Kai-Uwe Schanz, Director Financial Inclusion, Geneva Association

Suggested citation

Geneva Association. 2025.

Insurance as a Core Element of Financial Inclusion in Emerging Economies.

Author: Kai-Uwe Schanz. December.

6 min read

Author

Introduction

Financial inclusion has become a central pillar of sustainable economic development, particularly across emerging economies, where high levels of income volatility, widespread informal employment, and limited social protection systems leave households vulnerable to financial shocks. Despite global progress in expanding access to insurance, savings, credit, and digital payments, more than 1.3 billion adults worldwide remain excluded from formal financial services, with many more underserved. These gaps include insurance, where protection levels lag far behind needs, leaving societies exposed to health emergencies, natural disasters, crop failures, and economic disruption.

Financial inclusion as a driver of economic development

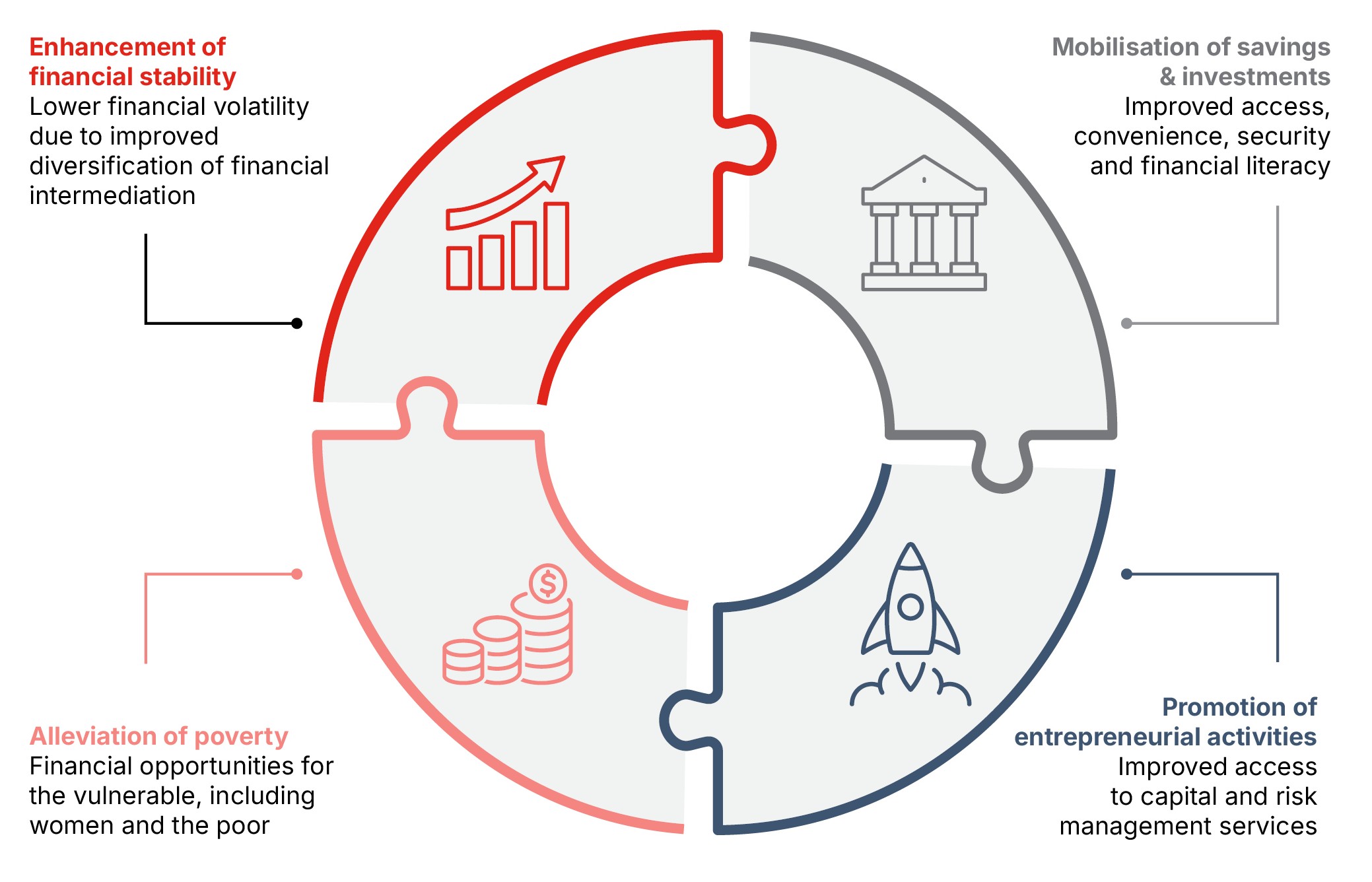

Evidence from cross-country studies shows that financial inclusion advances economic development through four mutually reinforcing pathways: mobilising savings and investments, enabling entrepreneurship, alleviating poverty, and improving financial stability.

Broad access to savings accounts fosters higher and more stable savings rates by providing safe, convenient mechanisms for storing funds. Empirical studies from developing countries show that formal savings channels not only encourage greater accumulation but also mobilise capital into productive investment, strengthening the financial sector’s ability to support economic growth.

Financial inclusion supports entrepreneurial activity at the micro, small, and medium enterprise levels. Access to both credit and insurance encourages business formation by lowering reliance on informal lenders and reducing vulnerability to shocks. Evidence from India, Sub-Saharan Africa, and other regions demonstrates how access to basic financial tools increases self-employment and small-business creation.

Financial inclusion also reduces poverty by enabling households to withstand income shocks, invest in education, and adopt more sustainable financial habits. Studies show strong links between financial inclusion and decreased poverty, particularly when women and other economically marginalised groups gain access to formal services.

Inclusive financial systems enhance macroeconomic and financial stability, too. Expanding access to deposits diversifies banks’ funding bases, while spreading credit across a wider population reduces concentration risk. Greater use of formal financial tools also supports economic formalisation, improves transparency, and reduces illicit financial flows. Women’s participation in formal financial systems plays an especially stabilising role due to their higher rates of saving and loan repayment.

The unique role of insurance

While payment services, savings, and credit have historically dominated financial inclusion agendas, insurance plays a unique role that cannot be substituted by other tools. Savings accumulate slowly and are often depleted during emergencies, while credit creates repayment obligations also at moments when households are least able to shoulder them. Insurance alone provides risk pooling and transfer, enabling households to withstand shocks such as health crises, accidents, and natural disasters without falling into poverty or liquidating essential assets.

Insurance also supports productivity-enhancing risktaking, such as investing in education or technology. By safeguarding the benefits of savings and credit, insurance strengthens the entire financial ecosystem and ensures that unexpected shocks do not erase developmental gains (see Table 1).

Insurance is not merely a financial product but an essential enabler of socioeconomic resilience. In emerging economies such as China and India, government-backed and public-private schemes,

notably in health and agricultural insurance, have expanded protection for hundreds of millions, reducing fiscal burdens and creating more stable foundations for growth.

TABLE 1: SAVINGS, CREDIT, AND INSURANCE – CHARACTERISTICS AND FUNCTIONS

Savings | Credit | Insurance | |

|---|---|---|---|

| Primary purpose | Accumulation of wealth for future consumption or investment | Access to funds for immediate consumption or investment needs | Protection against uncertain future events and financial losses |

| Risk management | Self-insurance - individuals rely on personal savings to buffer against shocks | Risk is with the borrower, who must repay regardless of circumstances | Risk sharing across a large pool, mitigating individual exposure |

| Information requirements | Low - financial institutions need basic information to manage deposits | Higher — lenders assess creditworthiness to mitigate default risk | High — insurers evaluate risk profiles to set premiums and coverage terms |

| Role in economic development | Provide an individual safety net and funds for investment | Enables entrepreneurial activities and consumption smoothing | Offers financial resilience against adverse events, encouraging and protecting investment and consumption |

Source: Geneva Association

Addressing evidence gaps: New and comparative survey-based data

To address persistent information gaps on insurance coverage and usage, the Geneva Association commissioned a survey across Brazil, China, India, Mexico, Morocco, South Africa, and Türkiye. With roughly 1,000 respondents per market, the survey provides insight into household risks, financial behaviour, familiarity with and usage of financial tools like insurance, as well as barriers to adoption.

Medical costs are the dominant worry in almost all countries surveyed, reflecting gaps in health coverage and high out-of-pocket spending. Concerns about premature death, disability, and insufficient retirement savings also appear prominently, signalling widespread awareness of lifecycle risks.

China, India, and South Africa display the highest familiarity with insurance, driven by digital super-app ecosystems, state-led financial inclusion programmes, and culturally embedded insurance traditions such as funeral policies, respectively.

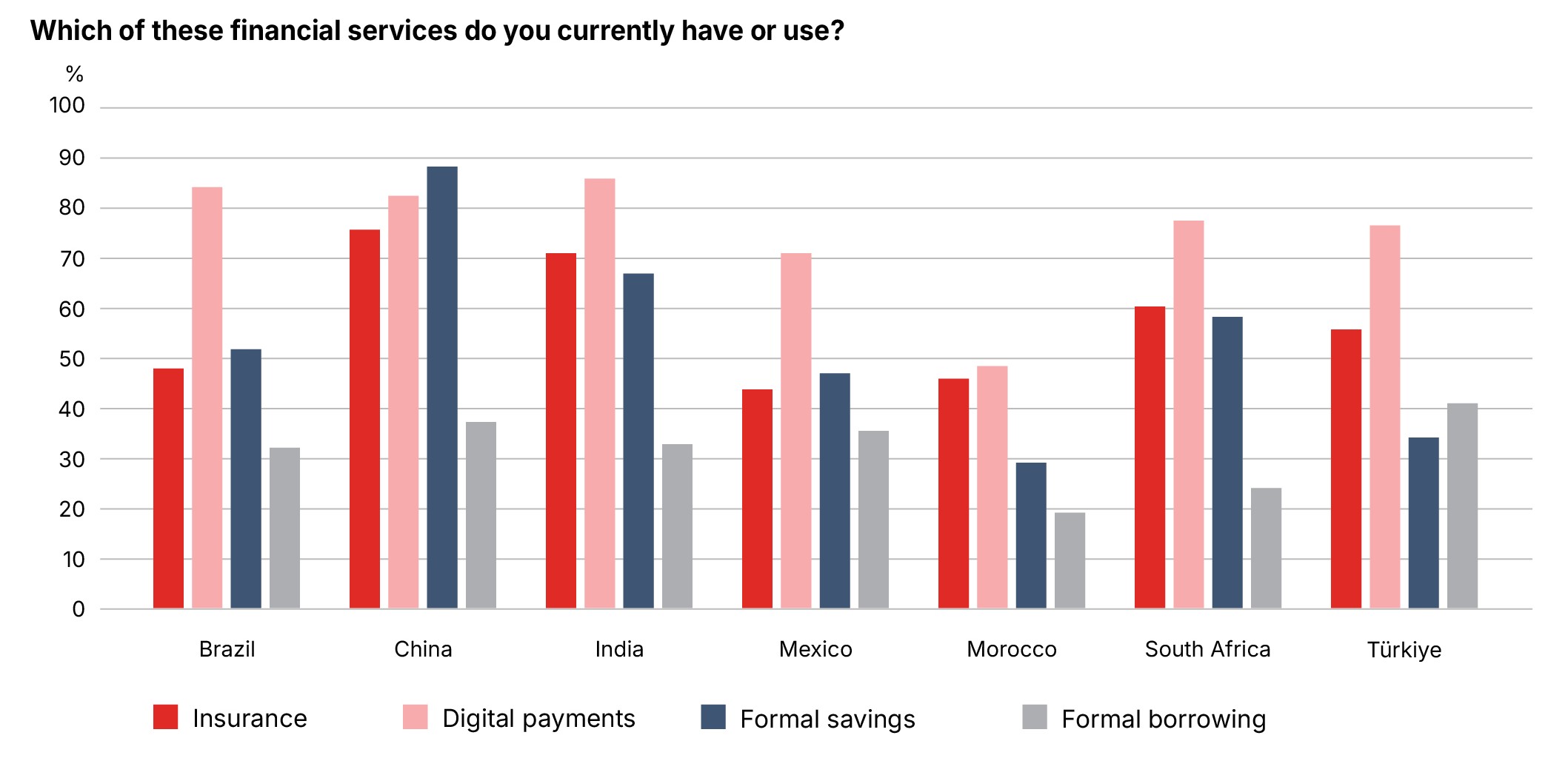

Digital payments are the most widely used financial service across all countries. China and India lead in insurance usage, with approximately three quarters of respondents holding at least one type of coverage. Borrowing is least used, reflecting structural barriers, lack of credit histories, and mistrust of lending channels (see Figure 1).

