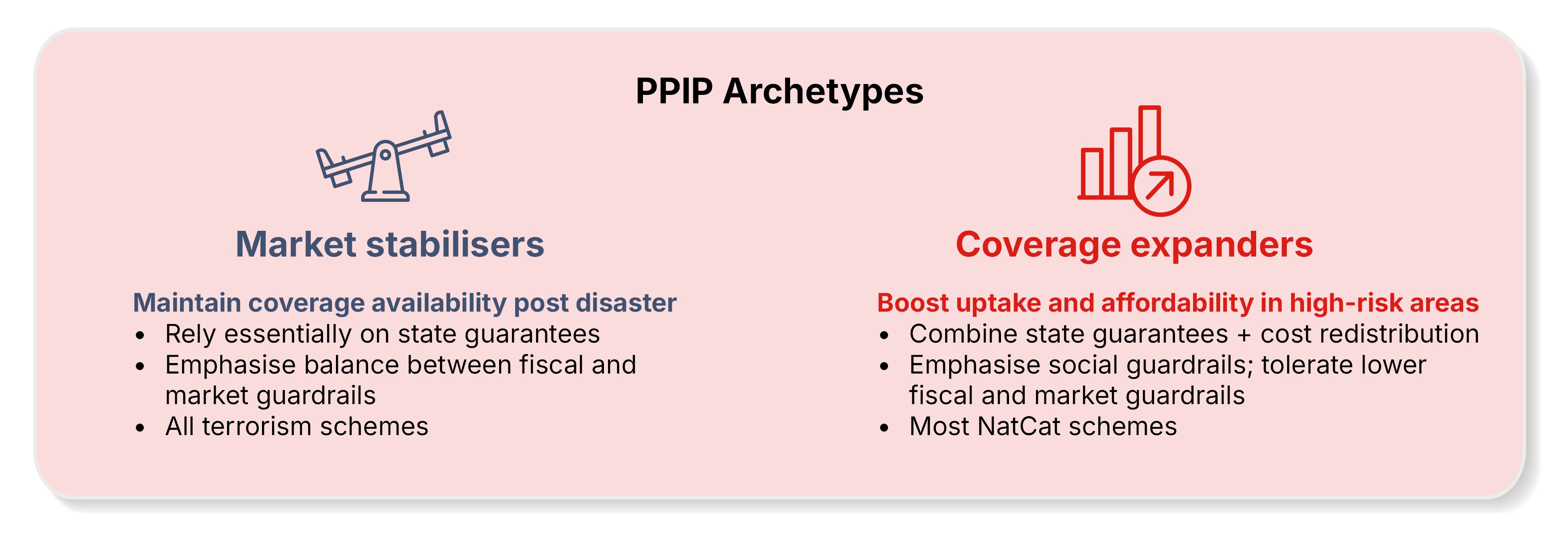

PPIP archetypes: Two ways of balancing policy trade-offs

When examining the performance of existing PPIPs, two archetypes emerge, reflecting different objectives and choices made regarding the policy trade-offs discussed earlier. Understanding these archetypes helps frame the assessment of their successes and challenges (Figure 9).

- Market stabilisers: Primarily created to restore insurance capacity after a market disruption (e.g. the 9/11 attacks, see Box 3). This archetype relies on state guarantees to help capacity grow back, including through the PPIP’s own capital. Market stabilisers often use voluntary participation and risk-based pricing, thus maintaining a balance between fiscal and market guardrails. This prevents a crunch in private-insurance availability from impacting other critical economic sectors, such as aviation or real-estate lending.

- Coverage expanders: Primarily focused on broadening insurance coverage, particularly in high-risk areas where uptake is chronically low (e.g. France’s CCR, New Zealand’s NHC) or – for more recent schemes – where rising losses erode availability and affordability (e.g. the UK’s Flood Re, Australia’s ARPC-Cyclone). This archetype typically combines state guarantees with cost redistribution, placing greater emphasis on social guardrails (affordability, access), sometimes at the expense of fiscal or market discipline.

