Cyber insurance contributes to cyber resilience not only by covering financial losses, but also by helping firms prevent, manage and recover from cyber incidents.

Suggested citation

Geneva Association. 2026.

Strengthening Cyber Resilience Through Insurance.

Author: Darren Pain and Sasha Romanosky. March.

2 min read

Key Findings

-

-

Through underwriting, risk assessments, guidance and incident-response services, cyber insurers can encourage stronger cyber hygiene and improved risk management practices.

-

Despite rapid growth in the cyber insurance market, significant protection gaps remain, particularly among small and medium-sized enterprises (SMEs), which often lack the resources to build robust cyber resilience capabilities.

-

Increasing awareness and utilisation of the prevention and response services embedded in cyber insurance policies could strengthen firms' ability to withstand and recover from cyber incidents.

-

Strengthening cyber resilience will require closer collaboration between insurers, policyholders, technology providers and governments to address increasingly interconnected cyber risks and support system-wide resilience.

Q&A

-

What is this report about and what are its main findings?

This report examines how cyber insurance can strengthen cyber resilience in an increasingly complex digital environment. It finds that cyber insurance provides value beyond financial compensation by helping firms identify vulnerabilities, improve cyber risk management, strengthen prevention measures and recover more effectively from cyber incidents. While the cyber insurance market has grown rapidly, wider adoption and greater use of insurer-provided resilience services could help address persistent cyber protection gaps.

-

Why does cyber insurance matter for cyber resilience?

Cyber insurance can influence behaviour before, during and after a cyber incident. Through underwriting standards, risk assessments, guidance and incident-response support, insurers encourage policyholders to strengthen cyber hygiene and invest in preventative measures. These capabilities can reduce the likelihood and severity of cyber incidents while improving firms' ability to respond and recover when attacks occur.

-

What are the implications for insurers and policyholders?

For insurers, the report highlights opportunities to expand cyber insurance adoption, strengthen risk assessment capabilities and develop products that better support prevention and resilience. For policyholders, cyber insurance can provide access not only to financial protection but also to expertise, tools and services that improve preparedness and response capabilities. Greater engagement with these services can enhance firms' overall cyber resilience.

-

How can cyber insurance help close cyber protection gaps?

The report identifies several ways insurers can support wider adoption of cyber insurance and stronger cyber safeguards. These include increasing awareness of cyber risks and vulnerabilities, particularly among SMEs; developing flexible and digitally accessible products; streamlining underwriting and claims processes; and partnering with cybersecurity providers to help identify and address vulnerabilities before incidents occur.

-

Why is collaboration important for managing cyber risk?

Cyber risks are highly interconnected, with incidents often affecting multiple organisations, sectors and supply chains. The report argues that strengthening cyber resilience requires closer cooperation between insurers, policyholders, technology providers and governments. Improved information-sharing, stronger risk management practices and coordinated approaches to emerging cyber threats can help build resilience not only at the firm level but across the wider economy.

7 min read

Authors

Darren Pain, Director of Research, Geneva Association

Sasha Romanosky, Senior Policy Researcher, RAND

Introduction

Cyber incidents are becoming more frequent and more costly. The median annual loss of a cybersecurity breach has risen 15-fold over the past 15 years, from USD 190,000 to nearly USD 3 million. Losses from major incidents have also grown sharply, exceeding an average of USD 28 million within the top 10% of loss events in 2024, almost five times the level recorded in 2008.1

Businesses increasingly identify cyber risk as a core operational concern. Yet many cyber incidents still stem from basic, preventable vulnerabilities such as susceptibility to phishing, weak passwords, unpatched software, and misconfigured systems. Insurers can play an important role in helping to raise firms’ cybersecurity hygiene and enhancing overall cyber resilience. However, cyber insurance penetration in certain market segments and regions remains low. Estimates suggest only around 10% of small and medium-sized enterprises (SMEs) globally have cyber insurance – and in some countries it could be much lower, especially among the very smallest firms.2

Cyber resilience and insurance

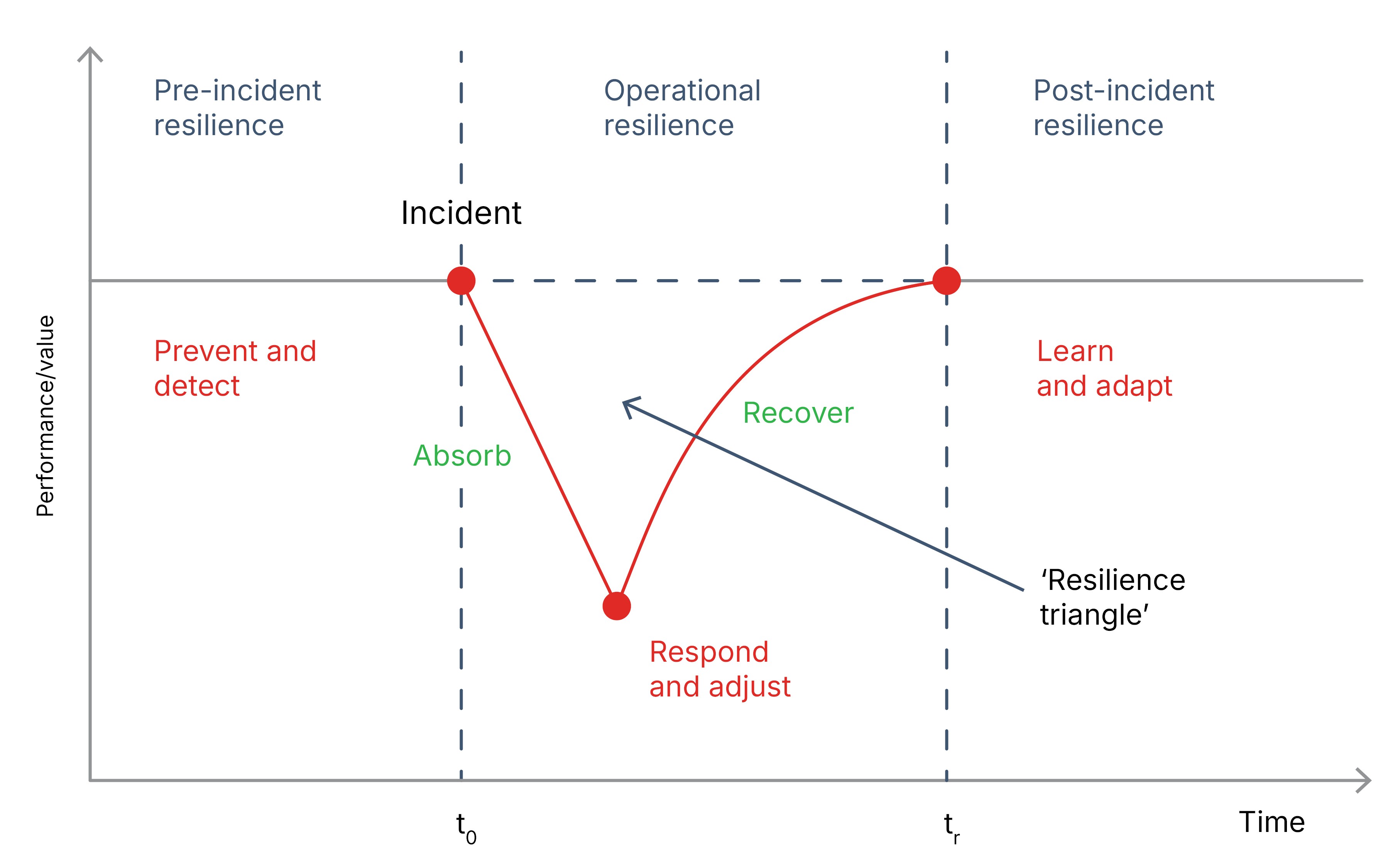

A ‘resilience triangle’ traces how a firm’s performance is impacted by an adverse disturbance. Depending on the structure of a firm’s systems, some shocks may be absorbed with no change in performance, if measures are in place to anticipate them and ameliorate their impact. But inevitably some disturbances will be unforeseen. Their effects will be determined by the firm’s ability to rely on backup systems, isolate parts of its business functions to limit the spread of any disruption, and access financial and physical resources to respond to and remediate the incident. The triangle framework reflects the actions a firm takes to build and maintain system resilience – before, during, and after a disturbance – and helps ensure reliability and maintain firm-level performance (sales, output, etc.) (see Figure 1).

Cyber insurance has evolved from being just a risk-transfer mechanism to also helping companies manage and reduce cyber threats and their impacts. Insurers require baseline security standards from policyholders. They may also bundle services, including security recommendations, cyber-risk monitoring and alerts, and payment for the costs of experts should an incident occur. In doing so, insurance can help firms ‘shrink the V’ of the resilience triangle by improving their pre-incident, operational, and post-incident resilience.

Unlike cybersecurity vendors, who might offer standalone warranties offering compensation should their specific product or service fail, cyber insurers have a vested interest in helping their policyholders minimise the full suite of losses from a cyber incident, including damages incurred by third parties. There is a feedback loop between advice, guidance, and coverage: prioritising more effective cybersecurity will, in turn, reduce insurance claims. Equally, if investing in cybersecurity enables an insurer to provide better coverage terms or more effective incident response support, the investment increases the value of cyber insurance.

FIGURE 1: A HOLISTIC VIEW OF RESILIENCE

Source: Geneva Association3

How effective is cyber insurance?

Empirical evidence suggests cyber insurers pay claims and influence insureds’ cybersecurity posture. One global study found that 92% of notifications of potentially covered losses fell within cyber insurance coverage.4 By comparison, UK insurers paid out on more than 90% of motor insurance claims, around 70% of claims on home buildings and contents policies, and a little over 50% of legal insurance claims.5