Insurance is considered useful by at least 70% of respondents in every market while borrowing is rated as least useful overall. Insurance is perceived as essential for asset protection and shock resilience, while savings dominate decisions related to major life events and long-term planning. Insurance plays a comparatively stronger role in India and China in major financial decisions, but a weaker role in Brazil, Mexico, Morocco, and Türkiye. Most uninsured respondents believe they could obtain coverage if they wanted it, suggesting that access is not the primary barrier; affordability and awareness remain more relevant constraints.

Health, term life, and motor insurance show high levels of awareness and adoption, largely driven by their intuitive relevance or mandatory nature. But disability, savingstype life products, and property insurance remain largely underutilised, indicating major protection gaps.

Affordability is the primary obstacle for health and life insurance. Knowledge gaps, especially regarding savings-type life insurance, also inhibit demand. Behavioural factors such as present bias, optimism bias and low prioritisation further limit uptake (see Figure 2).

FIGURE 1: USE OF FINANCIAL SERVICES

Source: Geneva Association customer survey, powered by Kantar

FIGURE 2: REASONS FOR NOT OWNING INSURANCE

Source: Geneva Association customer survey, powered by Kantar

We identify three interconnected pillars required to scale inclusive insurance sustainably: commercial innovation, public policy, and regulatory support.

Commercial success factors

Purpose-built products must be simple, understandable, accessible, valuable, and efficient. Simplicity reduces cognitive burdens; understandability fosters trust; accessibility leverages digital enrolment and mobile payments; value ensures meaningful coverage at affordable premiums; and efficiency is achieved through digital operations and automation. Parametric insurance represents an emerging product type well aligned with these principles.

Affinity partnerships with mobile operators, microfinance institutions, retailers, cooperatives, and digital platforms enable rapid, low-cost expansion. Embedded insurance (bundling coverage into transactions such as e-commerce, ride-hailing, or telecom services) reduces friction and boosts uptake. Hybrid models combining digital channels with local agents are particularly effective in low-literacy environments.

Customer trust hinges on transparent, timely claims processes, simple products, and culturally relevant offerings. Strong affinity distribution networks, such as cooperatives or community groups, help overcome scepticism and facilitate adoption.

AI, digital platforms, and alternative data sources enable granular risk assessment, fraud detection, automated underwriting, and faster claims. These tools reduce costs and improve affordability.

Public-policy success factors

Governments play a key enabling role by embedding insurance within national financial inclusion strategies, as seen in China, India, Morocco, and South Africa, for example. Fiscal support through premium subsidies, tax incentives, and co-funding mechanisms is essential for addressing affordability constraints, especially in health and agriculture. Public-demand creation requires insurance literacy programmes, inclusion in school curricula, and awareness campaigns. Mandatory schemes can broaden participation, though they must be carefully designed to manage affordability and moral-hazard risks. Digital public infrastructure such as digital ID, mobile payments, and interoperable data systems is crucial for low-cost scale.

Regulatory success factors

Regulation must strike a balance between prudential stability and room for innovation. Simplified licensing for microinsurers, digital onboarding rules, composite product allowances, and sandbox environments support experimentation while safeguarding consumers. Robust grievance mechanisms and customer-protection frameworks further enhance trust.

Conclusion

Insurance is a foundational but often overlooked component of financial inclusion. It uniquely protects households and businesses from catastrophic shocks, complements savings and credit, and supports longterm economic and social resilience. Emerging economies face vast insurance protection gaps, but they also have an opportunity to leapfrog traditional models through digital innovation, public-private partnerships, and regulatory flexibility. Achieving inclusive insurance at scale requires alignment between commercial viability, policy priorities, and regulatory enablers.

Foreword

In emerging economies, financial vulnerability is a daily reality for households and small businesses. Climate shocks, health emergencies, and income instability can erase years of progress in an instant. This report offers evidence on how inclusive insurance can strengthen the financial security of millions still at the margins of formal protection.

Our research shows that although access to digital payments, credit, savings and insurance has expanded, more than 1.3 billion adults remain excluded from formal financial services. Insurance plays a uniquely stabilising role: unlike savings, which is limited by liquidity needs, or credit, which can deepen indebtedness, insurance distributes risk and bolsters resilience at scale. Country experiences reinforce this. In India, technology-enabled, subsidised health, accident, and crop schemes have reached hundreds of millions, demonstrating the societal value of well-supported public programmes.

The Geneva Association conducted a customer survey across seven major emerging markets: Brazil, China, India, Mexico, Morocco, South Africa, Turkey. The findings reveal that while China, India, and South Africa show the strongest familiarity with insurance, across all countries at least 70% of respondents view insurance as useful. This is encouraging. Health costs dominate household concerns; yet major protection gaps remain – especially in property, disability, and savings-type life insurance – driven chiefly by knowledge and affordability barriers.

The report identifies three key levers for progress. Insurers must design simpler products to build trust and leverage digital technologies to reduce costs. Policymakers should embed insurance in national financial inclusion strategies, supported by digital public infrastructure and targeted subsidies. Regulators must balance innovation with consumer protection.

Looking ahead, closing protection gaps will require collective resolve to build financial and social resilience at scale.

Jad Ariss

Managing Director

Executive summary

Financial inclusion has become a cornerstone of sustainable development, particularly in emerging economies, where households remain highly vulnerable to financial shocks. Despite global advances in payment, savings, credit, and insurance services, more than 1.3 billion adults worldwide still lack access to formal financial systems. Many more remain underserved, including in insurance, resulting in vast protection gaps.

Research and country-level evidence point to four mutually reinforcing channels through which financial inclusion drives growth and resilience. First, it mobilises household savings and commercial investments by offering safe, convenient, and secure means for capital accumulation, boosting the productive deployment of funds. Second, it promotes entrepreneurship by supplying access to credit and insurance, lowering dependence on informal, high-cost lending and risk taking, and encouraging self-employment and small business expansion. Third, financial inclusion alleviates poverty by enabling households to smooth consumption, invest in human capital, and build resilience. Finally, it enhances financial stability by broadening banks’ deposit bases, diversifying loan portfolios, and incentivising economic formalisation. Particularly in digital ecosystems, financial inclusion also improves transparency, reduces illicit flows, and strengthens institutional trust.

Among financial tools, insurance plays a singular role by transferring risk away from households and strengthening collective resilience. Savings and credit are essential but limited: savings are constrained by liquidity pressures, while credit places repayment obligations on already vulnerable borrowers. Insurance, by contrast, pools risks across communities, ensuring that a financial shock to one household does not translate into ruin.

Case studies highlight this distinct function. In India, for example, government-led programmes have provided subsidised crop, health, accident, life, and pension insurance – albeit in small volumes – to hundreds of millions, reaching populations once excluded from formal protection.

Executive testimonies reinforce that insurance is more than a financial contract; it provides positive externalities for society, reducing fiscal strain on governments by expanding private-sector risk taking and sustaining socioeconomic gains over time.

Given the lack of comprehensive, internationally comparable data on insurance adoption in emerging economies, the Geneva Association commissioned a customer survey across Brazil, China, India, Mexico, Morocco, South Africa, and Türkiye. The survey provides fresh comparative insights:

- Medical costs dominate household anxieties, reflecting gaps in public health coverage and high out-of-pocket burdens.

- China, India, and South Africa demonstrate the strongest awareness of insurance, driven by digital ecosystems, public schemes, and cultural factors, respectively. China and India exhibit the highest levels of insurance penetration. In all markets, at least 70% of respondents consider insurance useful.

- Respondents value insurance for asset protection and risk mitigation, while savings dominate long-term planning and key financial decisions such as starting a family or buying a home.

- Most respondents who do not own insurance believe coverage would be available if they sought it, suggesting that access is not a primary constraint.

- Affordability remains the main barrier to purchasing health insurance in most countries. Knowledge gaps are most significant for savings-type life insurance.

- Health, life, and motor insurance are the most widely adopted; penetration of property, disability, and savings-type life insurance remains limited, suggesting major protection gaps in asset protection, income replacement, and retirement savings.

This report identifies key success factors in three areas for insurance inclusion in emerging economies, stressing the need for an integrated approach.

- Commercial: Viable inclusive insurance products must be simple, understandable, accessible, valuable, and efficient (the SUAVE framework). Distribution requires innovation – partnerships with telecoms, microfinance, retailers, and community networks, for example, are critical, as are embedded models that bundle insurance with existing transactions. Trust is paramount, hinging on transparent claims processes and culturally relevant products. Digital technologies, AI, and alternative data (e.g. related to e-commerce transactions) allow more granular risk assessment, personalised pricing, and scalable operations, reducing costs and fraud.

- Public policy: Embedding insurance within national financial inclusion strategies is central and more feasible than ever, given significant progress in digital payments and digital public infrastructure. China, India, Morocco, and South Africa, for instance, explicitly position insurance as a policy pillar. Fiscal support, such as India’s health and accident insurance or China’s crop insurance subsidies addresses affordability issues. Public demand creation requires literacy programmes, school curricula, awareness campaigns, and trust-enhancing customer protection frameworks. Digital public infrastructure, including IDs and payment systems, is essential to scaling low-cost delivery by private insurers.

- Regulatory: Insurance regulation must balance prudential soundness with flexibility to allow innovation. Simplified licensing, digital onboarding, composite products, and innovation sandboxes enable private-sector experimentation. Customer protection frameworks and ombudsman services reinforce trust.

The interplay of these three domains through a wide range of public-private collaboration determines scalability. Inclusive insurance only thrives when commercial innovation aligns with policy priorities (e.g. climate resilience and food security) and regulatory flexibility.

Introduction

Income instability arising from financial shocks, coupled with pronounced income inequality, are significant barriers to sustainable, long-term economic development. This challenge is particularly acute in countries that have a high dependence on agriculture, are vulnerable to natural disasters, and lack formal coping mechanisms.1 Financial inclusion, through formal payment, savings, credit, and insurance services, is widely viewed as an important enabler of economic growth and stability in emerging markets.2,3,4 Over the past decade, numerous global and national initiatives have aimed to expand access to financial services in emerging economies, by harnessing digital technologies, for example.5 Despite these efforts, approximately 1.3 billion adults worldwide remain excluded from the formal financial system.6 Many more continue to be underserved, notably in insurance, resulting in massive and disproportionately large protection gaps across emerging economies. In 2023, those countries represented over 60% of global protection gaps,7 accounting for less than 20% of global life, health, and property & casualty insurance premiums.8

While payment, savings, and credit services have traditionally dominated the financial inclusion agenda, inclusive insurance plays a critical role, too, by mitigating and absorbing risks that hinder or jeopardise social and economic progress. In this report, inclusive insurance describes approaches that narrow the difference between the average level of insurance coverage across the entire population and the level of coverage among specific demographic groups that may not be participating in or be underserved by insurance markets. These groups may include the young, the elderly, low-income earners, and the chronically ill.9

Inclusive insurance protects vulnerable households and businesses from shocks such as illness, natural disasters, or economic disruption, enabling them to avoid financial ruin, maintain consumption, and restore key productive assets. It also encourages entrepreneurship at the micro, small, and medium enterprise levels, enabling calculated risk taking. By complementing and protecting savings and credit as coping mechanisms, insurance inclusion strengthens financial resilience, promotes upward mobility, and contributes significantly to sustainable development in emerging economies.10

Inclusive insurance strengthens financial resilience, promotes upward mobility, and contributes significantly to sustainable development in emerging economies.

Internationally comparable data on the ownership and use of financial services in emerging economies remains limited. While resources such as the World Bank’s Global Findex Database provides about 300 indicators related to account ownership, payments, savings, credit, financial resilience, and mobile and smart phone ownership, comprehensive, standardised, and country-specific data on insurance adoption and usage is not available.11 The most relevant reference to insurance is that 23% of adults across the 141 surveyed lowand middle-income economies make payments to an insurer. If China were excluded, this would fall to 11%.