Figure 9: Two PPIP archetypes

Source: Geneva Association

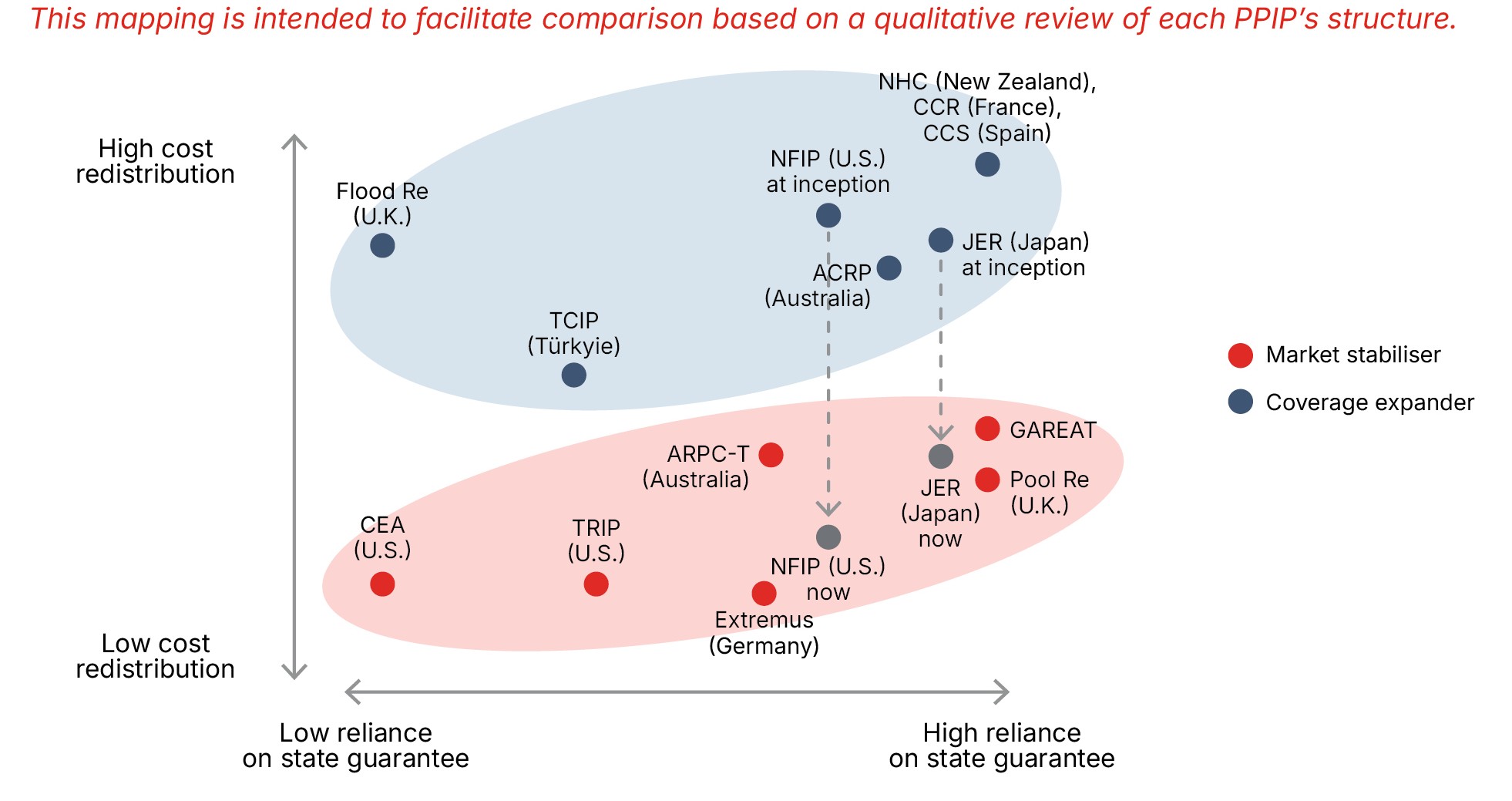

In our sample, all terrorism PPIPs, as well as California’s CEA (earthquakes), are market stabilisers (Figure 10).

Figure 10: State guarantees vs. cost redistribution and PPIP archetypes

- The horizontal axis reflects the state guarantee’s importance in a PPIP’s total claims-paying capacity. It is highest when state guarantees are unlimited.

- The vertical axis represents expert judgement about the degree of cost redistribution achieved through compulsion and solidarity pricing. Coverage expanders (blue cluster) exhibit significantly more cost redistribution than market stabilisers (red cluster). Note that NFIP (US) and JER (Japan) – two coverage expanders – have moved towards more risk-based pricing (NFIP since 2022, JER gradually since 1980), which is reflected in their changing positions.

Source: Geneva Association

Coverage outcomes: Successes and shortfalls

PPIPs with a market-stabiliser archetype have restored availability and price stability in markets experiencing reinsurance shortfalls or pricing spikes. Reviews of TRIP (US), ARPC-Terrorism (Australia), and Pool Re (UK) consistently highlight their role in preventing market failure.65 However, because most market stabilisers rely on voluntary coverage and risk-based pricing, protection gaps remain where coverage is expensive or potential customers lack awareness. For example, only 4% of UK SMEs carry terrorism cover.66 CEA (California) reaches fewer than 15% of homeowners.