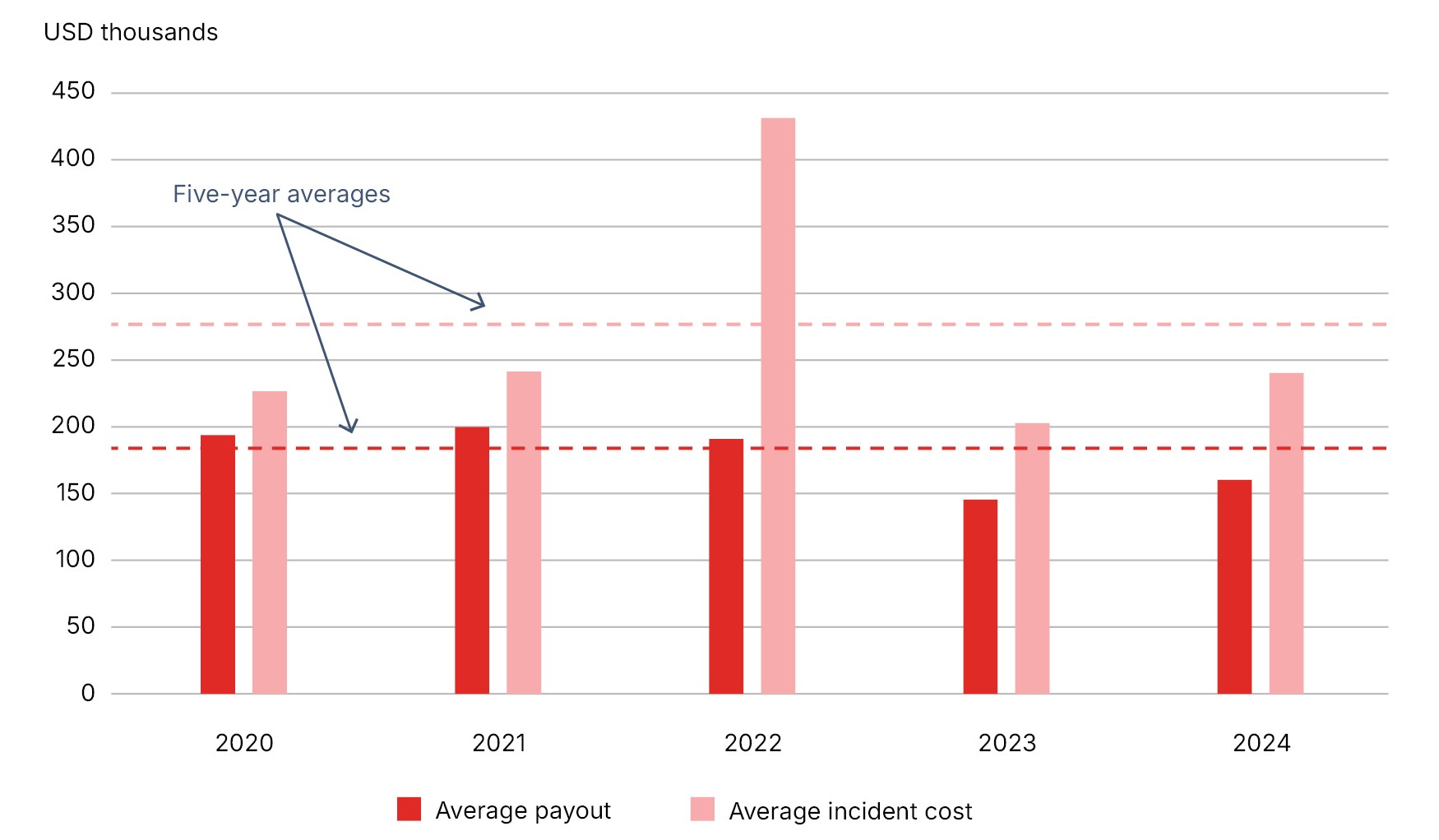

FIGURE 2: INCIDENT COSTS AND INSURANCE PAYOUTS TO SMES

Source: NetDiligence6

Data for the US, Canada, and the UK show that the average cyber insurance payouts represent a material share of overall incident costs, close to 70% in the case of SMEs (see Figure 2). Surveys and case studies also indicate that, through their underwriting procedures, cyber insurers have a positive impact on policyholders’ cyber hygiene. For example, a 2024 survey reported that nearly all organisations that purchased a cyber policy also invested in improving their cyber defences to optimise their insurance position. Over three quarters (76%) of surveyed companies increased cybersecurity investments in order to apply for cyber insurance.7

However, several market features still restrict the potential of insurance, on both supply and demand sides, to promote effective cybersecurity governance:

- Limits to risk differentiation. While underwriting practices have advanced in recent years, insurers still struggle to precisely differentiate insureds by their level of cyber risk. As a result, insurance terms and conditions do not always provide sharp incentives for firms with weaker cybersecurity to improve their controls.

- Practical obstacles to steering effective risk prevention and mitigation. Many insureds do not take advantage of insurers’ pre-incident security services. A recent survey found that nearly one third of respondents (32.5%) were unaware of any free risk management services included in their cyber insurance policy.8

- Misaligned incentives and institutional frictions. Efforts to manage risk after an accident or intrusion can also be undermined by potential conflicts of interest between insurers, intermediaries, and policyholders. For example, policyholders may not want to provide all the necessary information insurers need for loss adjustment, in case that reveals commercially valuable/sensitive data, or could lead to reputational harm and legal repercussions. A reluctance to share information undermines transparency and trust.

- Ambiguity surrounding potential catastrophic cyber events. The uncertainty over the likelihood and size of cumulative losses that might accompany a major cyber event – for example, possible accumulated claims from a common failure of IT systems or the contagious spread of malware – continues to restrict re/insurer appetite to underwrite cyber risks.

Fostering increased take-up of cyber insurance

Insurance can be a key enabler of a needed upgrade in firms’ cybersecurity as well as strengthening their capabilities to cope with cyber incidents, even if some peak cyber risks ultimately remain uninsurable. However, increasing the take-up of cyber insurance and enhancing its role as a vital tool in boosting overall cyber resilience, especially among SMEs, will require a combination of initiatives involving multiple stakeholders. These include:

- Raising awareness of cyber risks and the full benefits of coverage. Insureds’ risk profiles can be materially strengthened through the underwriting process and sustained engagement with their insurers, not least among SMEs, where the most significant risks are negligence and oversight. This suggests an opening for carriers (and brokers) to invest further in client education about cyber risks and the proactive and preventive cybersecurity options included in cyber policies. Forward-looking cyber insurers already understand this, stressing resilience in their interaction with policyholders.

- Tailoring cover to meet policyholders’ needs. Ongoing advances in underwriting practices will make tailored coverage options even more feasible, including protection against enforced shutdowns, fines and penalties imposed by regulators, and losses resulting from cyber-related property damage and business interruption. In particular, cyber insurers are increasingly looking at parametric and agreed-value solutions to speed up claim payouts for business interruption claims, either as add-ons to existing policies, or as standalone policies.

- Simplifying policy language, underwriting, and claims processes for SMEs. The priority should be to simplify the customer experience. As far as possible, this means crafting policies that are easy to understand, delivering a seamless onboarding journey for new policyholders, and streamlining underwriting and claims processes. For instance, insurers can target clear, jargon-free policy wording, adapted to local regulations and industry contexts, to ensure accessibility and relevance. More transparent policy wording would make it clearer what perils are covered and which exclusions apply. This will help to build trust between policyholders and insurers, and cement stable, long-term cybersecurity partnerships.

- Aligning distribution with customer preferences and risk profiles. As well as the cyber insurance product itself, the ways in which customers interact with cyber insurers and intermediaries should also be upgraded. New distribution models have already begun to emerge. In May 2024, the insurance broker Howden launched the first-of-its-kind SME cyber insurance platform.9 Several carriers have also introduced embedded cyber insurance offerings that bundle coverage with the purchase of IT services, software, or security products, in a bid to increase insurance penetration, especially among small firms.

- Partnering with digital infrastructure providers. Insurers need to invest further in high-frequency telemetry – automatic gathering and analysis of data from multiple sources, including networks, applications, endpoints, and cloud environments – to better assess their insureds’ IT vulnerabilities and cybersecurity postures. This includes deploying AI tools to improve pricing accuracy, reduce claims, and enhance the resilience-building capabilities of cyber insurance. The shift towards continuous underwriting will be aided by deeper connections between insurers, key infrastructure providers, and cybersecurity vendors.

- Collaborating with government agencies. Insurers possess rich data on incidents, losses, and vulnerabilities across industries; while government agencies often have access to classified or aggregated intelligence on emerging threats, attack techniques, and indicators of compromise. When these insights are shared securely and responsibly, firms benefit from earlier warnings, better risk assessments, and improved preparedness against emerging cyber threats. Beyond information sharing, insurers and governments can support the development and adoption of common cyber hygiene practices, which underpin eligibility for insurance coverage, including potential steps towards mandatory cybersecurity standards.

- Exploring initiatives to promote system-wide resilience. Major technology companies already use bug bounty programmes, offering rewards to external researchers for responsibly reporting security flaws, to improve vulnerability discovery. There is an opportunity for insurers to channel some cyber insurance premiums to fund bug bounty schemes directly. The potential cybersecurity gains might be significant if the skills of the ethical hacking community could be steered towards innovative defensive tools, such as automating vulnerability discovery or exploiting mitigation techniques. At the same time, operationalising such insurer-sponsored bug bounty programmes would take careful design and implementation, aligning the incentives of software vendors, policyholders, and insurance companies, while also overcoming any legal or regulatory hurdles.

Foreword

Cyber resilience is becoming a core requirement for organisations operating in an increasingly digital and interconnected economy. Cyber incidents are no longer exceptional events; they are a persistent feature of the modern risk landscape. The financial impact is rising sharply, with median annual losses from cyber incidents increasing roughly 15-fold over the past 15 years. Strengthening resilience – ensuring organisations can prevent, absorb, and recover from cyber disruptions – has become an essential priority for firms, insurers, and policymakers alike.

This report examines the growing urgency around cyber resilience, and the role insurance can play in strengthening it. Geopolitical tensions, the rapid adoption of cloud services and artificial intelligence, expanding digital supply chains, and increasingly sophisticated threat actors are intensifying the risk environment. Yet many incidents still stem from basic, preventable weaknesses such as phishing attacks, weak passwords, unpatched software, and misconfigured systems – highlighting persistent gaps in cyber hygiene and risk management.

Preparation alone is not enough: organisations must also be able to absorb cyber shocks, respond effectively, and recover quickly. Cyber insurance is a potentially powerful, though still under-realised, governance mechanism – one that can complement cybersecurity investment, incentivise better practices, and provide critical expertise and financial support when incidents occur, particularly for small- and medium-sized enterprises.

This report sets out practical recommendations to expand awareness, improve insurance design, enhance data sharing, and promote common cyber hygiene standards. By acting together, stakeholders can help ensure that cyber insurance continues to evolve into a trusted and effective tool for managing cyber risk and supporting resilience across the economy.

Jad Ariss

Managing Director

Executive summary

Cyber incidents are becoming more frequent and more costly. The median annual loss of a cybersecurity breach has risen 15-fold over the past 15 years, from USD 190,000 to nearly USD 3 million. Losses from major incidents have also grown sharply, exceeding on average USD 28 million within the top 10% of loss events in 2024, almost five times the level recorded in 2008.

Given geopolitical tensions, rapid digitalisation and use of artificial intelligence (AI), shifting regulatory requirements, and evolving threat actors, this trend is unlikely to reverse. Businesses increasingly identify cyber risk as a core operational concern. Yet many cyber incidents still stem from basic, preventable vulnerabilities such as susceptibility to phishing, weak passwords, unpatched software, and misconfigured systems.

Understanding cyber resilience goes beyond conventional risk management and the actions firms take to limit potential losses. Instead, resilience requires attention to how firms prevent, absorb, and recover from disruptions. Some shocks can be anticipated and mitigated in advance, but others cannot. The speed and scale of recovery depend on built-in redundancies and segmentation of IT systems, access to backup resources, and effective incident response (IR). More resilient organisations work to reduce both the depth and duration of performance losses following an incident, as well as to enhance their abilities to restore operational capacity and minimise any long-term damage to their reputation.

Cybersecurity investment and cyber insurance are complementary tools for strengthening resilience. Beyond providing financial compensation for losses arising from an incident, cyber insurance can positively shape firm behaviour and incentivise risk prevention and mitigation, especially among small and medium-sized enterprises (SMEs) who may have limited cybersecurity expertise. Insurers often require minimum security standards before underwriting, encourage risk controls during the policy period, monitor global threats and alert clients to vulnerabilities, and provide expert support in responding to and remediating breaches. As insurers observe cybersecurity patterns across many firms, they are also well positioned to promote resilience within the broader economy.

The market for cyber insurance has expanded rapidly, both in scale and scope of coverage, since it first emerged in the mid-to-late 1990s and especially over the past decade. During that time, it has persistently demonstrated its worth by paying claims, improving policyholders’ cyber hygiene through effective underwriting, and supporting IR. Data for the US, Canada and the UK show that cyber insurance payouts represent a material share of overall incident costs, close to 70% in the case of SME policyholders. Furthermore, insurance broker data indicate 92% of notifications of potential losses fell within cyber insurance coverage, which compares favourably to other insurance lines.

However, the promise of a more powerful governance role for cyber insurance – where insurers proactively raise security awareness among their customers, incentivise continuous improvements in cybersecurity, and help expedite recovery when cyber defences are breached – is yet to be fully realised, particularly among SMEs, where adoption is low. Most insurers still struggle to accurately assess cyber risks and how they are evolving due to limited visibility into clients’ internal security environments as well as the fast-moving threat landscape. Meanwhile, policyholders often underuse pre-incident risk prevention services, due to limited awareness, operational constraints, or concerns that sharing information may affect future pricing and coverage. The involvement of third-party service providers during IR can add legal and operational complexity at moments when speed and coordination are essential.