The IMF’s Financial Access Survey (FAS) offers the most extensive supply-side database on financial access and usage, covering 192 economies and tracking financial services through 121 reported and 70 estimated indicators.12 The dataset, which spans two decades (2004–2023), enables global comparisons and policy benchmarking. Despite its broad scope, the FAS includes only a limited set of indicators related to insurance, such as the number of policyholders. The data is also only available for select countries and years.

Panda et al. provide one of the few comparative empirical studies based on a dataset from 15 developing countries, covering almost 66,000 households.13 The data originates from the FinScope Consumer Survey conducted between 2011 and 2018 as part of the Making Access Possible (MAP) programme. The survey found that the use of formal savings mechanisms in developing countries remains low, with only 14% of adults saving through banks. Ten percent of respondents save through non-bank financial institutions, such as microfinance institutions. The use of credit is even more limited, with only 6% of respondents borrowing from

banks. Non-bank financial institutions provide credit to 7% of surveyed households. Insurance penetration also remains low, with only 16% of surveyed adults having any form of formal coverage. Funeral insurance is the most common product, followed by life insurance and medical insurance. Crop and property insurance remain largely underutilised.14

These gaps in granular, harmonised data on the use of financial services in emerging economies, particularly insurance, make it challenging to accurately assess financial inclusion and formulate effective commercial strategies and policy interventions. This report aims to help fill the gap and complements a previous Geneva Association report on inclusive insurance in advanced economies.15 It will:

- Discuss the critical role of insurance in financial inclusion. In light of the significant vulnerabilities faced by households in emerging economies, the report examines how insurance uniquely contributes to financial inclusion. The analysis, significantly enriched by approximately 30 interviews with insurance executives and experts from around the world, underscores how insurance not only mitigates risks associated with financial shocks but also complements and facilitates other financial services in reinforcing economic stability and promoting resilience, at both the micro (i.e. household) and macro (i.e. country) levels.

- Provide original, comparative, survey-based data on insurance, savings, and credit. The findings add colour about access to affordable and relevant insurance products across seven major emerging economies, based on an online survey of households. This data facilitates a nuanced understanding of the relative importance and interplay of insurance, savings, and credit services.

- Identify and explore key commercial, public policy, and regulatory success factors. Recognising that both market dynamics and policy environments are critical to the effectiveness of financial inclusion strategies, the report identifies levers that have successfully promoted insurance-based financial inclusion.

- Formulate practical recommendations for insurers, policymakers, and regulators.

“In emerging markets, insurance plays a unique and critical role in promoting financial inclusion. It provides essential risk coverage to populations often excluded or underserved by the formal financial system, offering protection that strengthens resilience, supports equity, and fosters social cohesion. Insurance allows individuals and families to manage risk more efficiently and affordably than saving large sums to cover unexpected events. For example, accumulating USD 1,000 for an emergency can take considerable time and effort, whereas an insurance policy covering that risk is a more accessible and cost-effective alternative. As such, insurance complements savings and investment management strategies at a significantly lower cost.

Emerging regions urgently need stronger insurance activity to support economic and social development. In Latin America, where insurance penetration remains low, closing the insurance gap would raise per capita income, improve savings rates, and benefit lowerand

middle-income groups. The estimated insurance gap in the region exceeds USD 300 billion. Premiums represent just 2.8% of the global total, despite the region accounting for over 7% of the world’s GDP.

Addressing this shortfall requires coordinated public-private action. Raising insurance and financial literacy is essential, as is the need for more flexible, tailored products that match people’s real economic conditions. Technology offers vital tools to expand coverage, particularly via mobile phones, which are more widespread than computers or bank accounts. Reaching underserved populations with simple, personalised solutions is critical. Insurance, properly designed, priced and delivered, can drive socioeconomic development, reduce vulnerability, and ensure broader, more inclusive prosperity.”

Antonio Huertas

Chairman & CEO, MAPFRE

“Unlike credit and savings, insurance offers financial protection against unforeseen adverse events without requiring immediate repayment or prior accumulation of funds. For example, crop insurance schemes or health programmes such as the Pradhan Mantri Jan Arogya Yojana, the world’s largest health scheme in India, provide essential coverage to millions of vulnerable individuals. This risk transfer mechanism addresses vulnerability and exclusion by allowing those with minimal assets or irregular incomes to avoid poverty traps caused by unexpected shocks such as illness, crop failure, or natural disasters.

Similar schemes exist in Thailand, including government-supported microinsurance, co-operative loan protection, and crop and weather insurance programmes run jointly with public banks and non-bank financial institutions. These initiatives help informal workers and small farmers maintain financial stability and protect their livelihoods. They demonstrate that insurance acts as a stabiliser for households and communities, complementing credit and savings systems by reducing the long-term financial risks

associated with unpredictable events. Insurance also enables lowand middle-income populations to move up the economic ladder and offers a scalable, cost-effective mechanism to supplement public welfare schemes, thereby supporting inclusive and sustainable economic growth.

Digitalisation enhances the reach and effectiveness of insurance. It lowers operational costs and allows for scalability, while data analytics enable insurers to understand the unique risks faced by different populations and offer affordable cover tailored to local needs. Further, technology and data analytics enhance access to insurance for underserved populations by improving awareness through targeted digital education and improving service via mobile platforms and social media. For instance, digital inclusion in India has enabled approximately 1 billion internet users and 18 billion digital transactions every month, making the distribution of insurance extremely scalable and cost effective.”

Markus Riess

CEO, ERGO

“Insurance is more than a financial product. It’s a mechanism for mutual support that builds resilience, reduces poverty, and enables economic growth. At Sura, we see its role as not just protecting individuals but catalysing national development. When people are insured, governments face less fiscal strain and entrepreneurs can take productive risks. But to truly scale inclusive insurance, we must simplify products, use data wisely, and promote risk literacy. Technology is an enabler, helping us reach underserved populations through digital channels and AI. However, we also need regulatory flexibility and public-private collaboration to make protection accessible and sustainable. Insurance must be recognised as essential infrastructure for inclusive progress, especially in vulnerable communities.”

Juana Francisca Llano Cadavid

CEO, Suramericana

“Insurance in emerging markets is ultimately about people who live just one risk away from poverty. Making it accessible requires collaboration between industry, policymakers, and regulators. We must create simple, affordable, technology-driven solutions, such as embedded insurance, digital onboarding, and mobile-first claims. These are not just innovations but tools for trust and inclusion. Technology alone is not enough. Public policy must raise awareness, offer the right incentives, and promote insurance literacy, especially in rural and low-income areas. Distribution must evolve through bancassurance, digital platforms, and community networks. Regulators should support flexible, customer-focused innovation. When we act with empathy and shared purpose, we do more than close protection gaps; we bring dignity, resilience, and financial strength to those who need it most.”

Tapan Singhel

CEO, Bajaj General Insurance

Financial inclusion as a driver of economic development

Through savings mobilisation, entrepreneurship, poverty reduction, and greater system-wide stability, financial inclusion creates a reinforcing ecosystem that drives resilient, inclusive, and sustainable economic development.

Theoretical frameworks, case studies, and cross-country evidence highlight how financial inclusion enhances economic outcomes through mutually reinforcing mechanisms.16 It facilitates the mobilisation of household savings and commercial investments, channeling more funds into productive use. It promotes entrepreneurship at the micro, small, and medium levels by providing access to credit and insurance, for example, enabling business growth. Financial inclusion also alleviates poverty by providing low-income individuals and households with access to credit, savings, and insurance, helping to maintain consumption after financial shocks and investment in education, and build financial resilience against economic shocks. Finally, it enhances financial stability by broadening financial participation and reducing reliance on informal credit. This section explores these four closely intertwined dimensions in greater depth (see Figure 1).

Mobilisation of savings and investments

A substantial body of research has investigated the effects of financial inclusion on savings behaviour and capital formation within developing and emerging economies. For instance, Ansar et al. found that enhanced financial inclusion led to increased savings rates among individuals, thereby contributing to greater capital accumulation.17 According to Allen et al., ownership of formal financial accounts (such as bank or mobile money accounts) significantly encourages individuals to save, especially in emerging economies, primarily by improving access and convenience and offering a higher level of security compared to informal savings methods.18 Their findings suggest that reducing barriers to account ownership can increase both the number of savers and the frequency of saving through formal accounts.19 Bhalli shows that increased savings in emerging economies through formal channels bolsters the mobilisation and efficient deployment of capital through commercial investments.20 These findings underscore the role of financial inclusion in strengthening savings and investment channels in emerging economies, thereby facilitating economic growth.

Promotion of entrepreneurial activities

Another key dimension of financial inclusion is its positive impact on entrepreneurial activity, especially in emerging economies and in the context of micro, small, and mid-sized businesses. Empirical evidence suggests that improved access to financial services significantly enhances the likelihood of individuals engaging in entrepreneurial ventures, typically starting with self-employment and gig work. Financial inclusion, by broadening access to savings, credit, insurance, and payment systems, empowers individuals, especially those in underserved communities, to establish and expand businesses on the back of improved access to capital and risk management

services. This, in turn, contributes to job creation and overall economic development. Burgess and Pande provide early evidence from India showing how rural bank expansion stimulates entrepreneurship.21 The provision of affordable formal financial services by rural banks has significantly mitigated dependence on high-cost informal lending sources. A more recent study covering six Sub-Saharan African countries finds that access to and use of formal financial services, including banking and mobile money, significantly increase the likelihood of individuals starting businesses.22

Poverty alleviation

Financial inclusion helps alleviate poverty by creating and expanding financial opportunities for individuals who previously had no access to such services, especially women and the poor. This enables investment in productive endeavours, including education, thereby enhancing economic opportunities and reducing poverty levels.23

Saha and Qin further underscore the significance of financial inclusion in poverty reduction.24 Their comprehensive analysis examining 156 countries from 2004–2019 finds that financial inclusion through banking services substantially reduces poverty rates across various income groups, with a particularly strong effect on extreme poverty. The study also highlights that addressing gender inequality through financial inclusion efforts contributes to more effective poverty alleviation.

Enhancement of financial stability

Financial inclusion influences financial stability, especially in emerging economies. It can enhance macro stability by diversifying banks’ funding sources and loan portfolios. Broadening access to deposit services, particularly among low-income savers, provides banks with stable, low-cost funding, thereby reducing individual bank risks. Additionally, distributing loans across a wider base of small borrowers can lower the concentration of credit risk, mitigating systemic vulnerabilities.25 In particular, women’s participation in the financial ecosystem plays a crucial role in enhancing financial stability. They are more likely to save, repay loans on time, and invest in long-term well-being, helping to diversify risks, increase deposit bases, and expand economic activity. Despite these benefits, women remain underserved due to barriers like limited access to credit and tailored financial products.26

Financial inclusion also contributes to financial stability through the formalisation of economic activity in emerging economies. By expanding access to formal financial services, informal workers and enterprises are incentivised to integrate into the formal economy, thereby improving tax compliance, regulatory oversight, and overall economic stability. Moreover, the adoption of digital financial services, such as mobile money and electronic payments, fosters transparency in financial transactions, reducing opportunities for illicit economic activities and strengthening institutional trust.27

FIGURE 1: THE ECONOMIC CASE FOR FINANCIAL INCLUSION

Source: Geneva Association

The unique role of insurance in financial inclusion

“Insurance is not merely a safety net after loss; it is the essential catalyst that enables investment, economic growth, and sustainable development, especially in emerging markets. Insurance uniquely mitigates risk, empowering individuals and businesses to pursue opportunities otherwise out of reach. Achieving true financial inclusion demands early, integrated partnerships across sectors, commercial viability at the core of business strategy, and a proactive role in prevention, knowledge transfer, and policy alignment.”