Coverage expanders that combine compulsion and solidarity pricing achieve the highest coverage and improve affordability the most. NHC (New Zealand, CCR (France), and CCS (Spain), which use compulsory bundling and solidarity pricing, achieve uptake of around 90–95%.67 ARPC-Cyclone reduced cyclone premiums in high-risk areas by around one-third and raised quote success rates from 66% to 84% in its first year. Before Flood Re (UK), only 8% of high-risk households could obtain more than two quotes; now 99% can get fifteen or more.68

Conversely, coverage expanders that rely on voluntary participation struggle to increase insurance uptake. In the US, NFIP take-up is around 30% in flood zones. In California, 89% of policyholders opt out of the CEA’s earthquake coverage. In Japan, only 35% of households have fire insurance, although the earthquake add-on rate rose from 33% in 2001 to 70% in 2023, indicating increased risk awareness. Despite a purchase mandate, Türkiye’s TCIP’s weak enforcement leaves 40% of eligible households uninsured.

For both market-stabiliser and coverage-expander archetypes, moreover, protection gaps persist for perils and exposures outside scheme mandates. These include CBRN or cyber risks for some terrorism PPIPs, commercial property in earthquake schemes, or post-2009 homes and dwellings of over three units in Flood Re (UK). Likewise, because ARPC-Cyclone (Australia) only covers cyclone-related losses, property insurance prices keep rising or remain unaffordable in regions exposed to other types of flooding.69

Finally, these PPIPs were established to cover physical property damage and, in some cases, resulting business interruptions.70 Yet, corporate value has shifted to intangible assets and global supply chains.71 While property damage remains an important issue, new exposures, such as data loss and contingent business interruption, which are not tied to physical property damage, may require dedicated solutions.

Guardrails: Navigating trade-offs in practice

This subsection examines how PPIPs have navigated the four guardrails outlined in Section 3. Examining their performance through the lens of the guardrails reveals both successes and areas of strain. This often suggests a need for reform, a discussion that is ongoing for several PPIPs.

Fiscal guardrail: Preserving fiscal space

Well-designed PPIPs protect public finances by building capacity for routine losses and making the state a reinsurer of last resort. Across PPIPs, four patterns stand out:

- Some guarantees are rarely drawn upon. Terror PPIPs, which are market stabilisers, as well as several coverage expanders such as TCIP (Türkyie) and CCS (Spain), have never drawn on state guarantees. Their success rests on accumulated funds or strong private reinsurance programmes that effectively buffer the state guarantee.72 France’s CCR used its unlimited state guarantee once (in 1999, after the Lothar/Martin storm).

- Peril frequency and pricing drive fiscal risk. Where hazard frequency is lower, private and PPIP capacity grows, and triggering the state guarantee becomes less likely (e.g. terrorism PPIPs, New Zealand’s NHC until the 2010–11 Canterbury earthquakes, TCIP in Türkyie). Conversely, high-frequency or clustered events can drain a PPIP’s capital. For example, NHC required state support after the 2016 Kaikōura quake, following reserve depletion in the 2010–11 Canterbury sequence. France’s CCR has been running on low funds since 2023 after a particularly costly drought in 2022, and in a context of increasing losses (Box 4).

- When guarantees are over-relied upon, reform follows. Solidarity pricing in the coverage-expander archetype can generate financial losses or even deficits for PPIPs facing the growing strain of high-frequency perils, such as floods and droughts, thereby increasing fiscal exposure (e.g. CCR in France, NFIP in the US). After significant losses, PPIPs rebuild capital through higher premiums or levies (e.g. Japan’s JER after the 2011 Tohoku earthquake) and boost their claims-paying capacity by transferring more risk to private markets. Both New Zealand’s NHC and the US NFIP have turned to reinsurance and ILS in the past decade, once their debt burdens became unsustainable.73 Despite a USD 16 billion debt cancellation in 2017, however, the NFIP still owes over USD 20 billion, underscoring the need for structural reform.

- Temporary state guarantees often become permanent. For example, the NFIP (US) has been continually extended since 1968.74 Moreover, market uncertainty over a PPIP’s continuation may create industry pressure for repeated extensions (e.g. TRIP in the US).75

Market guardrail: Not crowding out private markets, ensuring insurers bear a sustainable level of risk, fostering market discipline and innovation

Successful PPIPs crowd in private capital without hollowing out market discipline. Four lessons emerge:

- Diversified pools attract private reinsurance. PPIPs that build large, diversified pools are more attractive to reinsurers and ILS investors. In Türkyie, TCIP’s growing pool size enabled it to cut reinsurance costs by 35% within five years. 76

- Capped public cover can stimulate private top-up markets. In New Zealand, after the Canterbury earthquakes, private insurer claims were double those of the NHC, showing how a capped PPIP coverage can help anchor a robust private market for top-up insurance.77 Where demand is chronically low, however, complementary markets struggle to appear (e.g. Türkiye’s TCIP, NFIP in the US).78