Ultimately, some cyber risks are simply uninsurable because the scale and/or uncertainty about potential losses is too great for insurers to underwrite. Nonetheless, cyber insurance can be a key enabler of the needed upgrade in cybersecurity to cope with more routine and often preventable cyber incidents that can still be highly disruptive.

Expanding the uptake of cyber insurance and enhancing its role as a vital tool in boosting firms’ overall cyber resilience, especially among SMEs, will require coordinated action across insurers, firms, intermediaries, technology providers, and government. Key priorities include:

- Improving awareness and education of cyber risks and the preventative services embedded in insurance policies, particularly for SMEs with limited technical capacity.

- Developing more flexible and accessible insurance products, including clearer coverage terms and innovative approaches such as parametric or agreed-value solutions for business interruption.

- Streamlining underwriting and claims processes and clarifying policy language to ensure ease of understanding and relevance across sectors and jurisdictions.

- Modernising customer engagement, including digital distribution channels that simplify the buying process for brokers and smaller firms.

- Partnering with IT and cybersecurity vendors to access high-frequency data on vulnerabilities and support more accurate, continuous cyber risk assessment.

- Working with government to promote common cyber hygiene standards that can form the basis for coverage eligibility and security expectations.

- Supporting systemwide resilience initiatives, such as funding coordinated vulnerability discovery (e.g. bug bounty programmes) or advancing automated defence tools.

The insurance sector is already making progress in many of these areas. By helping establish and reinforce widely adopted standards of good cyber hygiene, cyber insurance can evolve into a more trusted and effective mechanism for building resilience across companies, industries, and economies.

Introduction

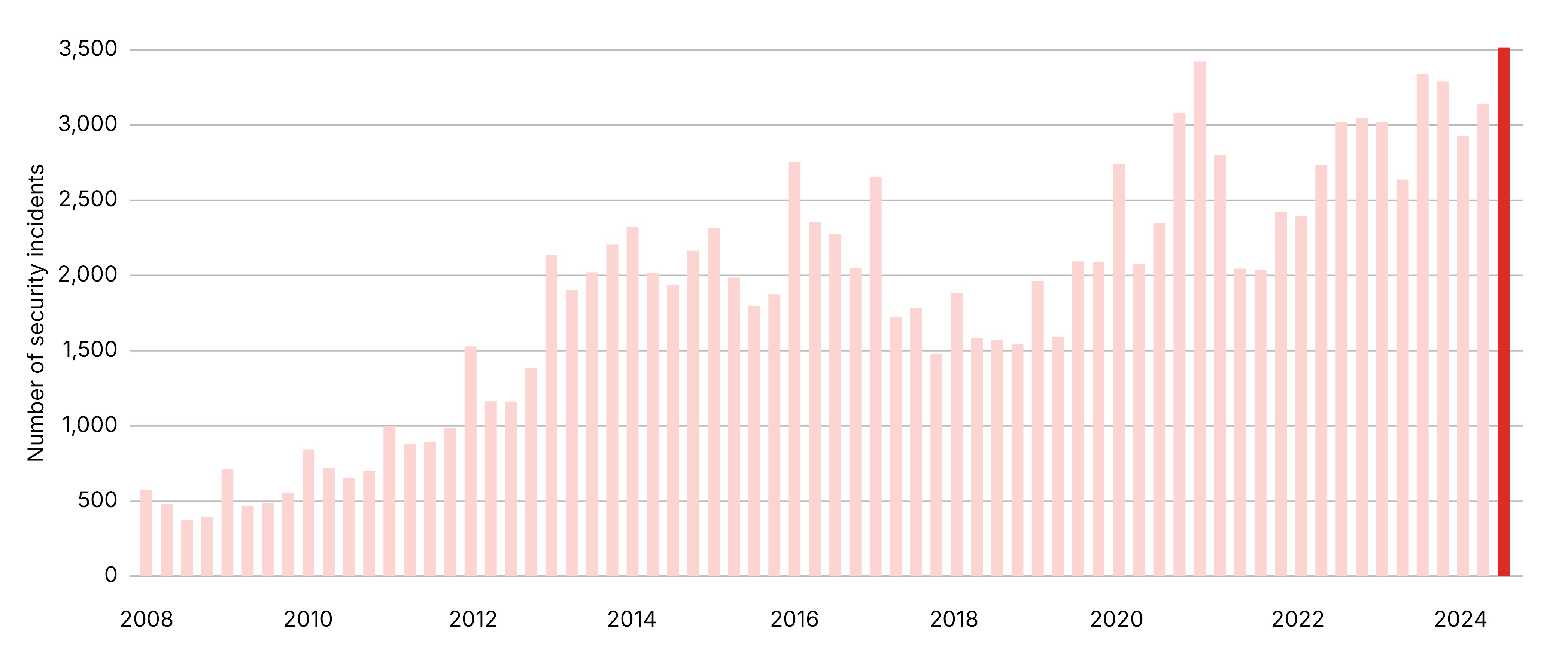

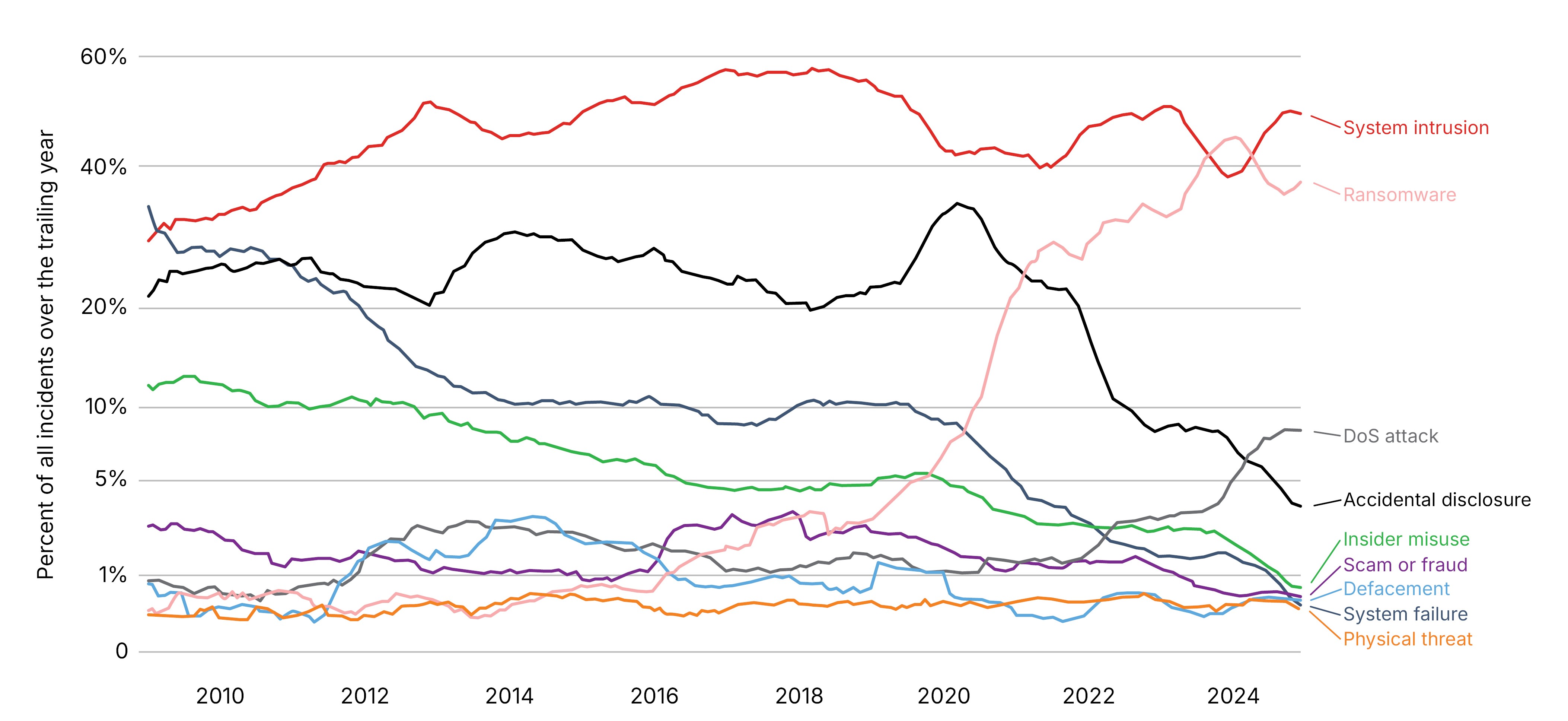

The cyber risk environment appears to be worsening. According to published data, while the overall number of cyber incidents varies year-on-year, there has been a clear upward trend over the past two decades (see Figure 1).1 Malicious cyber operations are becoming ever more prolific – ransomware and distributed denial of service (DDoS) attacks accounted for close to 50% of events in 2024 and contributed most to the increase in incidents over the past five years (see Figure 2). Moreover, many cyberattacks go unreported.2

Figure 1: GLOBAL CYBERSECURITY INCIDENTS PUBLICLY REPORTED OR DISCOVERED EACH QUARTER

Sources: Cyentia, Feedly Threat Intelligence (Q4 2024)

FIGURE 2: GLOBAL CYBERSECURITY INCIDENTS PUBLICLY REPORTED OR DISCOVERED EACH QUARTER

Source: Cyentia

Indicators of severity (based on partial data) likewise suggest cyber incidents are becoming more expensive. One study estimates the annual median loss from cybersecurity incidents has risen 15-fold over the past 15 years, from USD 190,000 to almost USD 3 million.3 The financial impact of major incidents has likewise increased markedly. In 2024, the average loss among the top decile of events surpassed USD 28 million – nearly five times the levels recorded in 2008.3

Cyber risks are a growing business concern

With geopolitical tensions, increasing digitalisation, an evolving regulatory and privacy law landscape, and a constantly changing group of threat actors, businesses see little prospect of a reversal of these trends. The Allianz Business Barometer ranked cyber as the top global risk in 2025, marking its fifth consecutive year at the top. Ten years ago, cyber risk ranked only eighth globally with 12% of responses, compared to 42% in 2025.5

The rapid adoption of emerging technologies such as AI only seems likely to amplify cyber risks as cybercriminals and other cyber adversaries successfully harness them to achieve greater sophistication and scale. While AI has benefits for security professionals, it supercharges the abilities of malicious actors, even among technically unsophisticated cybercriminals (see Box 1). AI can improve the targeting of vulnerabilities such as legacy systems, under-resourced IT departments, and human error.