Mirko Sartori, Generali

Households and small businesses in emerging countries face numerous risks, including illness, crop failure, and natural disasters. Their coping strategies vary based on socioeconomic and cultural factors.28 Access to formal financial services is essential not only for economic growth and development but also for effective risk management at the micro level, enabling households to better prepare for and recover from economic shocks.29

Traditional discussions predominantly emphasise payment services, savings, and credit as key tools for financial inclusion. Savings enable individuals to set aside resources for future use, often as a form of self-insurance against risks like income fluctuations. They function as a financial instrument, where individuals rely solely on their own accumulated resources to buffer against shocks. However, the effectiveness of savings is often constrained by immediate liquidity needs and behavioural factors such as impatience or lack of financial discipline.30

Access to formal savings accounts provides a secure and structured mechanism for managing money, reducing vulnerability, and fostering long-term planning. In India, for example, the government-led Pradhan Mantri Jan Dhan Yojana (PMJDY) initiative has brought over 550 million people (as of March 2025) into the formal banking system by offering zero-balance savings accounts (requiring no minimum balance), which has helped improve household financial behaviour and resilience.31

Credit plays a crucial role in financial inclusion by providing liquidity to individuals and businesses. It allows them to borrow against future income or collateral, facilitating investment and consumption smoothing. Credit requires a contractual agreement between a lender and borrower, with repayment obligations.32 Examples are microloans in India, which help mitigate seasonal income volatility,33 and mobile credit platforms like M-Shwari in Kenya, which provide quick access to loans, helping individuals navigate short-term liquidity constraints.34

However, access to credit is frequently restricted due to information asymmetries, as lenders assess creditworthiness to mitigate default risk.35 This challenge is particularly severe in low-income countries, where a lack of collateral and frequent absence of insurance coverage limit borrowing opportunities. Despite these barriers, innovative credit products like microloans and mobile loans help expand access and build financial resilience.36

Insurance, by contrast, provides a unique risk-sharing mechanism, where individuals, households, or businesses pool risks with others. Unlike savings and credit, which focus on accumulating wealth or facilitating consumption and investment, insurance primarily serves to distribute risks across a larger collective, offering financial protection against risks such as illness, natural disasters, or economic shocks.37 As such, it enhances financial resilience, allowing people to cost-efficiently manage risk without resorting to precautionary savings ex ante and distress-financing strategies ex post, such as depleting savings, borrowing at high interest rates or selling productive assets (see Table 1).38 Also, by removing the risk of financial ruin, insurance uniquely enables households and businesses to take on productive risks like investing in a business or education, which is limited by sole reliance on savings or credit. In addition, insurance helps sustain and safeguard the macroeconomic benefits derived from savings and credit,39 ensuring, for example, that savings don’t vanish after unexpected shocks and that credit systems (e.g. mortgage markets) remain healthy.

In conclusion, insurance serves a fundamentally different function from savings and credit by offering risk protection rather than capital accumulation or access to borrowing. Insurance not only prevents setbacks into poverty40 but supports more confident risk-taking and strengthens and protects the impact of other financial tools by providing a critical safety net.

“Inclusive insurance must be better understood as a cornerstone of financial resilience, not a secondary or sequential add-on. It strengthens the value created by credit, savings, and payments by acting as a safety net and an accelerator. Insurance is the only financial service fully dedicated to managing shocks that pull vulnerable populations into poverty. To scale its impact, we need stronger narratives to enable better understanding; deeper integration into policy agendas to ensure dialogue among regulators beyond those responsible for financial services – telecoms/ digital, health, agriculture, education to name a few; and transformative models enabled by composite licensing, true bundling, behavioural credit-rating, omnichannel distribution etc. And, of course, end-consumer insight, insight, insight to drive innovation. And then scale. A virtuous cycle.

Garance Wattez-Richard, AXA EssentiALL

“Insurance does not merely safeguard against risk. It is also a pivotal enabler of resilience and upward mobility, particularly in emerging markets for economically vulnerable populations. Unlike credit or savings, insurance offers a financial buffer that empowers individuals to take calculated risks, such as investing in businesses or education. Its success in fostering inclusion hinges on supportive public policy and innovative technology. Together, these elements transform insurance from a reactive tool into a proactive instrument of economic empowerment and long-term financial stability.”

Amita Chaudhury, AIA Group

TABLE 1: SAVINGS, CREDIT, AND INSURANCE – CHARACTERISTICS AND FUNCTIONS

| Savings | Credit | Insurance | |

|---|---|---|---|

| Primary purpose | Accumulation of wealth for future consumption or investment | Access to funds for immediate consumption or investment needs | Protection against uncertain future events and financial losses |

| Risk management | Self-insurance - individuals rely on personal savings to buffer against shocks | Risk is with the borrower, who must repay regardless of circumstances | Risk sharing across a large pool, mitigating individual exposure |

| Information requirements | Low - financial institutions need basic information to manage deposits | Higher — lenders assess creditworthiness to mitigate default risk | High —insurers evaluate risk profiles to set premiums and coverage terms |

| Role in economic development | Provide an individual safety net and funds for investment | Enables entrepreneurial activities and consumption smoothing | Offers financial resilience against adverse events, encouraging and protecting investment and consumption |

Source: Geneva Association

Addressing evidence gaps: New and comparative survey-based data

Considering the scarcity of comprehensive and internationally comparable data on the role of insurance in financial inclusion in emerging economies, the Geneva Association commissioned a global customer survey to add more colour on the state of financial and insurance inclusion. Conducted in Q2 2025, it spans seven major emerging economies – Brazil, China, India, Mexico, Morocco, South Africa, and Türkiye – capturing insights from about 1,000 nationally representative respondents per country (aged 18–65).41

The questionnaire was structured around the following four key thematic pillars:

- Financial concerns. Respondents were asked to identify their most pressing financial concerns (e.g. medical costs, income loss, retirement savings), highlighting their perceived financial vulnerabilities.

- Familiarity, use, and perceived usefulness of core financial tools, i.e. insurance, digital payments, savings, and borrowing.

- Attitudinal and situational drivers. Respondents were asked how they perceive financial products as solutions to real-life challenges and goals, such as managing financial shocks, protecting assets, supporting major decisions, and ensuring long-term security.

- Insurance access, awareness, and usage. The survey explored 11 insurance types, from health and life to agricultural and mobile device insurance. It also investigated reasons for non-ownership, including affordability, access barriers, relevance, and personal priorities.

It is important to note that online customer surveys in emerging markets tend to be biased toward higher-income and higher-education (urban) respondents due to disparities in digital access and literacy levels. Individuals from wealthier and more educated backgrounds are more likely to have reliable internet access, own digital devices, and possess the technological skills needed to participate in online surveys.

Personal risk perceptions

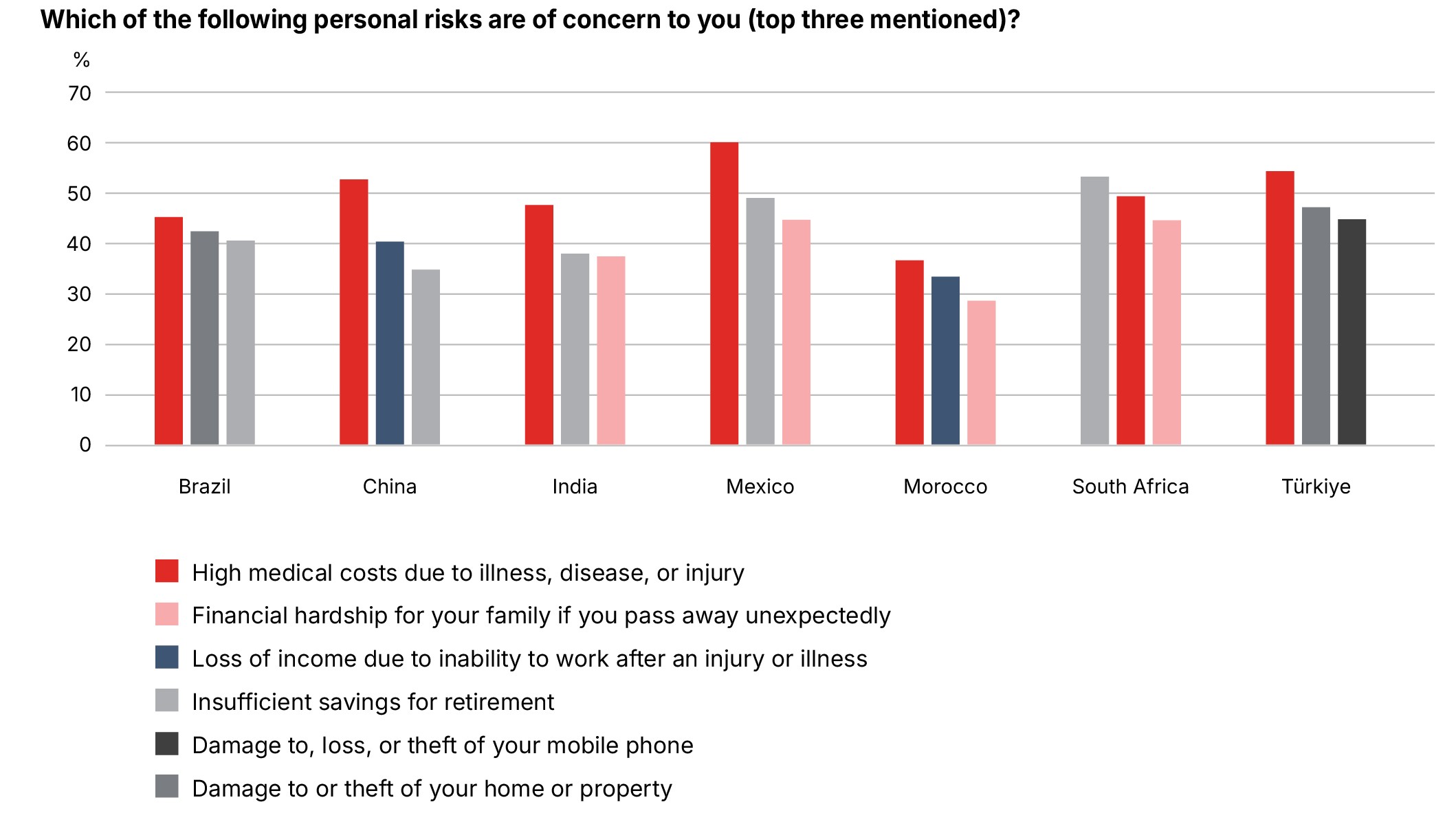

The survey asked respondents to identify their top personal financial risks and concerns. The results show that medical costs are the primary concern across all countries, except for South Africa. Premature death, disability, and retirement risks are widely cited, too, except in Brazil and Türkiye. Longevity risk (outliving one’s savings) is most salient in South Africa and Mexico (see Figure 2).