Box 1: Generative AI and cybercrime

Generative AI (GenAI) is a double-edged sword for cybersecurity: it strengthens the capabilities of both attackers and defenders, making the threat landscape more dynamic and challenging. On the defence side, it can enhance threat detection, automate incident response, and improve vulnerability analysis. Simultaneously, it can increase the speed, scale, and sophistication of cyberattacks, by enabling:

- Malware creation and code generation. GenAI models can create malicious code that previously required advanced expertise. While humans still need to prompt GenAI to create malware, improving models and datasets increase the potential for self-evolving malware that can evade traditional security measures.6

- More sophisticated phishing and social engineering. Hackers can use GenAI to craft highly convincing phishing emails and messages, particularly personalised, context-aware content.7

- Attack automation and scaling. GenAI can automate reconnaissance, vulnerability identification, and execution of attacks. This includes hunting for security loopholes and vulnerabilities in applications and systems, and autonomously deploying malware.8

As corporates integrate GenAI technologies into their own operations, they also potentially increase their vulnerabilities to cyber intrusions. Context poisoning and prompt injection – techniques using carefully crafted inputs to manipulate how a model responds and change its behaviour – represent a growing threat vector.9 The increasing adoption of agentic AI, with added layers of autonomous decision making, is likely to amplify cybersecurity risks.10

Source: Geneva Association

It is not just that cyberattacks are growing in volume and creativity. The attack surface is expanding as more companies rely on a dense web of third-party vendors, each one a potential threat vector. In 2024, 23.3% of all cyber incidents were caused by intrusions through third-party IT and technology companies, up from 10.9% in 2020, highlighting the growing indirect threat of compromised supply chains.11 Increased reliance on cloud computing capabilities opens up another key operational vulnerability, especially among SMEs, who are often critically dependent on such services.12 Managed service providers (MSPs), which oversee their clients’ systems, are another potential entry point increasingly targeted by cyberattackers.13

Many firms underinvest in cybersecurity

Despite growing cyber risks, established security weaknesses remain common, such as phishing emails, weak or reused passwords, unpatched software, and misconfigured systems. Targeting such vulnerabilities remains highly effective because many organisations still struggle to implement basic cybersecurity hygiene (e.g. effective firewalls, intrusion detection, or employee training). The Identity Theft Resource Center (ITRC) reports that more than 94% of data breaches in 2024 could have been prevented with simple cybersecurity protocols like multifactor authentication (MFA – a security method that requires users to provide more than one form of authentication to access an account).14

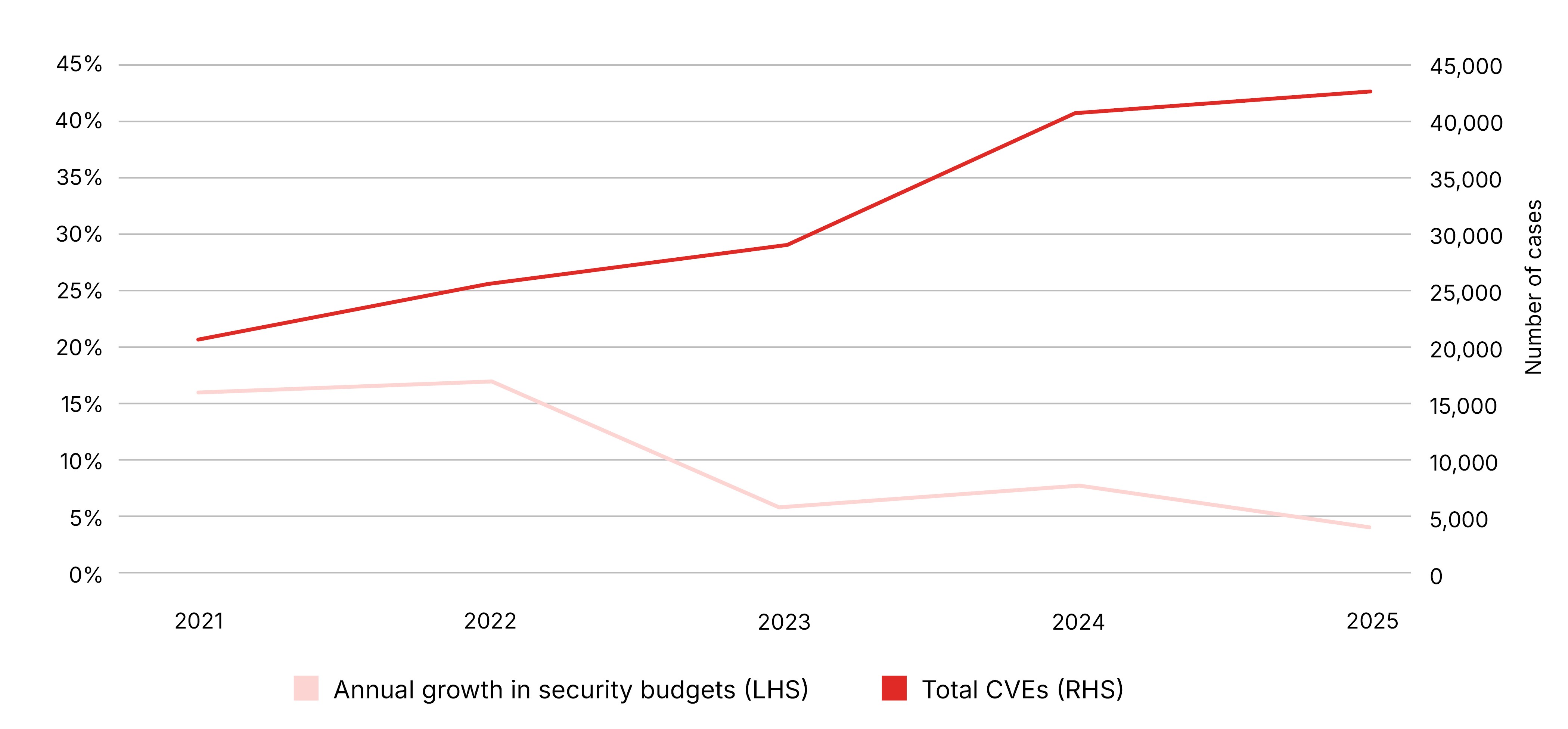

Many companies lack awareness of how rapidly cybercriminal business models evolve to exploit known and newly discovered weaknesses in IT systems. This is reflected in declining annual growth in security budgets in recent years, despite continuing security vulnerabilities (Figure 3).

FIGURE 3: GLOBAL CYBERSECURITY SPENDING VERSUS RISING IT VULNERABILITIES

Common vulnerabilities and exposures (CVEs) is a standardised dictionary/list of publicly known cybersecurity flaws.

Source: IANS and SecurityScorecard

Insurance as a risk governance mechanism

Insurance can play an important role in boosting cyber resilience, enabling firms not only to withstand an adverse disturbance (i.e. robustness) but also recover afterwards.15 Besides compensating financial losses arising from a malicious or accidental incident, insurance can align incentives to upgrade risk prevention and provide resources and expertise to expedite remedial actions, mitigate losses, and hasten recovery. That applies not just to direct or indirect victims of a cyber incident who might shoulder most of the associated costs. It also includes encouraging strong security guardrails among MSPs, cloud platform providers, and hardware/software developers.

Box 2: Cyber insurance

Cyber insurance first appeared in the mid-to-late 1990s. Originally providing protection against liability claims from customers or business partners for harms caused by online content or data breaches, the scope of coverage has progressively broadened. Cyber policies now typically offer both first-party coverage (for own company losses like business interruption and data recovery) and a wide range of third-party liabilities, including expenses incurred during litigation and regulatory investigations. Cover can be purchased either as an endorsement to existing insurance or as a standalone cyber policy.

Notably, coverage has expanded to include claims arising from business practices, not just security breaches. For instance, protection against liability for wrongful collection – unauthorised or improper gathering of personal data – is often included in cyber insurance. More recently, some cyber policies now cover specific GenAI risks such as malicious interference with a firm’s AI training data (i.e. data poisoning) and potential liability claims from third parties alleging copyright or intellectual property infringement.16

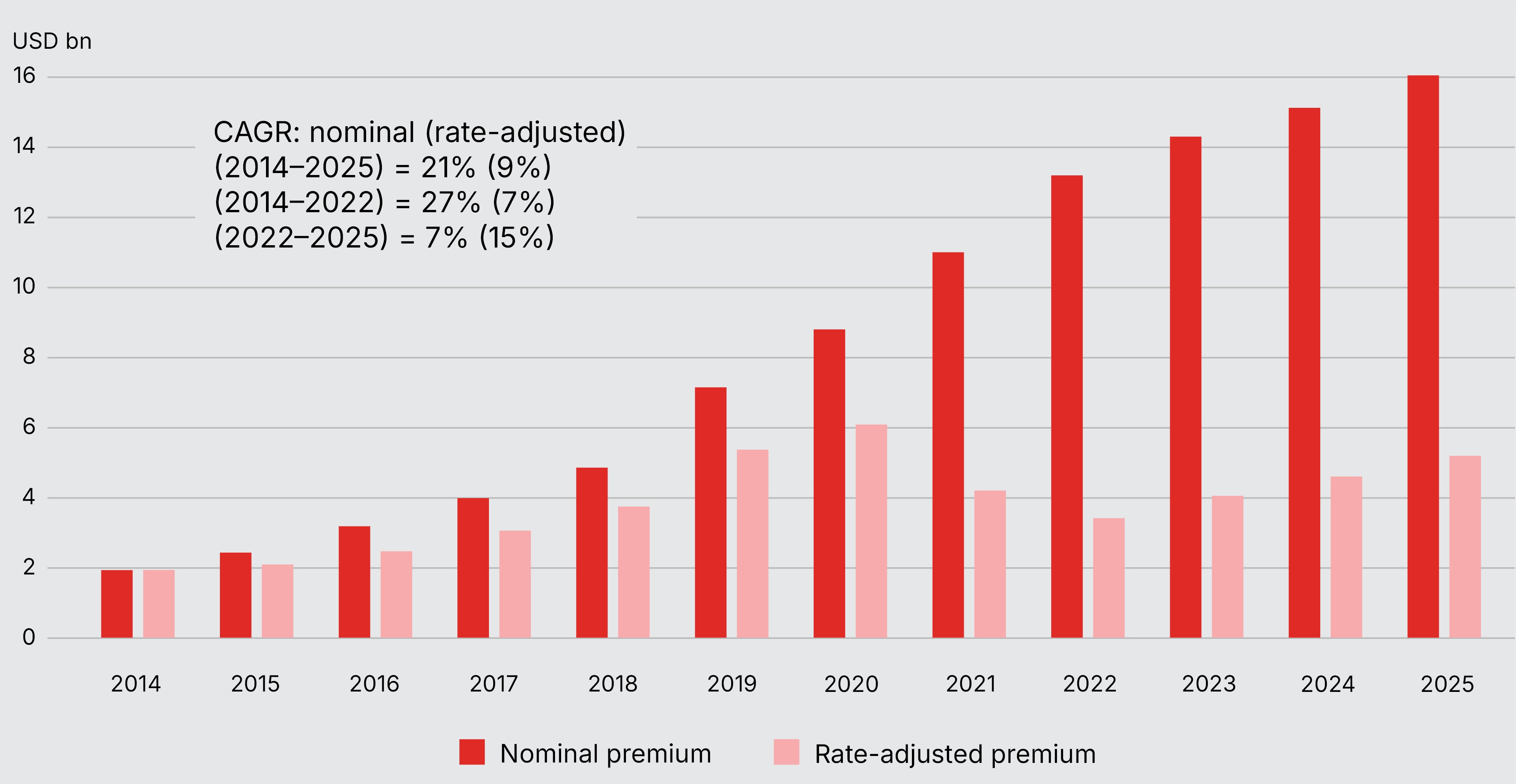

The standalone cyber insurance market has grown rapidly, especially over the past decade. Globally, premiums were worth around USD 16 billion in 2025, up from less than USD 1.5 billion in 2013. North America is the dominant region, commanding approximately two thirds of all cyber premiums. Europe is the second largest region, with a 21% premium share, while APAC is the third-largest market for cyber premium with a 10% share.17

FIGURE 4: GLOBAL CYBER INSURANCE PREMIUM GROWTH (2014–2025)

Source: Geneva Association, based on data from Howden and Swiss Re

Despite its rapid growth, cyber insurance still represents only around 1% of total property and casualty insurance revenues. Moreover, much of the market’s recent expansion reflects higher premium rates in 2021 and 2022, when strong demand for protection pushed up the cost of coverage. As a result, rate-adjusted (i.e. real) premium growth was far lower than headline nominal growth (see Figure 4). Over the past two years, this has reversed: rising risk exposures have offset falling rates to support overall market growth. Future expansion will largely depend on boosting uptake in currently underserved regions and market segments.

Source: Geneva Association

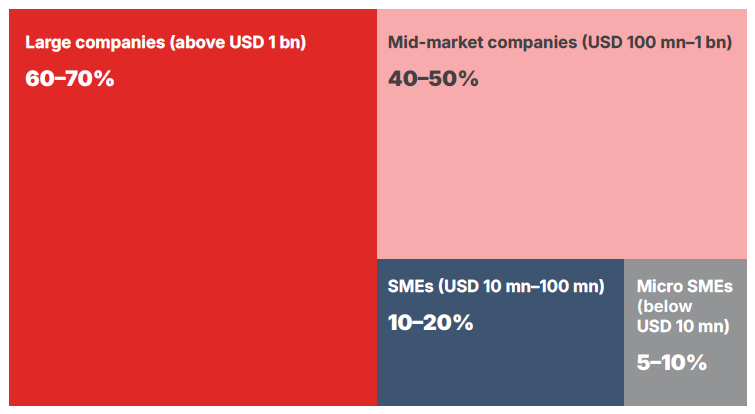

Different insurance policies may respond to a cyber incident depending on the specific policy wording, how the incident occurred and the losses that arise. As discussed in Box 2, a dedicated market for cyber insurance – the main policy intended to cover financial losses arising from cyber incidents, including those caused by third-party vendors – has developed rapidly. However, cyber insurance penetration in certain market segments and regions remains low. Estimates suggest only around 10% of SMEs globally have cyber insurance – and in some countries it could be much lower, especially among the very smallest firms.18,19 Data from the North American and European markets show that cyber insurance take-up remains well below 10% for micro SMEs (Figure 5).20 This is the case even though many have trouble safeguarding their cybersecurity. According to the World Economic Forum (WEF), 35% of small organisations believe their cyber resilience is inadequate, a proportion that has increased sevenfold since 2022.21

FIGURE 5: PERCENTAGE OF EACH CUSTOMER SEGMENT PURCHASING CYBER INSURANCE – NORTH AMERICA AND EUROPE

Source: Swiss Re

Report structure

Against this background, this report investigates how insurers can play a larger role in strengthening firms’ resilience against cyber incidents, and how market developments could reinforce the value proposition of cyber insurance.

Section 2 of this report discusses the notion of cyber resilience and how firms can bolster resistance against cyber intrusions and system failures, as well as how to recover should they experience an incident. Section 3 considers how insurance can support resilience building, not only through indemnification of losses but also in the provision of vital pre- and post-incident services. Section 4 evaluates the resilience benefits of cyber insurance, how its role could be enhanced, and how adoption could be increased, especially among SMEs. The final section provides concluding remarks.

Understanding cyber resilience

Resilience describes how well a system maintains its structure and continues to function in the face of a disruption (see Box 3). The less it will be affected by a disturbance – both in terms of the degree and duration of any dysfunction in operability – the more resilient is the system. The state of a system depends on how it was designed and how it is operated. These choices influence whether and how output/service is degraded during a disruption, how quickly it recovers, and how completely it recovers. Like physical capital, the stock of resilience may depreciate naturally over time as new weaknesses or vulnerabilities emerge.

Box 3: Roots of resilience

Resilience is a widely used term, but its meaning can vary depending on the context. It entered into the English language in the early 17th century from the Latin verb resilire, meaning to rebound or recoil. Early uses were often related to the ability of materials to withstand severe conditions.22 Modern-day applications of resilience emerged independently in ecology, psychology, and the social sciences in the 1970s.23 The common thread is interactions within and among complex systems. At its core, it refers to “[t]he capacity of a dynamic system to adapt successfully to disturbances that threaten system function, viability, or future development of the system.”24

Resilience in human and natural systems is often associated with sustainability in the face of constant change. That typically involves two kinds of response:

- Adaptation: Supports the resilience of a system by helping it stay in essentially the same state.

- Transformational change: If the maintained state becomes untenable, the system may move to a different stable state. Resilience is not always a matter of bouncing back, it may also suggest bouncing forward to a new state.

Narrow interpretations of resilience stress the ability to accommodate and recover from abnormal threats and events, be they enemy actions, natural disasters, or economic shocks. Broader definitions embrace awareness, detection, communication, reaction (and if possible, avoidance), and recovery.

Source: Geneva Association

The resilience triangle

The resilience triangle conceptually traces how a firm’s performance is impacted by an adverse disturbance. Depending on the structure of a firm’s systems, some shocks may be absorbed with no change in performance, perhaps because measures are in place to anticipate them and ameliorate their impact. Inevitably, however, some disturbances will be totally unforeseen. Their effects will be determined by the firm’s ability to rely on backup systems, isolate parts of its business functions to limit the spread of any disruption, and access financial/physical resources to respond to and remediate the incident. The triangle framework reflects the actions a firm takes to build and maintain system resilience – before, during, and after a disturbance – and helps ensure reliability and maintain firm-level performance (sales, output, etc.) (see Figure 6).25

Figure 6: A Holistic View of Resilience

Source: Geneva Association26

In the context of cyber incidents, a firm must decide how to manage the risk that a cyber event could seriously disrupt its operations (and ultimately impair its economic value). This involves the measures it can take to avert a cyber incident as well as those it can deploy to recover should it be hit. These actions might include investing in tougher cybersecurity controls, reconfiguring business processes and supply chains, taking steps to reduce legal or regulatory liability, and purchasing insurance to protect against unforeseen events.

2.1.1 Pre-incident preparedness

Pre-incident (preventive) cybersecurity controls include intrusion prevention and detection systems (see Box 4), as well as training programmes to reduce the risk caused by staff. Verizon estimates human factors – including phishing, intentional misuse by insiders, unintentional actions (e.g. unintended downloads of malware, software/hardware misconfigurations), and compromised user credentials – play a role in about 60% of all data breaches.27

Box 4: Types of cybersecurity controls

Pre-incident: Firms deploy tools and procedures to safeguard their cybersecurity, including:

- Intrusion detection and prevention systems (IDS, IPS, IDPS) which alert the firm to attempted cyberattacks and aim to actively block potential malicious threats in real time.

- Firewalls and perimeter access controls to prevent unauthorised activity.

- Endpoint detection and response (EDR) to help guide the firm to detect and remediate threats on endpoints – physical devices connected to a network, such as mobile phones, desktops, laptops – before they can spread throughout the network.

- Vulnerability management to prioritise patching and mitigation of software vulnerabilities.

- Security information and event management (SIEM) systems to act as a central collection point of all cyber activity across a firm and help separate benign from malicious activity.

During an incident: Containment practices and technologies are used to identify, isolate, and limit the initial impact of cyber incidents, such as identifying malicious activities swiftly, isolating affected areas, and preventing the spread of the threat to other parts of the network or connected systems. Forensic software and hardware solutions are used to search for and analyse digital evidence of an incident. These tools help in recovering, preserving, and analysing data from various electronic devices to identify the root cause, understand attacker tactics, and restore or repair systems.

Post-incident: Recovery strategies and backups are used to restore systems and data after a cyberattack or other disruptive events. These tools help minimise downtime, prevent data loss, and get operations back to normal quickly. Key tools include backup and recovery solutions, incident response plans, and cybersecurity awareness training.

Source: Geneva Association, RAND

Zero trust principles, operating on the basis that no user or system should be automatically trusted, can enhance cybersecurity. Unlike traditional security models that rely on a defined network perimeter, zero trust requires continuous authentication, authorisation, and validation of security configurations before access is granted to applications and data.

2.1.2 Operational resilience

Operational resilience captures the main component of the resilience triangle, depicting a firm’s reaction to a disturbance, the magnitude of its effect on the firm’s value or output, and the speed and form of recovery.

If prevention security controls are insufficient, the immediate fallout will depend on the degree of redundancy in a firm’s IT systems and its ability to run back-up processes to ensure operational continuity. Post-incident response and associated costs will be influenced by the firm’s ability to assess the nature and scope of the incident and activate incident response plans to absorb and contain the harms as well as the associated financial costs.

Once the incident has been contained, the firm engages recovery controls to repair and restore any affected systems. Expediting remedial actions will limit damage to the firm’s productivity (i.e. reduce the magnitude and duration of the initial disruption and reduce the downward leg of the triangle) and influence its recovery path. Recovery controls include digital forensics to identify any affected IT devices, cleaning and repairing those devices, restoring data from backups, as well as reconfiguring business processes and supply chains, and acting to reduce legal or regulatory liability.

2.1.3 Post-incident recovery

Even though a firm may fully restore its operational capabilities following a cyber incident, residual effects may linger. For example, an incident such as disclosure of confidential customer or corporate information may undermine trust in the firm, affecting its brand and future sales or profitability. As a result, even if the firm’s operations are restored, the demand for its goods or services, and hence actual output, may be significantly impacted. Companies hit by a cyber event could also face persistent effects on the cost and availability of finance.28

In addition, other parties beyond the firm could be harmed by a cyber incident, justifying a civil or criminal legal claim. Such liability can be costly and affect the future financial viability of the firm. The firm may also be subject to regulatory fines or fees that could have further financial or organisational repercussions. For example, the US Federal Trade Commission often imposes, in addition to pecuniary sanctions, cybersecurity audit and consent orders for up to 20 years following an enforcement action.29

The reputational fallout from cyber incidents is a growing concern (see Table 1). According to a recent survey by Hiscox, 61% of those responsible for their firm’s cybersecurity believe that reputational damage from a cyberattack would significantly damage their business. Close to two thirds (64%) believe they risk losing business if they do not handle client and partner data securely.30

TABLE 1: SURVEY VIEWS ON THE IMPACT OF CYBERATTACKS (% OF SURVEY RESPONDENTS CITING A FEATURE)

2024 | 2023 | |

| Greater difficulty in attracting new customers | 47 | 20 |

| Lost customers | 43 | 21 |

| Bad publicity, which impacted brand reputation | 38 | 25 |

| Lost business partners | 21 | 16 |

Source: Hiscox

Beyond conventional risk management

While resilience is closely related to risk management, the two are not the same. Risk management focuses on the actions firms take before an uncertain event occurs to limit potential losses. These actions typically include reducing risk (for example, lowering the likelihood or size of losses through operational safeguards), financing risk (such as building financial reserves), and transferring risk to others (for example, through warranties or insurance). In combination, these measures aim to bring risk exposure within acceptable tolerance levels.

By contrast, resilience describes the effectiveness of the firm’s preventative measures and how well it copes after a risk has materialised. Once an event occurs, uncertainty is no longer about whether it will happen, but about how severe its impact will be. Resilience, therefore, describes a firm’s ability to prepare for, absorb and recover from operational and financial shocks in order to ensure their long-run sustainability.