The domination of medical expenses as the top risk perception in most countries reflects the inadequate reach of public health systems and, in many cases, the limited affordability of comprehensive health insurance. In countries like India, Mexico, and Morocco, where out-of-pocket expenditure is high, concerns over catastrophic health costs are especially acute. Globally, in lower-middle-income countries, a group that includes India and Morocco, out-of-pocket health expenditure accounts for more than 40% of total health spending, making it the largest single source of healthcare

funding. In upper-middle-income countries, which include all other countries in the survey, out-of-pocket spending represents about 35% of total health expenditure, roughly equal to the share financed through government transfers.42

The strong recognition of life-related risks, such as premature death, disability, and underfunded retirement, in most emerging economies covered by the survey points to growing awareness of the need for financial

protection. Social security systems often provide very limited coverage, especially for informal workers. Private insurance solutions remain underdeveloped or inaccessible for many due to affordability and low financial literacy (see section 4.8). South Africans’ concern with longevity may stem from the absence of a mandatory, contributions-based pension system (second pillar).43

FIGURE 2: TOP PERSONAL RISKS

Source: Geneva Association customer survey, powered by Kantar

Familiarity with financial services

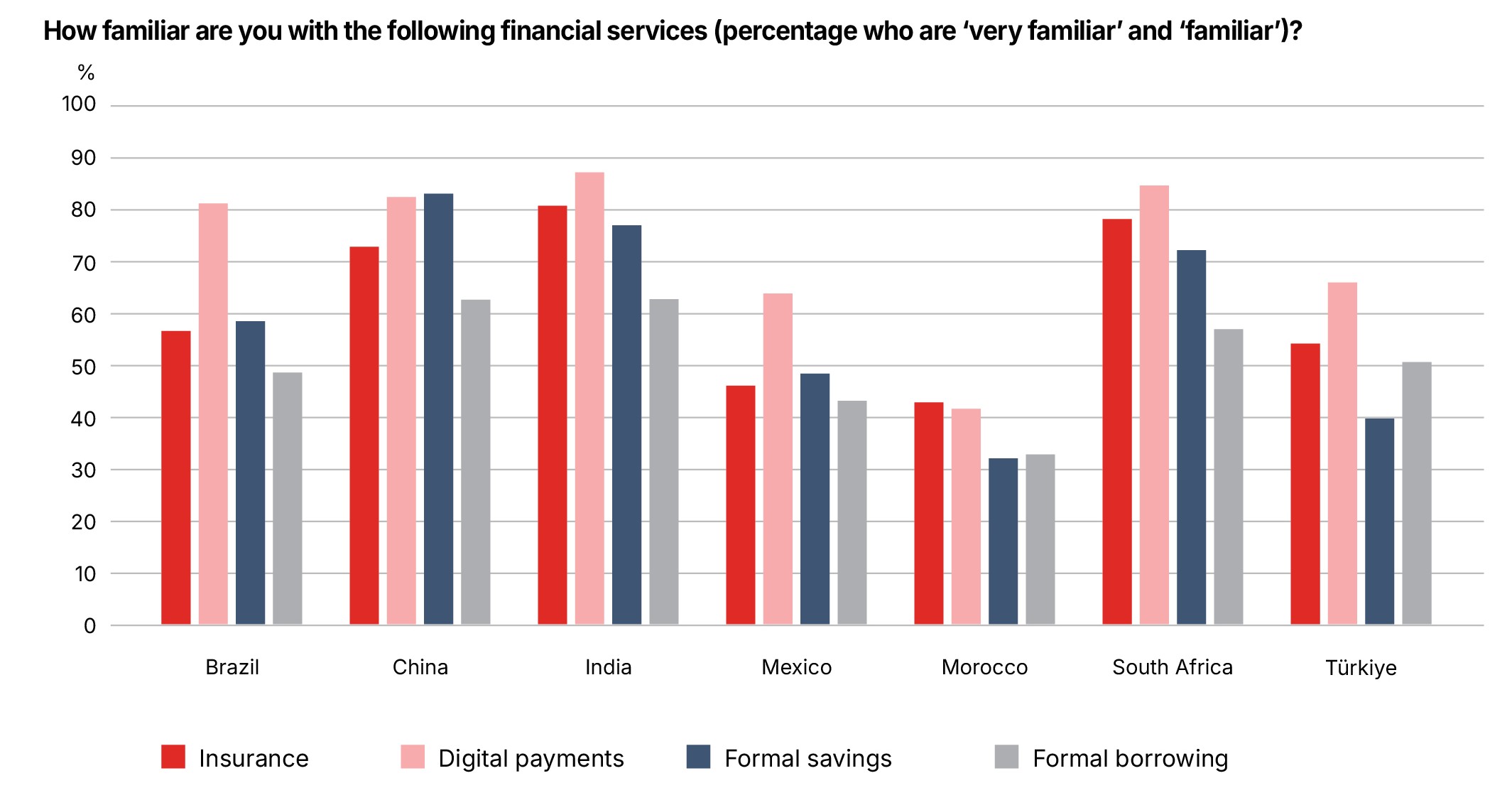

The survey evaluated respondents’ familiarity with four key financial services: digital payments, formal savings, insurance, and borrowing. The findings reveal significant cross-country variation, with China, India, and South Africa displaying the highest overall familiarity and Morocco exhibiting the lowest. Digital payments are the most recognised service, with the exception of formal savings in China and insurance in Morocco. At around 70–80% of respondents, China, India, and South Africa demonstrate the greatest levels of familiarity with insurance-related services (see Figure 3).

China’s elevated familiarity can be primarily attributed to its robust digital financial ecosystem. The widespread adoption of fintech platforms such as Alipay and WeChat Pay has transformed traditional financial interactions, seamlessly integrating payments, savings, and insurance into everyday mobile use. These platforms have significantly lowered the entry barriers to financial services, thereby increasing awareness and participation, even among previously unbanked populations. The result is a population highly attuned to formal financial products through user-friendly, technology-driven channels.44

South Africa’s relatively high familiarity with insurance is underpinned by its established, albeit uneven, insurance sector.45 Funeral, life, and hospital cash policies are widely advertised and culturally embedded, contributing to a heightened awareness of such products.

Similarly, India’s strong performance in this domain reflects the impact of state-led financial inclusion programmes. The Pradhan Mantri Jan Dhan Yojana (PMJDY) initiative has introduced millions of people to formal financial services. More specifically, the Pradhan Mantri Jan Arogya Yojana (PMJAY) has expanded subsidised access to health insurance for low-income families, introducing many to formal insurance schemes (see Box 4).

In contrast, Morocco’s low familiarity levels likely stem from a confluence of structural and socioeconomic constraints. Financial literacy remains relatively limited, especially in rural regions, where digital infrastructure is sparse and access to formal financial institutions is often constrained. Informal financial practices dominate, further diminishing familiarity with formal mechanisms such as savings accounts, insurance policies, or borrowing.46

FIGURE 3: FAMILIARITY WITH FINANCIAL SERVICES

Source: Geneva Association customer survey, powered by Kantar

Usage of financial services

Digital payments are the most widely used financial product across the majority of surveyed countries. China and India exhibit the highest levels of insurance penetration, at around 75% and 70%, respectively.47 In contrast, formal borrowing registers the lowest usage rates in nearly all markets (see Figure 4).

This pattern aligns with broader global trends in financial technology adoption. The widespread use of digital payments can be attributed to increasing smartphone

penetration, expanded internet access, and the proliferation of mobile wallet applications.48 In China, the preference for formal savings reflects a longstanding cultural orientation toward thrift, reinforced by the seamless integration of savings products into ubiquitous super-app platforms such as WeChat and Alipay.

The relatively high uptake of insurance in select countries is indicative of institutional innovations, including public-private partnerships and targeted microinsurance schemes. In India, for example, government initiatives associated with the PMJDY initiative have significantly expanded coverage.49

The limited use of formal credit in many emerging markets points to persistent structural barriers such as insufficient credit files, resulting from limited formal financial engagement, as well as low levels of financial literacy. Moreover, informal labour markets and lack of collateral further exacerbate exclusion from formal lending channels.50

FIGURE 4: USE OF FINANCIAL SERVICES

Source: Geneva Association customer survey, powered by Kantar

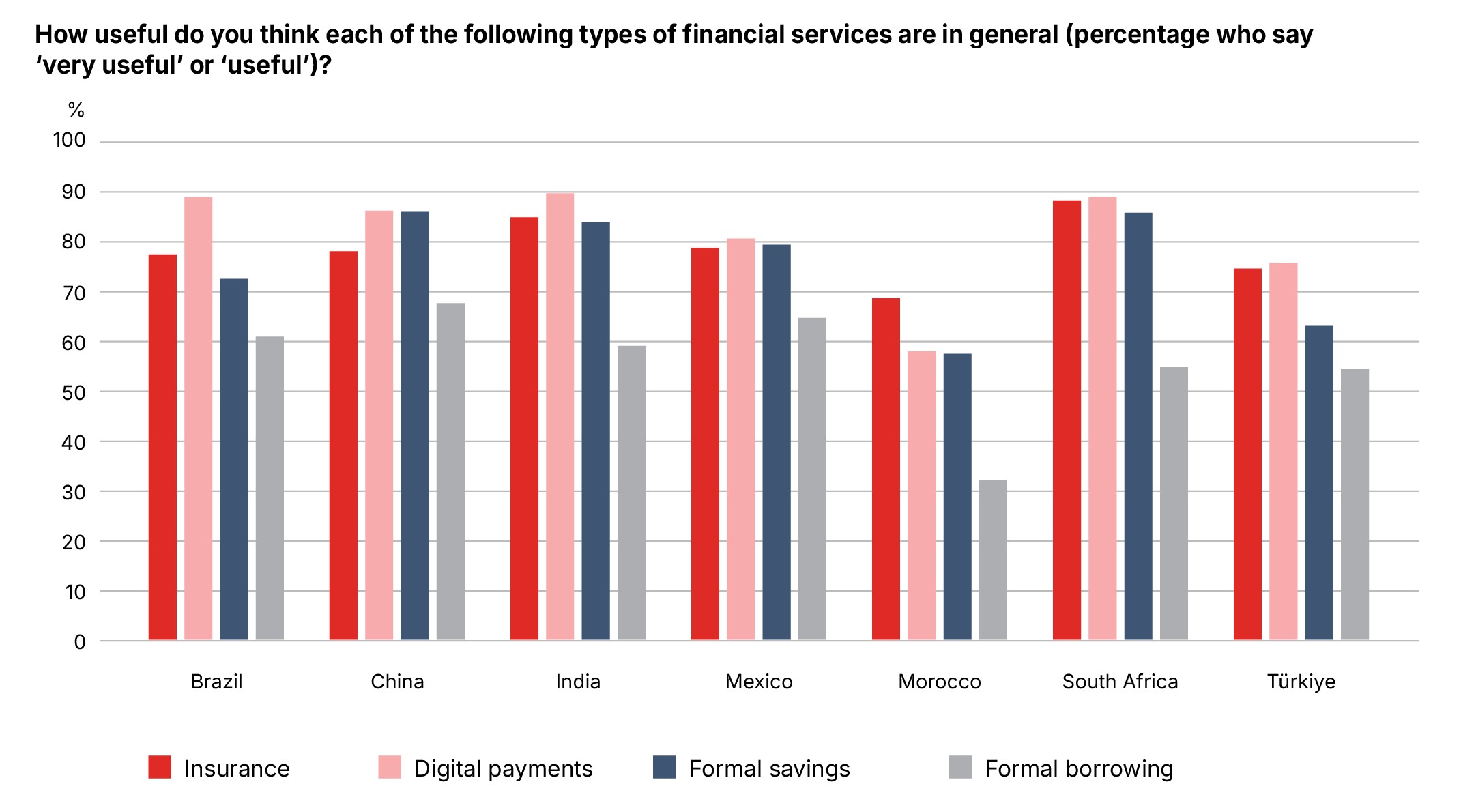

Perceived usefulness of financial services

Survey responses across the seven markets reveal divergent perceptions of financial service utility. Digital payments are rated as the most useful financial service in all surveyed countries except Morocco, where insurance is considered more beneficial. In all countries investigated, insurance is viewed favourably, with at least 70% of respondents considering it useful. Borrowing is viewed as the least beneficial financial service across all countries (see Figure 5).

The high ratings for digital payments reflect their role in enhancing financial efficiency, particularly in contexts with mature mobile ecosystems such as China and government-supported digital infrastructures like Brazil and India. The COVID-19 pandemic further accelerated the digitalisation of economic activity, solidifying mobile payments as a trusted, fast, and low-friction method for daily transactions.51

The consistently low perceived usefulness of borrowing is notable and may signal structural constraints, such as financial customers in emerging markets often facing adverse outcomes like debt distress, over-indebtedness, or high interest burdens charged by informal providers.52

FIGURE 5: USEFULNESS OF FINANCIAL SERVICES

Source: Geneva Association customer survey, powered by Kantar

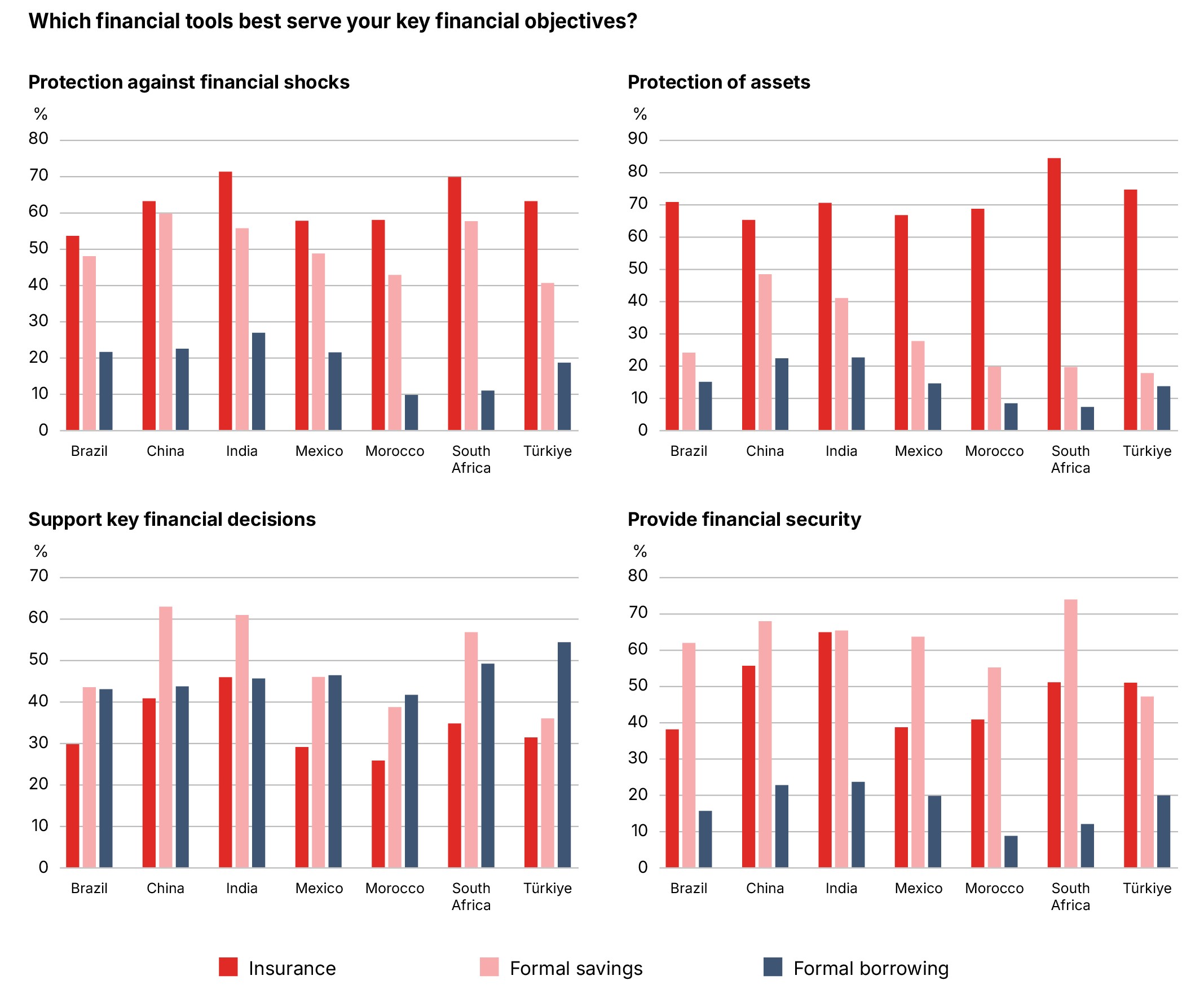

Relevance for key financial objectives

Survey respondents were asked to identify which financial tools best support their financial goals. Insurance is broadly perceived as essential for asset protection and shielding against financial shocks, such as the main breadwinner’s premature death or major out-of-pocket health expenditure. Meanwhile, savings (especially in China, India, and South Africa) and borrowing (especially in Türkiye and South Africa) are associated with major life decisions such as education or buying a home. When considering long-term financial security, such as retirement planning, savings emerge as the dominant tool, though insurance is co-ranked alongside savings in countries like India and Türkiye (Figure 6).

The strong association of insurance with risk mitigation and protection is a positive signal for insurers and policymakers alike. In economically vulnerable or disaster-prone markets, such as those facing health-system fragility or climate-related threats, the presence of a risk-transfer mechanism like insurance becomes critical. Its perceived relevance is likely to reflect an understanding of its stabilising role, especially in the absence of public safety nets. The prominence of savings in both immediate and long-term contexts suggests a preference for liquidity and autonomy as well as the perceived inadequacy of retirement systems. In India, for example, the absence of comprehensive public pensions has driven individuals to rely heavily on personal savings.53

Notably, except for China and India, insurance plays a relatively weak role in shaping or supporting critical life decisions such as starting a family, buying a home, or launching a business. This limited relevance points to deficits in financial literacy, insurance market development and the perceived value of risk-transfer mechanisms.54

FIGURE 6: RELEVANCE OF FINANCIAL TOOLS

Source: Geneva Association customer survey, powered by Kantar

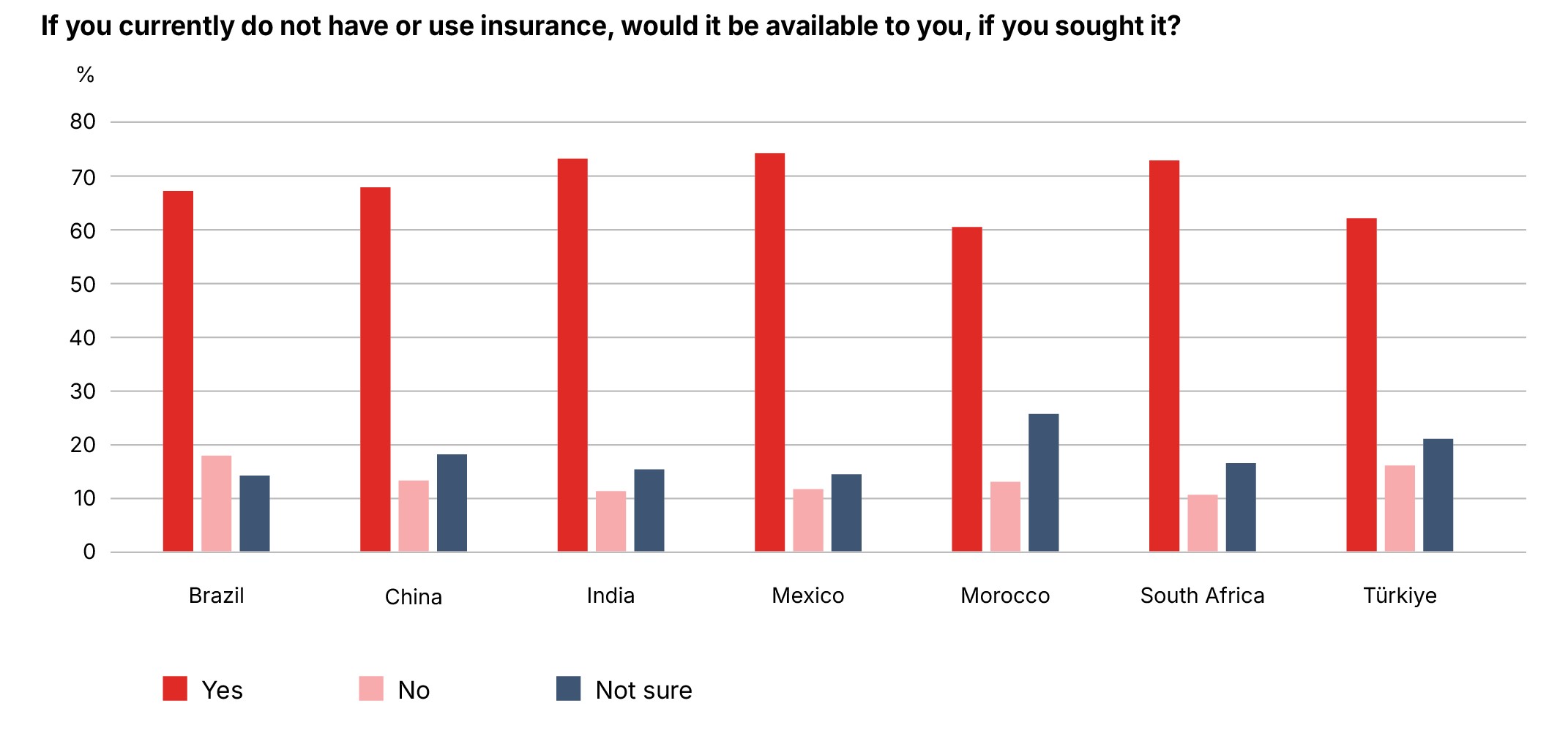

Access to insurance

Access to insurance per se does not appear to be the primary obstacle to uptake among respondents. When uninsured individuals were asked whether they could obtain coverage if desired, a significant majority affirmed that access was not a significant constraint. This suggests that demand-side factors, such as affordability and knowledge gaps, are more salient impediments to insurance adoption in emerging markets (see Figure 7 and section 4.8).

This finding aligns with the substantial progress made in insurance-distribution infrastructure. Mobile-based platforms, digital insurance, and community-based distribution models, including local agent initiatives, have enhanced penetration by leveraging mobile-phone adoption, improving internet connectivity, and building social capital and trust within communities.55,56