The geometry of cyber resilience

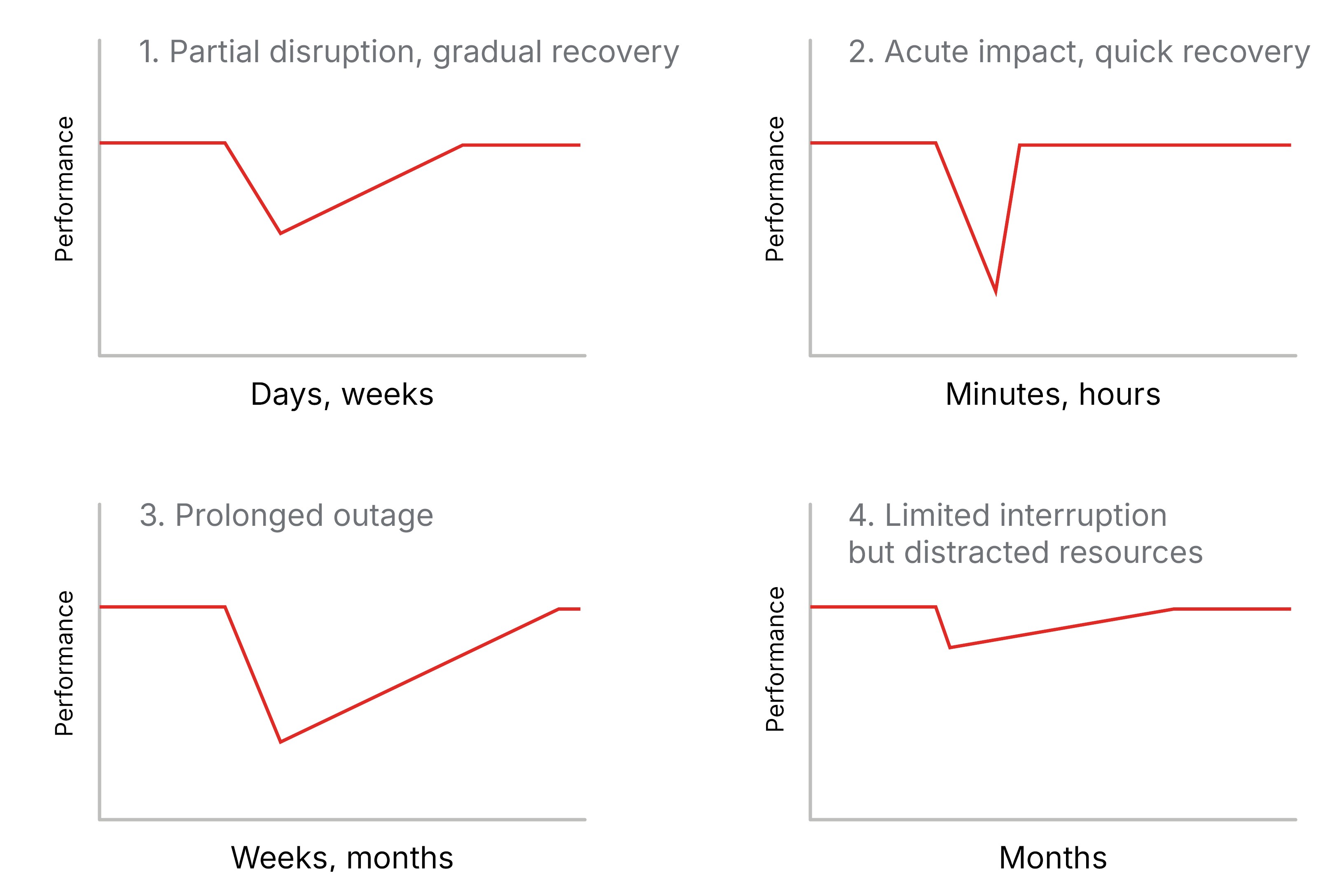

A firm’s resilience to a particular adverse event – and therefore the shape of the resilience triangle – will be influenced by: 1) its ability to reduce the probability of a successful intrusion or IT failure; 2) its ability to absorb the impact of that event; and 3) the time taken to fully recover from that event. Firms will be affected differently by different kinds of cyber incidents, and any one cybersecurity control may prevent or mitigate multiple kinds of adverse events.31,32 Figure 7 outlines some notional resilience archetypes that illustrate different effects of incidents on firm performance.

Figure 7: Resilience archetypes

Source: RAND

- Partial disruption, gradual recovery.

A firm suffers a relatively modest cyber incident, then recovers gradually over a period of days or weeks. Most ransomware attacks would fall into this category, given that these attacks typically target some, but not all, of a firm’s operations, with firms experiencing an average recovery time of 21 days.33 A 2024 IBM/Ponemon survey suggested 60% of firms took between 100 and 150 days to fully recover from a cyber incident.34

- Acute impact, quick recovery.

This case reflects incidents that have an intense effect on a firm’s output or performance but are resolved quickly. For example, DDoS attacks are usually temporary, typically lasting under 20 minutes, though some can extend to several hours.35 Even one of the most serious and widespread DDoS incidents (the 2017 Dyn DDoS attack) lasted less than a day.36

Similarly, network or cloud service outages can dramatically affect a firm’s services (either public facing, or internally). While they have the potential to cause losses across all of a cloud provider’s customers, the effect on a single firm is generally short-lived. For example, the Amazon AWS outage in October 2025, while highly disruptive for affected firms, lasted around 15 hours.37

For most firms, the CrowdStrike incident of July 2024 would also be characterised as an acute impact with quick recovery.38 A faulty software update caused a critical failure in Windows operating systems, but there was swift investigation into the cause, and a fix was available within hours. CrowdStrike reported that operations for 99% of their customers were restored by the end of the same day. Importantly, however, other firms such as Delta Air Lines faced a prolonged outage from the very same event, costing over USD 500 million and resulting in 7,000 cancelled flights.39

- Prolonged outage.

Alternatively, a firm may experience a cyber incident and suffer considerable delay before it is able to restore all operations. For example, car manufacturer Jaguar Land Rover suffered a major cyberattack in the middle of 2025. After many months, it stated that it would restore partial operations in a ‘controlled, phased restart’ of some sections of its manufacturing facilities.40 As a result of the cyberattack, it reported losing GBP 50 million in lost production per week, and required a government loan of GBP 1.5 billion.41

Similarly, the cyberattack on the UK retailer Marks & Spencer in April 2025 disrupted many online and electronic services for 6 weeks, with some services unavailable for 15 weeks.42 Even after operations resumed, it continued to experience backlogs and delays in order fulfilment.43

- Limited interruption but distracted resources.

There is a final class of cyber incidents that may affect business operations only slightly but nevertheless distract the firm. These include fraud due to business email compromise, incidents of privacy violations, and even cases of data exfiltration and extortion. In these cases, there is little impact to business performance, though the firm may take weeks or months to resolve the issue.

The resilience-enhancing role of insurance

Cyber insurance has evolved from being a risk transfer mechanism to also helping companies manage and reduce cyber threats and their impacts. Insurers require baseline security standards from policyholders. They may also offer packages including security recommendations, cyber risk monitoring and alerts, and payment for the costs of experts should an incident occur.44 In doing so, insurance can help firms ‘shrink the V’ of the resilience triangle by improving their pre-incident, operational, and post-incident resilience (see Figure 6).

A complement to cybersecurity investment

Some firms may regard cyber insurance and cybersecurity as substitutes – a firm could upgrade its cybersecurity to reduce its cyber risk, or purchase insurance to absorb the cost of large claims. However, when well managed, cybersecurity investment and insurance can be complementary and mutually reinforce each other.

Insurance can encourage best-practice cyber hygiene, including regular software and hardware patching, with improved terms and conditions for policyholders that strengthen their cybersecurity. Through their risk assessment procedures, insurers might also guide a firm to allocate resources to more advanced or cost-effective cybersecurity measures.45,46 Likewise, experienced claims handlers can steer insureds to the best recovery solutions and help them efficiently respond to an event.

Unlike cybersecurity vendors, who might offer standalone warranties offering compensation should their specific product or service fail, cyber insurers have a vested interest in helping their policyholders minimise the full suite of losses from a cyber incident, including damages incurred by third parties. There is a feedback loop between the advice and guidance provided and coverage: prioritising more effective cybersecurity will reduce insurance claims.47 By the same token, if investing in cybersecurity enables an insurer to provide better coverage terms or more effective incident response support, the investment increases the value of cyber insurance.

Cyber insurance-as-a-service

In assessing the potential synergies between insurance and cybersecurity, cyber insurers have progressively added services such as advisory, legal, and crisis management, to their product offerings (see Box 5). While technology-led start-up companies (InsurTechs) are often associated with this evolution, traditional carriers now also typically combine proactive protection and incident response (IR) services together with financial safeguards.

Box 5: Strengthening cyber hygiene through insurance

The insurance industry has learned it must go beyond pure risk transfer to sustainably offer cyber coverage that boosts policyholders’ resilience. Modern cyber insurance typically provides ancillary cybersecurity services that guide businesses toward effective risk prevention and mitigation, in addition to covering crisis response.

Sharing threat intelligence

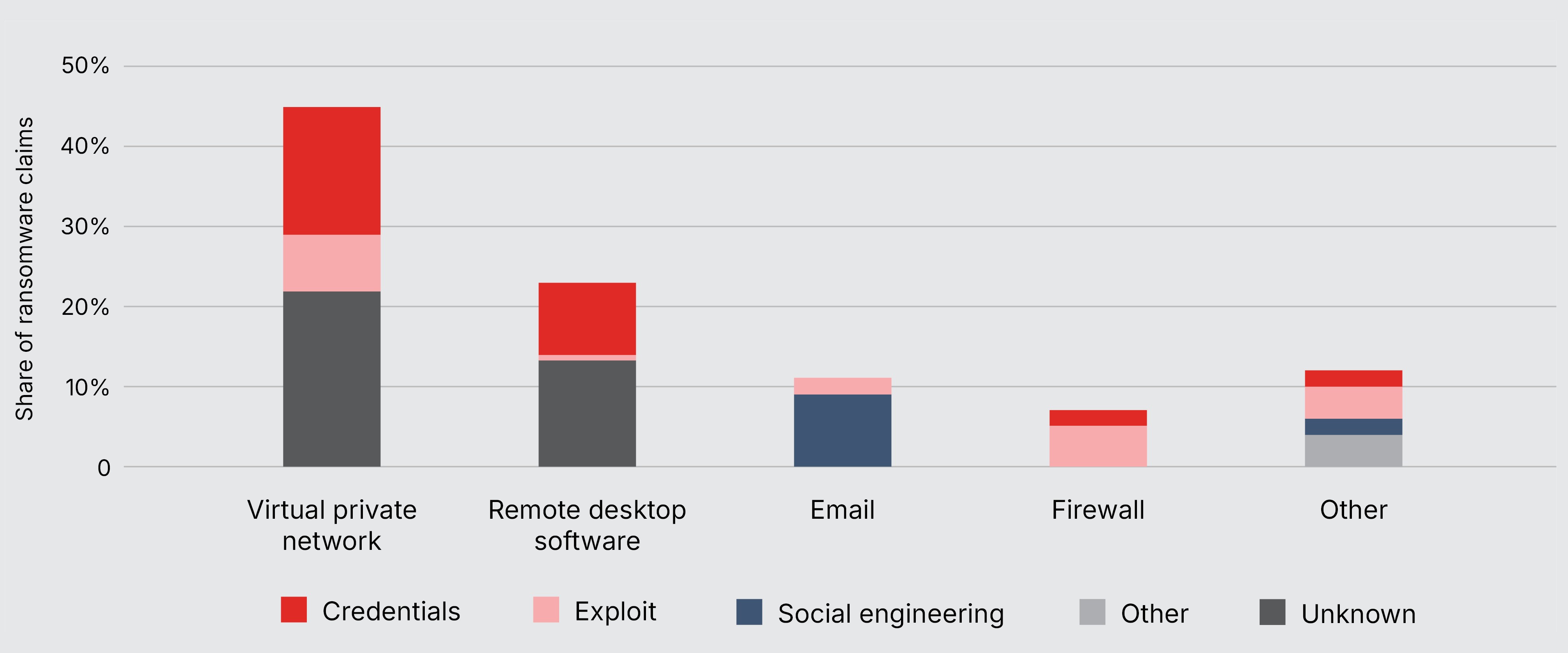

In most insurance lines, knowledge about effective loss controls accrues slowly as claims evidence accumulates.48 However, cyber insurers cannot wait for insights from actuarial analysis years after the loss, as attackers may have changed tactics in the meantime. Instead, insurers must monitor vulnerabilities in real time and notify customers about emerging attack vectors. For example, the majority of 2024 ransomware claims started via unauthorised access to either the victim’s virtual private network (VPN) (45%) or remote desktop protocol (RDP) systems (18%) (see Figure 8).49 If one of these services is not secure, insurers can proactively inform insureds.

FIGURE 8: KNOWN INITIAL ACCESS VECTORS FOR RANSOMWARE CLAIMS

Note: Initial access vectors are methods cybercriminals use to gain a foothold in a network, primarily involving stolen credentials, social engineering (e.g. phishing), and exploiting software vulnerabilities.

Source: Coalition

Coalition, for example, gathers threat intelligence to send out alerts about new software vulnerabilities that are under active exploitation. This includes operating a global honeypot network – decoy systems that lure cybercriminals and reveal new attack methods – to collect real-time intelligence on ransomware tactics. This telemetry allows early detection of new ransomware campaigns, often before their impact is made public.

Hands-on support

However, this kind of information is useless if the customer does not have the capacity to take remedial action. Small businesses often lack the resources and/or expertise to resolve cybersecurity issues. Many insurance carriers mitigate the impact of an ongoing attack by providing access to 24/7 helplines to triage a potential event (even before confirming a breach and initiating a claim). In addition, Coalition runs a dedicated security support centre to guide policyholders to fix issues before they turn into incidents.

Policyholder incentives

Insurers have progressively sought to better differentiate prospective insureds according to the strength of their cybersecurity posture. This includes meeting certain security criteria as a condition of coverage. Aligning incentives can also work by rewarding good cybersecurity behaviour. For instance, policyholders who engage with recommended risk reduction services may benefit from reduced loss retention levels or lower deductibles.50

Source: Sezaneh Seymour and Daniel Woods, Coalition

3.2.1 Pre-loss prevention

As part of their underwriting assessment, insurers may require their clients to undergo formal cyber penetration testing.51 This involves deploying cybersecurity specialists, who actively attempt to breach the security defences of a system, network, or application to uncover weaknesses that could be exploited in real-world attacks.52 Some carriers also work with bug bounty organisations to leverage the expertise of the broader ethical hacking community (see Box 6).

Box 6: Cybersecurity at SMEs: Leveraging bug bounty schemes

Cyber insurers increasingly emphasise protection services alongside loss indemnification to raise security awareness among their customers and encourage better security practices. One tool that some carriers are exploring is bug bounty programmes. These offer ethical hackers financial incentives to discover security vulnerabilities and weaknesses in a policyholder’s IT systems. For example, Helvetia has partnered with GObugfree, a Swiss expert in bug bounty programmes, to develop a simplified vulnerability testing version called the Community Bugtest. This one-time security check helps SMEs identify and close vulnerabilities before they can be exploited. The service is not part of the cyber policy; rather Helvetia acts as an intermediary to introduce its customers to GOBugfree.53

How does the Community Bugtest work?

While similar in nature to a traditional penetration test, the Community Bugtest differs in scope and depth. Specifically, it is limited to a fixed timeframe (two days) and offers a streamlined, high-level overview of the company’s security weaknesses. A penetration test, by contrast, typically examines a predefined scope in greater depth using a structured methodology. GObugfree’s employees simulate an external cyberattack, relying solely on publicly available information to gain access to the firm’s systems. Any resulting recommendations can then be prioritised and addressed by the company’s own IT team or with the support of a specialised security partner.

The Community Bugtest serves as an entry point for small firms to understand how they might benefit from a full-scale bug bounty programme where outside ethical hackers are rewarded for discovering individual vulnerabilities in systems or software. However, the Bugtest itself does not involve any bounty payments. Instead, a company pays a one-time fee for this service.

Insurance benefits

Companies that implement security recommendations from vendors such as GObugfree reduce the cyber risks they face and as a result can make themselves more insurable. This can lead to better terms and conditions on their cyber insurance, including more favourable pricing as well as possibly higher coverage sums. Customers who additionally opt for ongoing monitoring schemes like a full bug bounty programme may benefit from even more favourable insurance terms.

Source: René Buff, Helvetia

Penetration tests are usually performed at the inception of the cyber insurance policy or at the annual renewal and include scanning exercises that automatically check for known software and hardware vulnerabilities, lack of security controls, and common network misconfigurations. External scans assess publicly accessible systems to identify vulnerabilities in perimeter defences, like firewalls and exposed ports. Internal scans focus on weaknesses within a network's internal infrastructure, with vendors often using authorised access to detect unauthorised or unpatched software.54

Alongside periodic scanning, cyber insurers also offer proactive monitoring and risk assessment. Many insurers now own or partner with cybersecurity firms – including third-party vendors providing Security Operations Center as a Service (SOCaaS) services – to offer endpoint protection or multifactor authentication and other cyber risk prevention and mitigation services. Such services seek to screen the public internet, as well as the dark web, for information about potential threats and vulnerabilities that could impact their policyholders.

Other insurers go even further, using offensive tactics to gather threat intelligence and build up a dynamic picture of the attacks to which their policyholders may be vulnerable. This includes partnering with tech start-ups that aim to disrupt cybercriminals' activities. For example, DarkWebIQ and Hudson Rock help identify potentially compromised accounts sourced directly from threat actors on the dark web and offer remediation advice to vulnerable firms.55

In addition to technical cybersecurity improvements, preventive organisational measures are another means to increase cyber resilience. These include, but are not limited to, regular training to raise employee awareness, a robust backup strategy, the definition and enforcement of access and authorisation policies, and the implementation of a cyber incident response/business continuity plan.

3.2.2 Post-incident response

If a policyholder’s cybersecurity is compromised – whether the result of an accidental failure or malicious attack – insurers also arrange services to help businesses recover. These include forensic investigations to identify the cause and extent of a cyberattack to support remediation efforts, as well as legal, public relations, and communications support to manage the longer-term fallout of the cyber incident on a firm’s reputation.

Insurers typically provide policyholders with a panel of pre-approved incident response (IR) firms and cover the associated fees incurred by policyholders. The victim, or in many cases the firm’s legal adviser, will choose and contract with the specific IR firm.56 A key benefit of using an on-panel IR firm is that insurers can negotiate fixed upfront prices for IR services often below market rates. Insurers may still reimburse the fees of off-panel firms, but this will depend on the terms of the cyber insurance policy and usually must be agreed prior to the incident.57

Close cooperation between the insurance carrier and IR firms helps accelerate insurance payouts, which can be crucial in financing essential remedial and recovery work. Speedy claims handling relies on ensuring that the necessary forensic data and documentation are compiled and cross-checked against the terms of the policy. This can be aided by IR firms that are familiar with the insurer’s claims procedures and can quickly provide additional information for the loss adjustment process.

A coordinating mechanism for resilience

One firm’s cybersecurity depends not only on its own effort but also on the efforts of others in the same ecosystem (e.g. vendors and suppliers). In principle, insurance can function as a coordinating mechanism by fostering effective security investment that expressly considers the interdependence of cyber risks across firms.

Several academics have proposed approaches for an enhanced coordinating role for insurers, especially because they have visibility of multiple firms’ cybersecurity postures, including vulnerabilities arising from the use of third-party service providers. For example, one study demonstrated that provided insurers can effectively evaluate and monitor policyholders’ cybersecurity, they could design insurance contracts that incentivise security investments that take account of spillover effects across firms.58,59 Another study considers a service provider and shows that an insurer will insure all agents (the service provider and its customers) as long as it can appropriately incentivise the provider to improve its security.60

Such policy features remain theoretical and have yet to find a commercial application. Nonetheless, an insurer’s ability to leverage knowledge about interdependent cyber risks holds considerable promise to foster improved systemwide cyber resilience.61 Short of re-working contract design, some authors also highlight how insurers might use insights from systems modelling. These models can assess cybersecurity interdependencies across firms and promote good security governance through the auxiliary services embedded in cyber insurance (see Box 7).

Box 7: Systems modelling for cyber insurance

Many companies now outsource key elements of their IT ecosystem, such as storage of customer data or security monitoring, creating critical external security dependencies. This calls for greater appreciation of how shocks can propagate and their effects be amplified across firms, as well as the systemwide benefits of key risk mitigation mechanisms like insurance.

Systems thinking: Building a framework for modelling based on computer science

A useful starting point is the concept of a distributed system, which is formed of:

- Connected locations, such as the rooms where servers and databases reside, connected by network cables, offices, and storerooms.

- Resources, such as computers, people, and inventory, which reside at the system's location.

- Processes that execute using the available resources at their locations to deliver the system's intended services.

Seen through this lens, the security properties of the ecosystem can be framed as an interdependent network of individual locations, resources, and processes.62 Each firm – as owners of those digital assets – should decide its cybersecurity posture based on an understanding of how interconnections across firms will influence its chances of being affected by a cyber incident at another firm within the ecosystem. The more resilient the system, the better able it is to withstand cyber threats and keep operational capacity within agreed tolerances.63

Modelling these interactions is mathematically challenging and requires rigorous analysis.64 A well-constructed model of a system can nevertheless help identify security weaknesses and guide decision making around firms’ cyber resilience. In turn, it can inform insurers in underwriting cyber risks.

A systemwide resilience role for cyber insurance

By aggregating and disseminating information about threats and vulnerabilities across firms and shaping coverage to incentivise best-practice cyber hygiene, insurers can enhance systemwide cyber resilience. In this way, insurers can function as decentralised enforcers of good security governance, expressly taking into account that weak cybersecurity by some firms can impose negative externalities on others.65

Such a stewardship role for insurers is most obvious when they possess full information about threats and vulnerabilities and have the ability to steer policyholders’ appropriate investment in cybersecurity. In practice, insureds may have better knowledge of their internal risk posture than insurers and disclosure may be resisted. Cyber threats also change rapidly and dependencies and externalities shift, meaning that what is good practice today may be insufficient tomorrow.

Significant progress has been made in recent years in helping to understand the dynamic characteristics of the cyber risk ecosystem, but further work is required. For cyber insurance to fulfil its potential to contribute to overall cyber resilience, there needs to be common understanding of the processes that influence the frequency and severity of cyber losses, otherwise the market will always be inherently inefficient.66

Source: David Pym, University College London (UCL), and Henry Skeoch, Beazley

How effective is cyber insurance at improving cyber resilience?

High hopes have been placed on the ability of cyber insurers to enhance firms’ cyber resilience.67 Nevertheless, doubts persist about whether cyber insurance can fulfil that promise. This section reviews the available empirical evidence on how well cyber insurance supports cyber resilience, drawing on existing studies and market intelligence gathered from industry participants.