FIGURE 7: AVAILABILITY OF INSURANCE

Source: Geneva Association customer survey, powered by Kantar

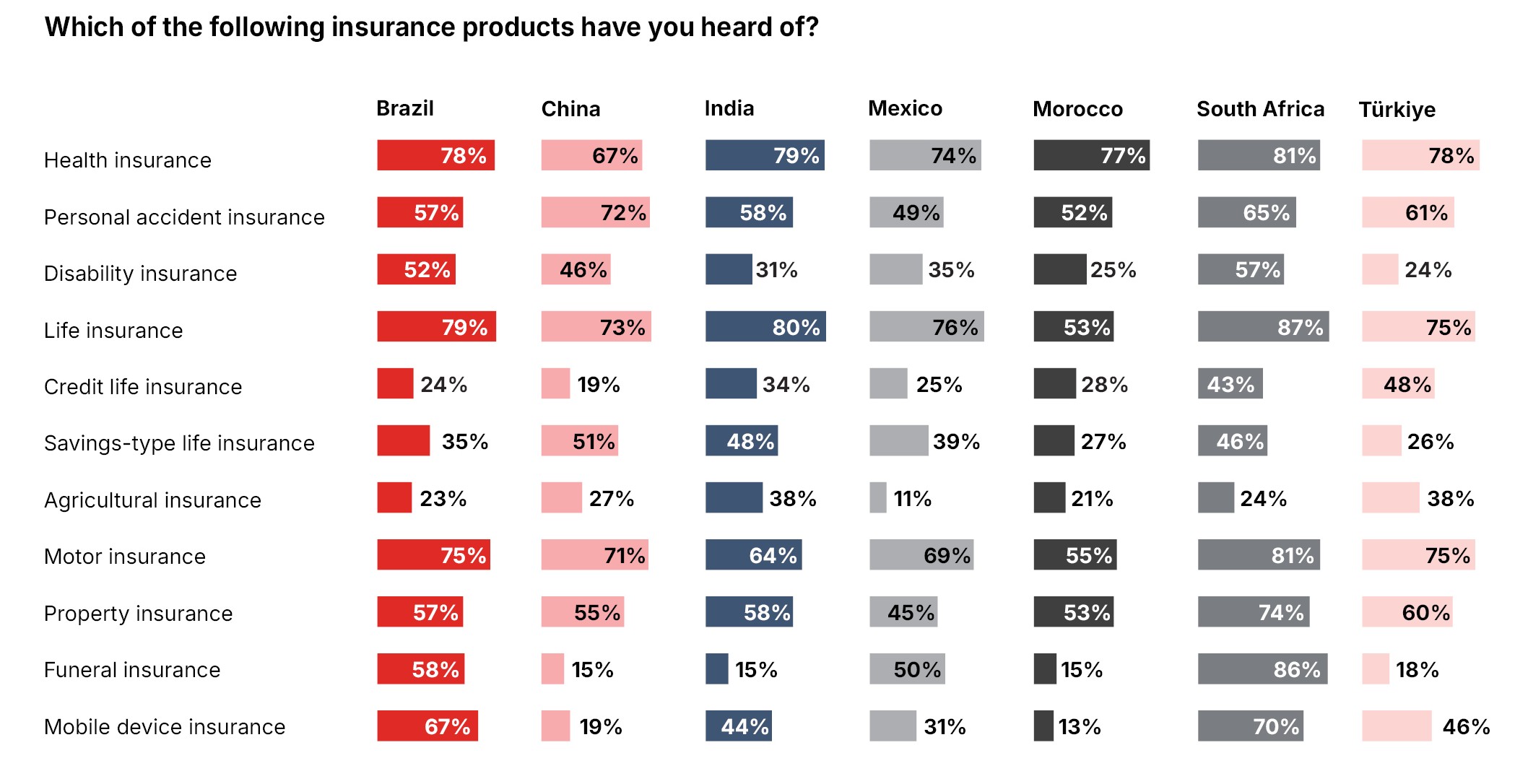

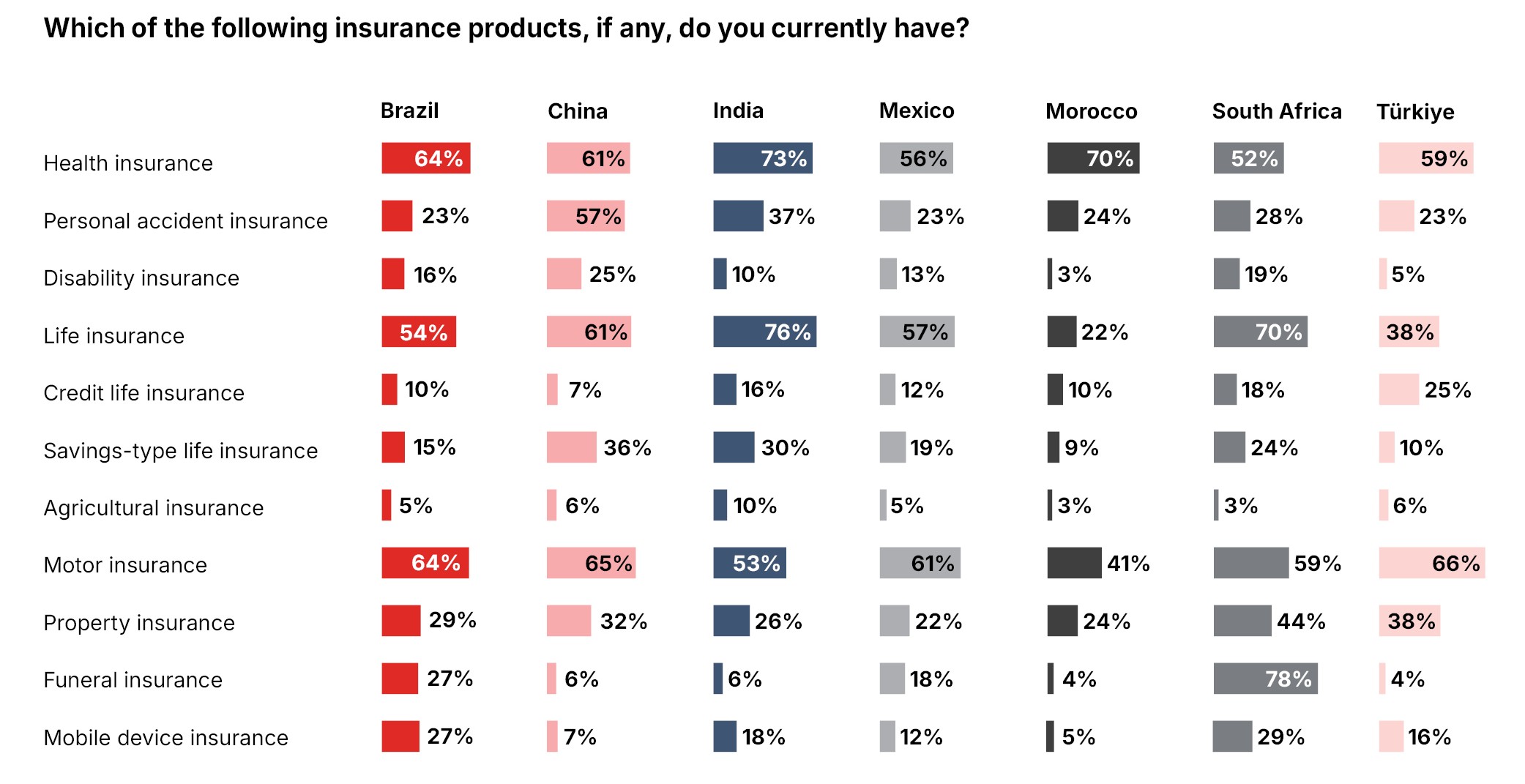

Awareness and usage of specific insurance products

Insurance awareness and uptake are shaped by an interplay of behavioural and structural determinants. A prominent behavioural influence is the availability heuristic, whereby individuals display heightened awareness of and demand for insurance products associated with life events that are frequently encountered or emotionally salient.57 Products covering health risks, mortality, or motor accidents are top of mind for survey participants due to the vividness of the underlying events. As a result, insurance offerings such as health, (term) life, and motor insurance are more likely to be perceived as necessary and adopted (see Figures 8 and 9).

Structural factors, particularly policy and regulatory frameworks, play an important complementary role in shaping both awareness and usage. For instance, the existence of state-mandated or employer-sponsored health insurance schemes enhances familiarity with and access to formal insurance mechanisms.

While high awareness correlates with higher usage in essential or mandated products, the gap between familiarity and adoption remains substantial in complex or discretionary products (e.g. disability and savings-type life insurance). The relatively low uptake of such insurance instruments, especially in Morocco and Türkiye (see Figure 9), highlights factors such as limited financial literacy, absence of tailored educational initiatives, cultural and religious considerations, and liquidity constraints that hinder households from committing to long-term financial products.58 Moreover, behavioural factors such as present bias lead individuals to excessively discount future benefits, making products with deferred or abstract payoffs less attractive.59 All in all, the survey suggests major protection gaps in critical areas such as property, disability, and longevity risks.

Brazil and South Africa exhibit unusually high awareness and uptake of niche products such as mobile-device and funeral insurance, respectively. In Brazil, this pattern is driven by widespread smartphone penetration and distribution models that bundle insurance coverage with telecommunications services.60 Conversely, in South Africa, uptake of funeral insurance is exceptionally high, reflecting the cultural significance of funerals. The high premium placed on dignified burial ceremonies has entrenched funeral insurance as a socially important financial tool. Decades of microinsurance initiatives, often channeled through funeral parlours and community-based agents and supported by conducive regulatory frameworks, have institutionalised its usage.61

Funeral insurance in South Africa illustrates what could be achieved for protection gaps more broadly when cultural factors, distribution mechanisms, product relevance, and regulatory frameworks align.

FIGURE 8: FAMILIARITY WITH INSURANCE PRODUCTS

Source: Geneva Association customer survey, powered by Kantar

FIGURE 9: INSURANCE OWNERSHIP

Source: Geneva Association customer survey, powered by Kantar

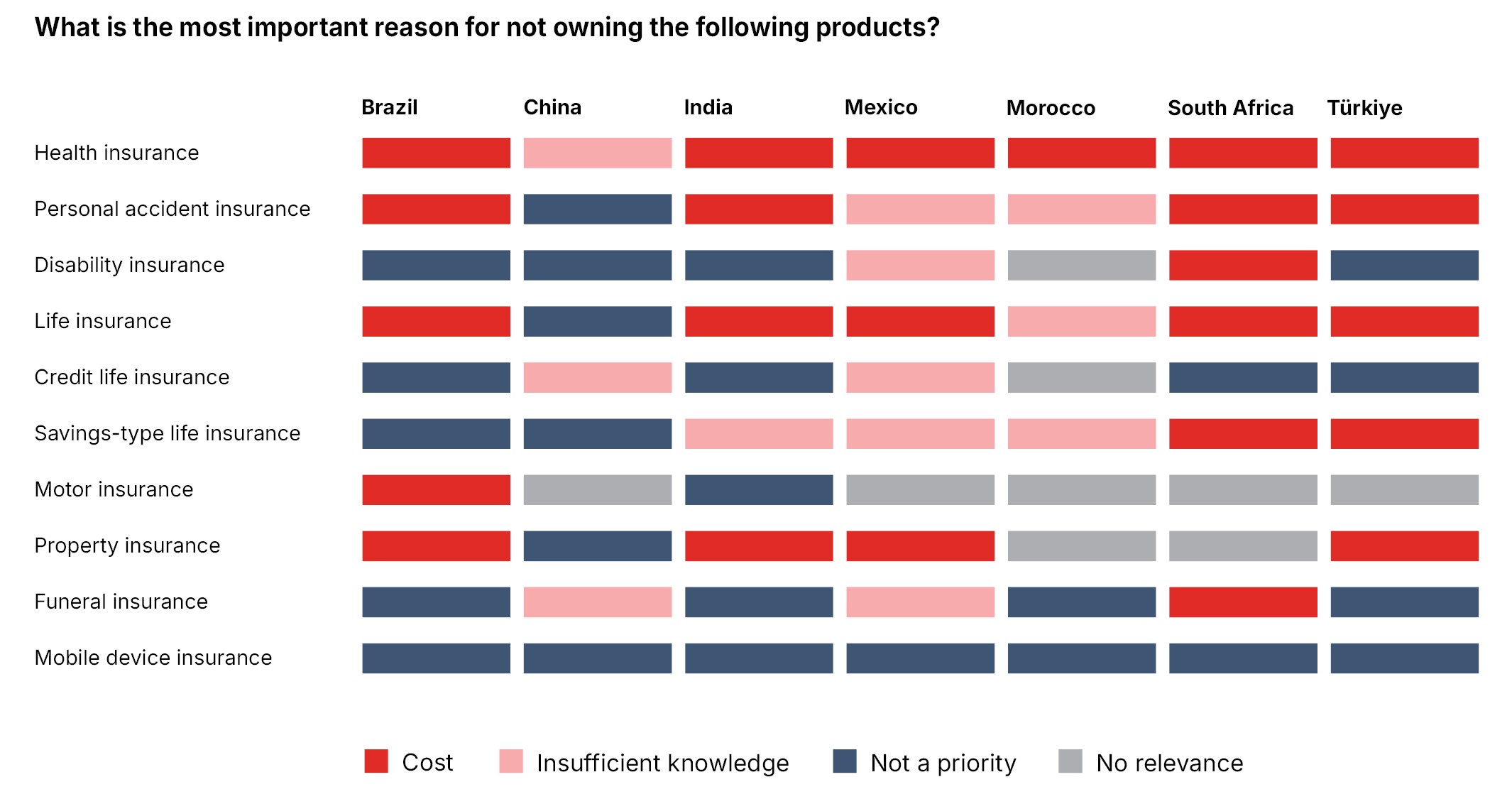

Reasons for non-ownership of insurance

Figure 10 delves into the reasons behind non-ownership of insurance products among respondents who currently lack any form of coverage. In the case of health and (term) life insurance, affordability stands out as the dominant obstacle. This finding is consistent in all surveyed countries except China, the wealthiest nation in the sample, where knowledge and prioritisation are more frequently cited as the key barriers. This suggests that in more economically developed markets, cognitive constraints may (begin to) outweigh purely financial ones.

The perceived irrelevance of motor insurance in most countries likely stems from limited private vehicle ownership and the prevalence of informal or public transport options. Similarly, the relatively low uptake of funeral, mobile device, and disability insurance appears to reflect deeper cultural and behavioural factors. Respondents may not prioritise these products due to optimism bias, i.e. the belief that negative events are unlikely to happen to them,62 due to cultural discomfort in planning for death and incapacity or the perceived immateriality of losses affecting mobile devices.

When it comes to savings-oriented life insurance, knowledge gaps again emerge as a primary hindrance. This may signal the need for product simplification and improved transparency alongside broader financial education efforts. Such findings align with the notion that even where products are physically available, uptake is still constrained by limited understanding and a lack of prioritisation.63

In summary, the results suggest that the most pressing barriers to insurance ownership are economic (unaffordability), cognitive (lack of knowledge) and behavioural (incompatible priorities), implying that future commercial, policy, or regulatory interventions should focus on affordability, education, and behavioural change.

FIGURE 10: REASONS FOR NOT OWNING INSURANCE

Source: Geneva Association customer survey, powered by Kantar

Success factors of insurance inclusion: An integrated perspective

This section builds on the preceding analysis of financial inclusion as a driver of economic development, the unique role that insurance plays in expanding the financial frontier to underserved populations, and the new comparative, survey-based data presented and discussed in the previous section. Combined with invaluable insights from about 30 executive and expert interviews, these findings establish the foundation for identifying and examining key success factors that enable inclusive insurance to scale in emerging markets.

An integrated approach to key success factors for inclusive insurance is essential due to the complex interplay between commercial sustainability, public policy objectives, and regulatory oversight. Traditional analyses often treat these domains in isolation, overlooking how their tradeoffs and complementarities shape market outcomes. This holistic methodology recognises that commercial strategies are strongly influenced by policy and regulatory incentives and constraints, just as policy effectiveness depends on private-sector engagement and regulatory capacity.

For instance, a health insurance product targeting informal workers may only succeed if it aligns commercial aspects (e.g. affordable premiums and scalable distribution), public-policy goals (e.g. universal health coverage) and regulatory enablers (e.g. simplified licensing and digital claims processes). Also, without public premium subsidies for low-income households, insurers may face limited demand. Likewise, the product is unlikely to scale if regulatory frameworks do not accommodate mobile enrolment or recognise group health schemes linked to informal worker associations.

“Inclusive insurance is a cornerstone of financial resilience, especially for underserved populations and micro, small, and medium enterprises that make up the backbone of many economies. To unlock its full potential, we must elevate insurance from the margins of financial inclusion to the heart of risk management. This requires risk literacy, risk reduction, innovative products, enabling regulation, and a shift in narrative – from access to positive impact. As climate, nature, and economic risks intensify, inclusive insurance is essential for a just transition to resilient and sustainable communities and economies.”

Butch Bacani, United Nations Environment Programme

Commercial success factors

The expansion of inclusive insurance in emerging markets depends on a set of insurer-driven success factors (see Table 2). Across all these factors, long-term commercial viability is a foundational prerequisite for inclusive insurance that can scale, endure, and deliver meaningful social impact.64

Product-market fit

Viable inclusive insurance products in emerging markets necessitate a deliberate departure from simply offering existing products to different customer segments. Instead, products must be purpose built to meet the distinctive preferences, constraints, and behavioral patterns of low-income and other underserved segments. The SUAVE framework, which emphasises simplicity, understandability, accessibility, value, and efficiency, provides a normative blueprint for inclusive insurance product architecture, grounded in both behavioural economics and operational feasibility.65

Simplicity involves minimising contractual and procedural complexity. Policy terms should be intuitive, exclusions limited, and claims processes streamlined, often relying on basic documentation such as photographic evidence to reduce transaction costs and cognitive burden. This mitigates barriers associated with limited financial literacy and enhances the likelihood of sustained engagement.

Understandability pertains to the use of standardised, jargon-free language across all customer-facing materials. It supports transparency, improves customer comprehension even in the face of knowledge gaps, and strengthens the capacity of distribution agents to communicate value propositions clearly. This is particularly salient in emerging market contexts, where formal insurance is novel and trust remains nascent.

Accessibility encompasses both geographic and technological dimensions. Products must be transactable via low-friction digital channels, e.g. mobile money, e-signatures, and remote onboarding, thereby reducing the need for physical infrastructure.66

Value is defined by actuarial fairness and contextual relevance. Premiums must reflect customers’ risk profiles and payment capacities, while offering sufficient coverage and flexibility. Practitioners interviewed for this research suggest target loss ratios between 60% and 80% to ensure customer benefit without undermining commercial sustainability. Bundled products can also reduce cumulative premiums while covering multiple risks.67

Efficiency relates to operational scalability and responsiveness. Leveraging InsurTech, e.g. automated underwriting, digital claims assessment, and client analytics, can not only enhance cost effectiveness and affordability but also service quality.68

Parametric insurance exemplifies a product innovation that aligns with the SUAVE framework for inclusive insurance. Its simplicity derives from the use of clear, objective triggers (e.g. rainfall indices), which eliminate the need for complex claims assessments. The model’s design enhances understandability, as customers can more readily comprehend trigger-based payouts compared to traditional loss evaluations, particularly when linked to locally relevant risks such as drought or flooding. Parametric insurance also improves accessibility by effectively reaching underserved populations, including smallholder farmers and informal workers, often through mobile or digital delivery channels. Furthermore, it offers significant value by providing prompt liquidity following adverse events, thereby mitigating poverty risk and facilitating faster recovery. Finally, the model’s efficiency is demonstrated through expedited, automatic disbursements that reduce administrative costs and delays, ultimately fostering greater trust and long-term sustainability.69

“In Brazil, insurance remains undervalued, inaccessible, and unaffordable for much of the population due to low financial literacy and product complexity. To address this, the sector must prioritise simplified products and leverage mobile technology, amongst other actions. I strongly believe that insurance is not merely a financial product but a critical mechanism for protecting households from economic shocks, supporting health and education outcomes, and enhancing resilience to climate-related risks. Expanding access to inclusive insurance is essential for fostering long-term social and economic stability.”

Vinicius Marinho da Cruz, Bradesco Seguros

“Success in inclusive insurance hinges on offering simple, relevant, and affordable products. An example from China is ZhongAn’s ‘million-dollar medical insurance’, a high-deductible, high-coverage insurance plan for critical illnesses starting from USD 20 annual premiums for around USD 1 million coverage. It complements China’s basic public healthcare, covering critical illnesses like cancer that the public system may not fully cover. Another example from Malaysia is Grab’s daily e-hailing insurance. The ride-sharing platform developed daily commercial motor insurance, allowing parttime drivers to comply with government insurance mandates affordably and flexibly, increasing both compliance and inclusion.”

Christoph Krieg, Peak3

Distribution efficiency

To reach low-income, remote, and underserved populations with inclusive insurance, distribution models need to be rethought. Traditional channels, reliant on broker networks and agency-based sales, face limits in markets characterised by limited insurance awareness, infrastructural constraints, and high transaction costs. In this context, innovative, partnership-driven, and digitally enabled distribution strategies have emerged as critical determinants of market penetration and cost efficiency.70

A growing body of empirical evidence supports the efficacy of multi-sectoral affinity partnerships with mobile network operators, microfinance institutions, cooperatives, retailers, community-based organisations, and post offices in achieving scale and trust simultaneously.71 These actors offer pre-existing customer bases, infrastructural reach and, in many cases, established reputational capital, all of which reduce acquisition costs and mitigate informational asymmetries. Mobile platforms are particularly salient, which facilitate digital onboarding, micro-premium collection (often via airtime deductions) and expedited claims settlement through mobile money. This well-established infrastructure is pivotal in overcoming geographic and economic barriers to insurance access.72

Embedded insurance models represent another frontier innovation in inclusive insurance distribution. By integrating coverage into existing customer transactions, such as telecommunications services, digital lending, e-commerce, ridesharing, or airline bookings, insurers can align product offerings with real-time customer behaviour. This contextual and point-of-sale-driven approach reduces friction in the purchasing process, increases uptake through default inclusion, and allows for dynamic product customisation based on transaction data.73

Bancassurance remains an important complementary channel in regions such as Latin America. Banks’ trusted status and access to customer data enable targeted cross-selling, particularly when supported by appropriate regulatory frameworks. The deployment of localised agent networks through bank outlets, trained in culturally resonant communication and equipped with mobile technologies, is essential for last-mile delivery.74

These hybrid models, which combine digital efficiency with human interaction, are particularly effective in low-literacy or low-trust environments. An integrated, omnichannel distribution architecture that balances scale, personalisation, and trust is therefore a structural necessity for the expansion of inclusive insurance in emerging markets (see Box 2 for a case study on South Africa).

“Inclusive insurance in Brazil thrives when affordability, simplicity, and trust come together. Success depends on offering cost-effective products, intuitive design, and building partnerships across industries – fintechs, retailers, or any business that connects with these consumers – to reach underserved segments. Bundling insurance with services like telemedicine increases perceived value, while clear, transparent offerings help build trust. Financial education and culturally aware engagement are key, as many Brazilians don’t actively seek insurance. By embedding insurance into everyday digital experiences, insurers can create both social impact and commercial sustainability.”

Luciana Amano, Prudential Financial

Customer trust

Customer trust is a foundational prerequisite for the effectiveness and sustainability of inclusive insurance, particularly in emerging markets, where significant portions of the population remain unacquainted with formal risktransfer mechanisms (e.g. this applies to Morocco, see Figure 3). Trust is an enabler that directly influences both the initial uptake and continued engagement of low-income and underserved segments with insurance products.75

The principal determinant of trust is the integrity of claims management. A ‘claims-first’ approach, which prioritises the efficient, timely, and equitable settlement of claims, is insurers’ primary reputational asset, especially in the context of inclusive insurance. In the face of informational asymmetries and institutional unfamiliarity, any delays, rejections, or procedural opacity in claims handling can undermine customer confidence and trigger adverse selection or attrition effects.76

Equally important are product intelligibility and contextual relevance. Trust is eroded when policy terms are excessively complex, opaque, or perceived as misaligned with customer needs. By contrast, simplified product architecture, transparent conditions, and culturally salient offerings, such as low-cost funeral insurance in South Africa or usage-based vehicle insurance in Southeast Asia, enhance perceived value and trust in insurers and their offerings.77

Trust intermediated through proximate, affinity distribution networks, i.e. organisations that have a pre-existing relationship with a pool of potential customers, further amplifies the adoption of insurance. Peer-based models that leverage local actors, such as microfinance agents or community leaders, can outperform digital channels in low-literacy settings by mitigating skepticism and increasing persistence.78

Data-driven innovation

In emerging economies, AI and digital technology are essential for developing efficient, scalable insurance models that can reach underserved populations. Advanced analytics and machine-learning technologies, for example, play a pivotal role, particularly in affinity-based partnership models where insurers can benefit from their partners’ pre-existing relationship with potential customers. These tools enable more granular risk assessment and segmentation by analysing diverse data sources such as behavioural patterns and transaction histories. This allows insurers to develop more accurate, personalised pricing strategies, which are especially critical in emerging economies where traditional data may be limited or unreliable. AI also enhances product design, fraud detection, and claims automation, making insurance not only more precise but also more accessible and affordable for underserved populations.79 More specifically:

- To address infrastructure challenges, insurers are increasingly adopting mobile applications and cloud platforms to achieve operational efficiency. These technologies streamline key processes such as policy issuance, premium collection, and claims management. Mobile apps enhance customer engagement through user-friendly interfaces, while cloud platforms offer scalable, secure, and real-time data solutions. Together, they reduce costs and support the delivery of faster and more responsive insurance services.80

- Real-time data collected from satellite imagery and Internet of Things (IoT) sensors enables the development of parametric, index-based insurance products, for example. These technologies support automated trigger mechanisms, significantly reducing the need for manual claims verification. As a result, insurers can provide faster, more transparent and efficient payouts to policyholders (see section 5.1.1).

- Alternative data sources, such as transactional data, which users have consented to share (e.g. related to e-commerce and ride-hailing), significantly enhance the accuracy of risk assessment, especially for individuals who lack traditional employment records or credit histories.81

“In an evolving landscape where the boundaries between finance, healthcare, and ageing services are increasingly blurred, leading organisations are rethinking how to deliver value through integrated, technology-enabled models. Ping An has adopted a strategy, enabled by AI and big data, that aligns financial services with health and senior care to address some of society’s most pressing challenges. The integration of health and elder care services reflects a forward-looking approach to preventive health and ageing with dignity. This model points to a future where insurance is not merely a safety net but a proactive enabler of well-being.”

Richard Sheng, Ping An

TABLE 2: COMMERCIAL SUCCESS FACTORS FOR INCLUSIVE INSURANCE IN EMERGING ECONOMIES

Product-market fit | Distribution efficiency | Customer trust | Data-driven innovation |

| Simplicity | Digital enablement | Claims management | Artificial intelligence |

| Understandability | Affinity partnerships | Product intelligibility | Mobile applications |

| Accessibility | Embedded models | Contextual relevance | Cloud platforms |

| Value | Bancassurance | Affinity distribution | Real-time data collection |

| Efficiency | Omnichannel | Alternative data sources |

Source: Geneva Association

Box 1: Reducing protection gaps through embedded and bundled insurance – The importance of strategic partnerships in empowering Colombia's microentrepreneurs and their families