Insurers pay claims and influence insureds’ cybersecurity posture

Insurance broker Willis Towers Watson analysed 4,650 cyber claims in over 90 countries, finding that 92% of notifications of potentially covered losses fell within cyber insurance coverage.68 By comparison, while insurers paid out on more than 90% of claims on motor insurance in the UK, the acceptance rate was around 70% on home buildings and contents policies, and closer to 50% for some lines such as legal insurance.69

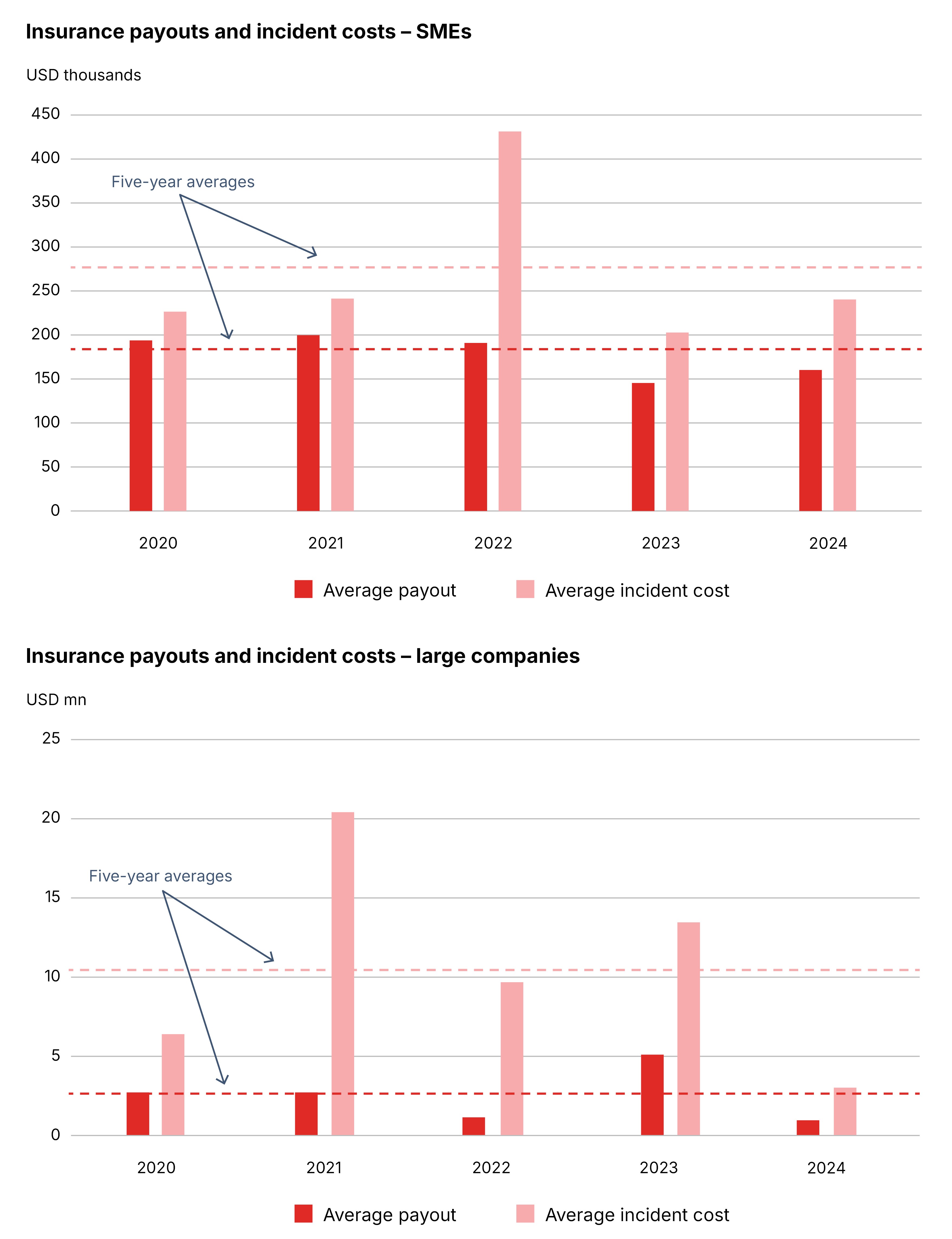

Data for the US, Canada and the UK also show that average cyber insurance payouts represent a material share of overall costs of an incident, close to 70% in the case of SMEs (see Figure 9).70 Across the industry, the majority of claims funds are spent paying for professionals to help respond to incidents.71 Crisis costs (including the costs to engage a privacy attorney to help navigate an incident and establish privilege, a digital forensics incident response firm (DFIR), and specialists to handle public relations, notification, and credit monitoring) average about 52% of expenses. Such services are crucial as publicly funded emergency services, such as the police, do not typically provide operational support to recover from cybercrime.

FIGURE 9: CYBER INSURANCE PAYOUTS AND INCIDENT COSTS

Source: NetDiligence

Surveys indicate that, through their underwriting procedures, cyber insurers have a positive impact on policyholders’ cyber hygiene. In particular:

- According to cybersecurity provider Delinea, cyber insurance requirements are driving heavy investment in cybersecurity tools. Around 96% of companies surveyed purchased at least one cybersecurity solution before being approved for coverage.72

- A 2024 survey by cybersecurity solutions company Sophos reported that nearly all organisations that purchased a cyber policy also invested in improving their cyber defences to optimise their insurance position. Over three quarters (76%) of surveyed companies made increased investments in cybersecurity in order to apply for cyber insurance.73

- A survey commissioned by InsurTech At-Bay showed cyber insurance helps encourage security measures, mitigation strategies, and targeted spending. More than 70% of respondents said they view cyber coverage as important or critical to their company and reported increased spending on cybersecurity solutions over the past 12 months.74

Case studies also highlight how cyber insurance improves policyholders’ cyber resilience (see Table 2). Likewise, past studies endorse the supportive role of cyber insurance in dealing with a cyber incident.75

TABLE 2: SELECTED CASE STUDIES OF SUCCESSFUL INSURER-LED UPGRADES IN FIRMS’ CYBERSECURITY POSTURE

Issue | Insurer-led solution | Outcome | |

| Improve insureds’ cyber risk preparedness |

|

|

|

|

|

| |

| Contain and recover from a major cyber incident |

|

|

|

|

|

| |

| Optimise insurance coverage |

|

|

|

|

|

| |

Source: Tom Egglestone, Resilience

Organisations that have cyber insurance say they appreciate how it aids their overall security posture. A Munich Re survey indicates the majority of policyholders welcome the provision of ancillary services from carriers and see them as integral to cyber insurance (see Figure 10). Similarly, a recent Howden poll indicates that firms with insurance policies that include such services believe they significantly improve their capabilities to cope with a cyber incident.76 As highlighted in Box 8, firms that deploy common security controls advocated by cyber insurers are much less likely to experience a breach.

FIGURE 10: cyber insurance survey indicates the majority of policyholders welcome the provision of ancillary services from CARRIERS (% RESPONDENTS)

Source: Munich Re

Box 8: Insurance promotes good cybersecurity

Cyber insurers play a vital role in identifying cybersecurity weaknesses and providing access to specialised expertise to address them. In the first instance, insurers may refuse to cover entities that demonstrate poor cyber hygiene. For example, Allianz declined insurance to a prospective client in the financial sector due to inadequate endpoint and network protection controls. Similarly, an airport client was not offered protection because its cybersecurity posture was deficient, including the absence of MFA for remote access, limited vendor management processes, and weak backup management.77

Beyond the initial screening, cyber insurers’ underwriting and risk prevention services provide actionable insights insureds can use to strengthen their cyber resilience. Cyber360 assessments, workshops, and risk scenario analyses, provide policyholders with enhanced transparency and control across their digital ecosystem. According to a recent study of security controls commonly used by cyber insurers when assessing risk, organisations that regularly test their cyber incident response plans are significantly less likely to face breach-related insurance claims.78

By developing and analysing tailored threat scenarios and emerging potential vulnerabilities, insurers help reduce their clients’ potential exposures through targeted mitigation strategies. For example, in March 2024, insurers notified policyholders about a particular Citrix software vulnerability along with advice about implementing the required patch, enabling their policyholders to mitigate the threat of a ransomware attack.79

Source: Rishi Baviskar, Allianz Commercial

Market realities may blunt its governance role

Despite encouraging signs that cyber insurance contributes positively to firms’ cyber resilience, several market features still restrict its potential to promote effective cybersecurity governance. These reflect factors affecting both the supply of and demand for coverage.

In some cases, companies buy cyber insurance simply because of contractual commitments with their customers or suppliers rather than a conscious decision to optimise their cybersecurity. Such contractual obligations often mandate vendors to purchase cyber insurance, specify incident response roles, and ensure timely breach notifications by affected firms. For example, contracts often include data protection and breach notification clauses aligned with insurance coverage requirements. Where those clauses do not exist, some companies may simply eschew cover.

4.2.1 Limits to risk differentiation

To underwrite and price cyber risks accurately, insurers must align discoverable risks and exposures with factors unique to each business. This includes details collected during the application process, as well as other factors, like individual cybersecurity controls deployed by the firm.80 While underwriting practices have advanced in recent years, insurers still struggle to precisely differentiate insureds by their level of cyber risk. As a result, insurance terms and conditions do not always provide sharp incentives for firms with weaker cybersecurity to improve their controls.81

To some extent, this situation stems from a lack of reliable data either because the underlying risks are rapidly evolving, or the information that insurers have about firm’s cybersecurity posture is insufficiently granular or is incomplete. For example, despite advances in technographic data capture, insurers may have limited insight into clients’ business continuity plans, cloud architecture, and intangible asset exposure.

Outside-in scanning tools offer additional information about a policyholder’s vulnerabilities, but they provide only a partial snapshot and must be combined with details about the firm’s internal IT infrastructure and configurations. Recent empirical research suggests insurers still largely base their risk selection on policyholders’ self-assessed cybersecurity questionnaires, even though automated security scores produced by external vendors may have more predictive power about future claims (see Box 9). Furthermore, the same study finds that insurers primarily manage their exposure by capping coverage rather than fine-tuning prices according to the riskiness of the insured.82

Box 9: How cyber insurers select and price risk: insights from an empirical analysis

Advances in data collection and analytics have substantially improved the tools available to evaluate a firm’s cybersecurity posture. Automated scanning tools, as well as techniques to detect, block or redirect malicious intrusions (e.g. honeypots and sinkholes), now routinely gather information on open ports, vulnerabilities, and malware infections.83 Specialist vendors translate these observations into cybersecurity scores which, although imperfect, have been shown to be empirically useful in predicting cyber incidents.

A central question is the extent to which cyber insurers use these tools in risk selection and pricing. If insurers can accurately identify firms’ risk characteristics and adjust premiums accordingly, they can mitigate adverse selection (where high-risk companies disproportionately seek coverage) and moral hazard (where insured firms face weaker incentives to maintain good cyber hygiene). Improved risk differentiation should, in turn, strengthen insureds’ incentives to invest in their own cybersecurity.

Selecting and screening prospective policyholders

A recent study examined a proprietary dataset combining US data on cyber insurance take-up, cyber incidents, and firm-level cybersecurity risk indicators from one of the largest insurance brokers.84 For contracts sold through the broker between 2019 and 2022, firms with higher cyber risk – measured either by past incidents or by external security vendor scores – were more likely to purchase cyber insurance. That result could reflect two effects: demand-side selection (riskier firms seek coverage) and/or supply-side screening (insurers selectively underwrite high-risk firms at higher premiums).

To investigate this issue further, the study deployed additional survey data from the broker. The surveys captured firms’ self-assessed cybersecurity posture, allowing the researchers to distinguish between firms that intended to apply for insurance and those that ultimately obtained coverage.85 Regression analyses – using as dependent variables the probability of applying for cyber insurance and the probability of obtaining coverage – indicated that:

- Firms intending to apply for insurance were generally more alert to their underlying cyber risk exposure, either because they experienced a cyber incident or their cybersecurity score declined.

- Most firm characteristics, including firm size and cybersecurity score, were not statistically significant predictors of being insured, suggesting limited screening by insurers based on these variables. In contrast, the survey-based score was a significant predictor, indicating insurers relied more heavily on self-reported assessments when screening applicants.

Alongside prior research highlighting how questionnaires often understate technical or infrastructural features that matter for accurate risk assessment, this empirical evidence suggests insurers still lean on imperfect survey metrics, even when more predictive indicators – such as external risk scores or incident histories – are available.86

Pricing and coverage of cyber risk

Additional regression results on the same dataset showed that while small firms with recent incidents received higher coverage limits, their cybersecurity scores did not meaningfully influence the premiums they paid. Instead, insurers appeared to manage exposure primarily by capping the amount of coverage – particularly for large firms – rather than by adjusting premiums to reflect changes in risk.

Combined with the previous finding that firms with higher risk are more likely to apply for cover, the regression analysis suggests that adverse selection may arise from insurers not fully incorporating certain risk factors into their screening and pricing decisions. Furthermore, capping coverage is consistent with insurer capacity constraints and the need to control aggregate exposure to potential catastrophic cyber losses, resulting in tighter policy limits for large clients.

Some caveats

As with any empirical study, we should exercise caution when generalising the findings. Insurers may not fully incorporate cybersecurity scores into underwriting procedures simply because these measures are typically accessible only to large carriers. In addition, the reliability of the scores takes time to establish, and retrospective adjustments after incidents reduce their usefulness for prospective underwriting.